A massive boom is coming.

And those prepared are set to make a lot of money.

It could rival the gains of cryptos and meme digital assets such as Dogecoin.

Only, this stuff is real. It’s tangible. And it’s going to make early investors a lot of money.

But before I tell you about it, you have to first understand my train of thought on how I arrived at this prediction.

Let’s go.

If You Don’t Ask, You’ll Never Learn

Asking questions has terrible consequences nowadays.

Ask a question about COVID. You’re an idiot.

Ask a question about vaccines. You’re a conspiracy theorist.

Ask a question about politics. You’re far left or far right.

Ask a question about both? You’re canceled.

I can tell you that I have experienced every one of those instances over the past year.

In fact, when I suggested that COVID could have come from a lab last year, I was called a conspiracy theorist, an idiot, far-right, and even canceled (temporarily) on social media platforms.

Well, if I am a conspiracy theorist, an idiot, and far-right, then I guess leading scientists from around the world are too.

Because just last week, 18 of the world’s leading scientists suggested the same thing.

Via the American Association for the Advancement of Science:

“On 30 December 2019, the Program for Monitoring Emerging Diseases notified the world about a pneumonia of unknown cause in Wuhan, China. Since then, scientists have made remarkable progress in understanding the causative agent, severe acute respiratory syndrome coronavirus 2 (SARS-CoV-2), its transmission, pathogenesis, and mitigation by vaccines, therapeutics, and non-pharmaceutical interventions. Yet more investigation is still needed to determine the origin of the pandemic. Theories of accidental release from a lab and zoonotic spillover both remain viable. Knowing how COVID-19 emerged is critical for informing global strategies to mitigate the risk of future outbreaks.

… Although there were no findings in clear support of either a natural spillover or a lab accident, the team assessed a zoonotic spillover from an intermediate host as “likely to very likely,” and a laboratory incident as “extremely unlikely”. Furthermore, the two theories were not given balanced consideration. Only 4 of the 313 pages of the report and its annexes addressed the possibility of a laboratory accident. Notably, WHO Director-General Tedros Ghebreyesus commented that the report’s consideration of evidence supporting a laboratory accident was insufficient and offered to provide additional resources to fully evaluate the possibility.”

To be clear, I never said for sure that COVID came from a lab; I merely raised the question and suggested that it was a possibility – just like 18 world-renowned scientists are now doing. And why shouldn’t we ask?

Then, in another letter, I revealed how the RT-PCR COVID test, the gold standard for COVID testing, was extremely misleading because of the high level of sensitivity being used in defining a positive case – especially when it came to its use in determining quarantine measures and lockdowns.

Via Everything You Need to Know About COVID Testing:

“It doesn’t matter how much evidence shows that the current testing methods for COVID-19 are highly inaccurate…governments around the world will force a lockdown.

… the data suggests that only 10% of those who tested positive for COVID may actually be infectious and need to isolate, if they’re even sick or contagious at all.”

I was called a conspiracy theorist for that letter. I was even told by a Canadian Facebook user that I was killing people and that I should be locked in jail for spreading misinformation.

That was last November.

It turns out I was right.

The truth is now coming through the Canadian courts.

Via the Justice Centre for Constitutional Freedoms:

“The Justice Centre’s expert medical witnesses, Dr. Jay Bhattacharya, world-famous epidemiologist and Professor of Medicine from Stanford University, and Dr. Thomas Warren, infectious disease specialist and medical microbiologist, both provided evidence that the PCR test is unreliable in determining whether a person is infectious with the actual Covid-19 disease.

Chief Microbiologist and Laboratory Specialist Dr. Jared Bullard is a witness for the Manitoba government in this hearing. Questioned under oath by Justice Centre lawyers on Monday, May 10, Dr. Bullard acknowledged that the PCR test has significant limitations.

The head of Cadham Provincial Laboratory in Winnipeg, Dr. Bullard admitted that PCR test results do not verify infectiousness, and were never intended to be used to diagnose respiratory illnesses.

Dr. Bullard testified that PCR tests can be positive for up to 100 days after an exposure to the virus, and that PCR tests do nothing more than confirm the presence of fragments of viral RNA of the target SARS CO-V2 virus in someone’s nose. He testified that, while a person with Covid-19 is infectious for a one-to-two week period, non-viable (harmless) viral SARS CO-V2 fragments remain in the nose, and can be detected by a PCR test for up to 100 days after exposure.

Dr. Bullard testified that the most accurate way to determine whether someone is actually infectious with Covid is to attempt to grow a cell culture in the lab from a patient sample. If a cell culture will not grow the virus in the lab, a patient is likely not infectious. A study from Dr. Bullard and his colleagues found that only 44% of positive PCR test results would actually grow in the lab.”

The next question then becomes what Ct value is actually being used in these tests.

I suggested in November, that the Ct value being most widely used was 40, based on the evidence I had.

Via Everything You Need to Know About COVID Testing, continued:

“Do you know what Ct count most labs use? Forty. Four Zero. 40.

…If a Ct of 40 is too high, why are labs around the world using it? Why does the WHO recommend a Ct as high as 45?”

Turns out, Manitoba has been using 40, and in some cases 45 – just as I had suggested.

Via the Justice Centre for Constitutional Freedoms, continued:

“Manitoba has confirmed that it utilizes Ct’s of up to 40, and even 45 in some cases. This indicates “cases” resulting from such tests (above a Ct of 25) are almost certainly not actually infectious.”

The inaccuracies of the PCR test were only the beginning of the widespread misinformation on COVID.

What was worse was how they counted COVID deaths…

Via The Real Reason Why COVID-19 Death Rates are so High, April 2020:

“A doctor can label anyone who dies with the symptoms of COVID-19 – which are very hard to distinguish from the common cold, flu, or even pneumonia – without actually testing them.”

The keywords here are “symptoms of COVID-19” – which is a long list that includes being short of breath, coughing, wheezing, and overall weakness.

The last I checked, when people die, many of them experience one of these symptoms.

And in many other letters, I continued to reveal the flaw in that reporting – including how some traffic accidents have been added to the COVID death count.

Of course, I was once again called a conspiracy theorist, an idiot, and a liar.

But guess what?

Six months later after I revealed why the COVID death rate was so high, Ontario’s health official admitted exactly what I have been saying for over a year.

Via the Toronto Sun:

“The daily pandemic death counts in Ontario include people who have tested positive for COVID-19 but have not necessarily died from the virus.

The exact number of people who fit into this category is unknown by the government and not even being counted.

… The Sun was able to confirm this information after speaking with three of the hardest-hit public health units in Ontario — Toronto, Ottawa, and Peel Region.

“The mortality data sent to the Ministry and reported in (Ottawa Public Health) dashboard/reports represents the number of Ottawa residents with confirmed COVID-19 who have passed away,” an Ottawa Public Health spokesperson explained via email. “It does not indicate if COVID-19 was the cause of death, and we can’t make that inference.”

According to local health units, this reporting process is required by the province.

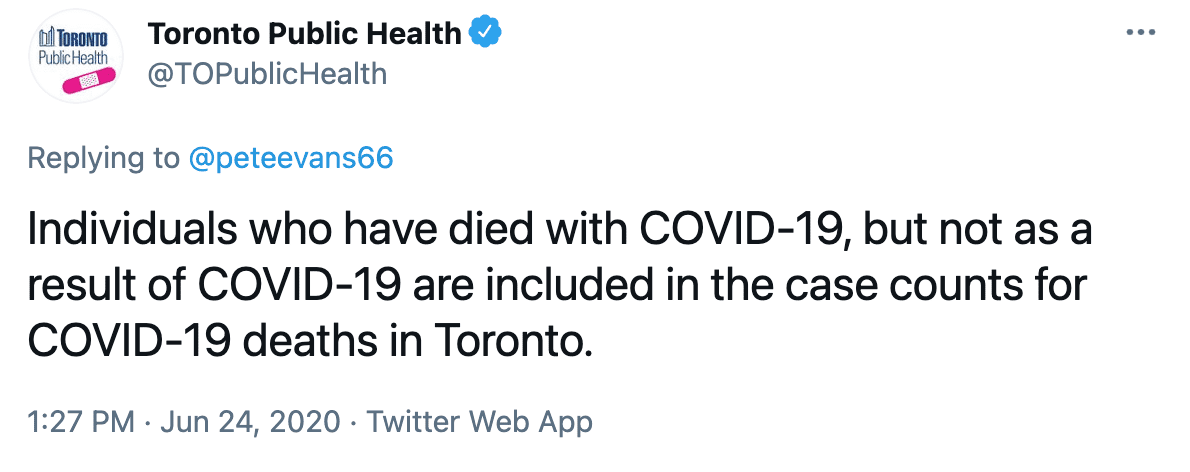

“Toronto Public Health continues to follow the provincial definition for how COVID-19 deaths are categorized,” said Dr. Vinita Dubey, Toronto’s associate medical officer of health. “This means that individuals who have died with COVID-19, but not necessarily as a result of COVID-19, are all included in the case counts for COVID-19 deaths in Toronto.”

Still don’t believe me?

Here’s their tweet…

The government is literally telling us that ANYONE who dies with COVID, but not from COVID, is marked as a COVID death. And they’re not even counting the number of those who actually died from COVID!

Is that not absurd?

Imagine if this news was made more prominent? Imagine if people simply started asking more questions…

So, where am I going with this?

Politics to Drive the Next Big Wave

After months of yet another lockdown in Canada, light is finally starting to shine on the extreme inaccuracies of COVID tests and inaccurate reporting – a test and reporting that have led to millions of lost jobs, depression, community divide, and trillions of dollars of debt.

So despite all that you were told by the government last year, such as, “just two more weeks of lockdown and we’ll be back to normal,” the truth is the plan was already in place to lock the country down again.

If you have been following the past issues of this newsletter, you would have seen this coming.

Via the Boldest Prediction of 2020, from November 2020 (before the resumed lockdown):

“It’s crazy to think that the entire world is willing and accepting of lockdowns based on the results of a COVID-test that is so highly inaccurate. This is fact and cannot be disputed.

Am I saying COVID isn’t something we should worry about? Certainly not.

But I am saying the numbers don’t add up to these severe economic and social global lockdowns being deployed.

…Prepare for another lockdown.“

Today, most of Canada is back on lockdown, while U.S. states who now consider Ct value in their public health response to Covid, such as Florida, are opening up.

Go figure.

So, it doesn’t matter if someone calls you an idiot, a conspiracy theorist, or any name being used to meme those who ask questions.

What matters is whose right.

Especially when it comes to investing.

The Next Big Boom

Over the past year, policymakers and governments have been telling us that there hasn’t been inflation.

Meanwhile, real estate and food prices have climbed, and materials such as lumber have soared.

No inflation, they say.

If you had listened to them, your savings and your money have already eroded.

This is why last month, I highlighted how inflation would pick up and gave evidence as to why.

Via Bigger than Bitcoin:

“…It doesn’t take an expert to see rising prices everywhere – especially where it counts: housing and food.

In the U.S., the average home is up 17%, with asking prices reaching all-time highs.

… In Canada, food prices are expected to go up by as much as five per cent this year.

Meanwhile, global food prices are surging and have now spiked for the tenth month in a row.

Get the point?

When you increase the money supply by such unfathomable amounts, inflation ultimately follows.

And while the powers that be can simply change inflation numbers by changing how it’s calculated, as the Fed just did by discontinuing the M1 and M2 weekly money supply series, average Joes still feel the pain.

Remember: Inflation is the ultimate destroyer of the lower classes. It is the primary power that separates the rich from the poor. The higher inflation goes, the bigger the wealth gap.

And that has been the plan all along…”

Is it surprising that just a few weeks after I published that Letter, U.S. core consumer prices rose at the fastest pace since 1981?

Despite that, the Fed and other policymakers continue to tell us that we shouldn’t be worried – that this level of inflation is transitory.

Yet, they all fail to mention rising prices in the three most important aspects of survival: food, shelter, and energy – all of which aren’t included in core inflation data.

While the experts continue to tell us that inflation isn’t an issue, I am telling you it is.

Because even though we’ve seen little inflation despite all-time low interest rates, the Fed has other ways to influence price outside monetary policy.

Deregulating Debt

Remember back in 2016 when Canadian and American real estate were red hot?

Despite everyone talking of a bubble, I suggested that the surging price of real estate was going to continue. Not because of interest rates or a better economy, but because of riskier loans…

Via The New Housing Bubble Just Began from 2016:

“Last month, Wells Fargo, the largest U.S. mortgage lender and third-largest U.S. bank by assets, finally admitted to “deceiving the U.S. government into insuring thousands of risky mortgages, as it reached a record $1.2 billion settlement of a U.S. Department of Justice lawsuit.”

Via Reuters:

“…According to the settlement, Wells Fargo “admits, acknowledges, and accepts responsibility” for having from 2001 to 2008 falsely certified that many of its home loans qualified for Federal Housing Administration insurance.

The San Francisco-based lender also admitted to having from 2002 to 2010 failed to file timely reports on several thousand loans that had material defects or were badly underwritten…”

With a $1.2 billion loss now on its balance sheet, Wells Fargo will have to make that back somehow.

That somehow turns out to be, well, more risky loans.

Via LA Times:

“Wells Fargo & Co. has started offering a new type of mortgage that requires a tiny down payment and could appeal to customers who might otherwise get loans backed by the Federal Housing Administration.

…Most big banks have pulled back from offering FHA loans after dealing with lawsuits and billion-dollar settlements connected with underwriting problems. Wells Fargo had been the exception, but with its new loan program, called Your First Mortgage, the San Francisco bank could soon be making fewer FHA loans.

… Your First Mortgage requires a down payment of just 3% of a home’s purchase price, smaller than the minimum 3.5% down required for FHA loans.”

They’re not the only ones offering these non-FHA, 3%-down, riskier mortgages.

Last week, JP Morgan announced the launch of a similar product.

…You know what that means?

It means that a customer can now put 0% down on a house, as long as the house is appraised at more than what the house is selling for!

The Bank of America also announced a similar program back in February.

… Here’s the punch line:

The top three U.S. banks by assets are now ALL participating in riskier mortgages.“

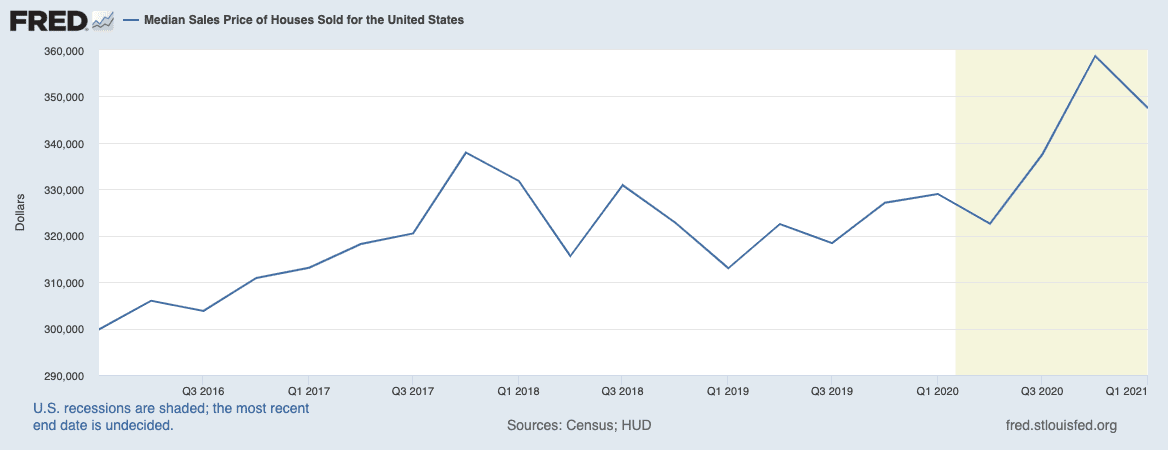

Did riskier loans lead to higher prices, despite interest rate hike expectations amidst an already red hot real estate market?

Here’s a chart of real estate prices in the U.S. since then…

Transitory My A$$

Now that you’ve seen how easy it is to manipulate real estate prices, what happens when the same playbook is deployed on consumer spending?

Well, we’ll soon find out.

“Some of the largest U.S. banks plan to start sharing data on customers’ deposit accounts as part of a government-backed initiative to extend credit to people who have traditionally lacked opportunities to borrow.”

In short, those without credit will now get credit – more importantly, credit cards.

This comes on the heels of consumer lending standards that have never been this loose since around the time records began in 1991.

Via Zerohedge:

“According to the Fed’s latest April senior loan officer survey released earlier this week, banks took a machete to their lending standards across the board for C&I, mortgage, credit card and auto loans (with the exception of CRE loans for construction and land development purposes).

…With the U.S. housing market a bubbly, frothy mess the likes of which have not been seen since the 2006 housing bubble, banks did their part to make it even frothier, and a net 6.3% and 19.0% of banks reported looser lending standards for GSE-eligible and QM-jumbo mortgages in April, respectively, up from net 3.2% and 1.7% in the prior January survey. As shown in the chart below, this is on par with the loosest resi mortgage credit standards since before the financial crisis! Not surprisingly as Americans scrambled to lever up and buy a house (or 2nd, or 3rd), the net share of banks reporting stronger demand increased to 12.7% and 19.7% in April from 6.5% and 6.6% in January, respectively.

…credit card standards have not been this loose since around the time records began in 1991, while auto loans are similarly among the loosest on record. This means that anyone that can fog a mirror is now eligible for a credit card!”

It goes without saying that throughout history, anytime debt has been extended, spending occurs. And those without credit are primarily low-income households, who almost always spend every bit of debt given to them.

I already showed you what happened to real estate in 2016 when the banks made it easier to get mortgages, during a time when the market was already red hot.

So, despite an already hot inflationary period, what do you think will happen when the banks make it easier to buy, well, everything?

The Commodities Supercycle

We need commodities to create the things people buy. And when people buy more, more resources are required to make what they buy.

It’s a straightforward concept.

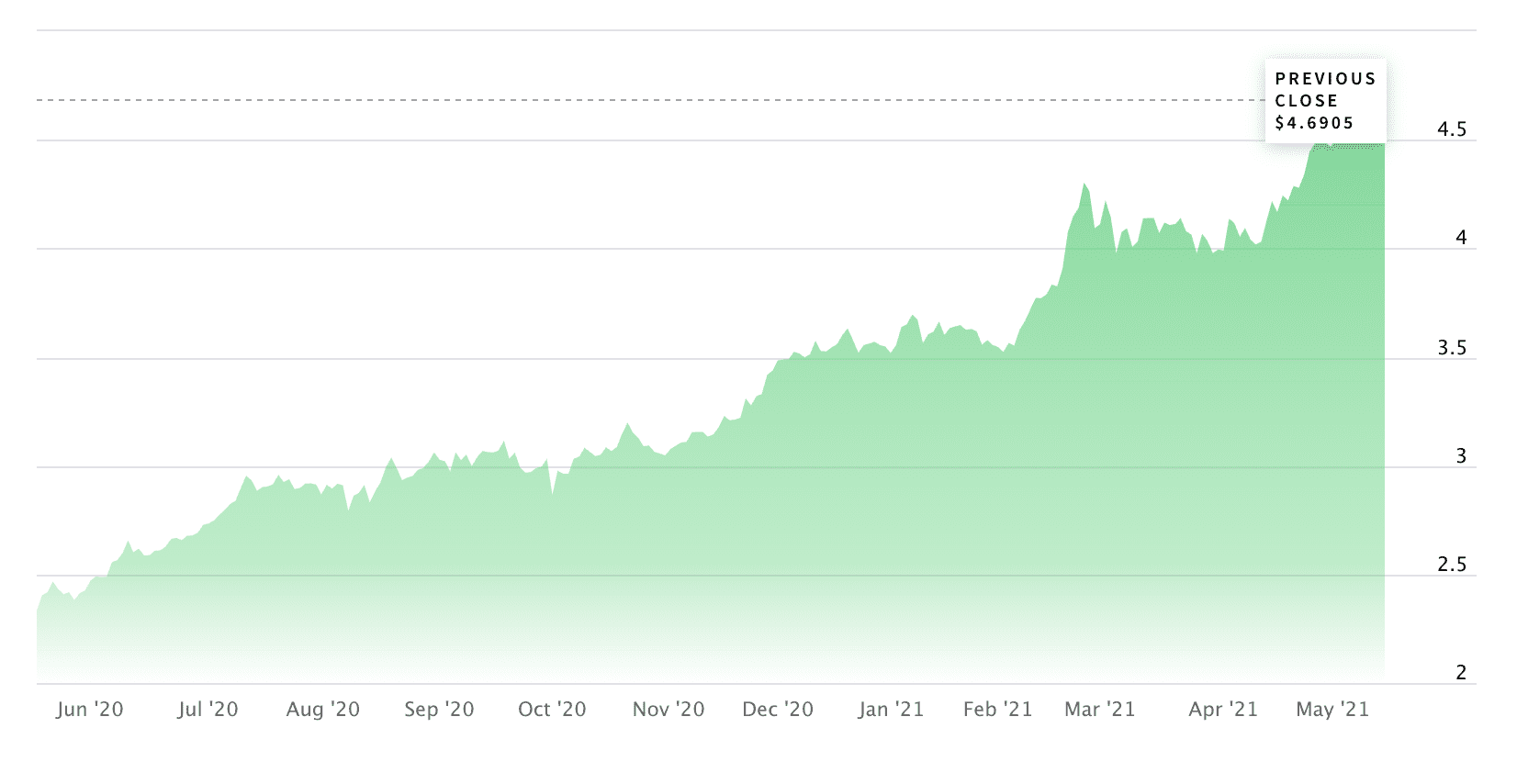

One needs to look no further than copper, the bellwether metal itself, to see why the next commodities supercycle could be here.

Last year, we said copper prices were going higher and then later gave readers a bunch of stocks to look at – many of which have easily doubled since then.

Via Copper and Copper Stocks Chart Analysis in November:

“We have looked at companies in the copper space, and there are lots to like. On the whole, many of these charts are expressing a true optimistic future outlook. Senior companies, FCX and SCC, have positive chart patterns. Mid-cap companies ERO and LUN also have a positive bias to their charts, as well. On the small-cap side, it sure looks like we may have found ourselves a very promising trade-set up in CS and CMMC.”

While many “experts” believe the rise in copper price is transitory, like inflation, I wholeheartedly disagree.

You see, not only are consumers about to borrow and spend like there’s no tomorrow, but many of the government policies around the world are calling for more infrastructure spending – a category of expenditure that relies solely on commodities.

Then there’s the whole global “green” push, which will require excessive capital expenditures and materials to fulfill. This includes everything from electric vehicles and the charging stations to power them, new power grids, and other green initiatives such as upgrading existing buildings to achieve maximum energy efficiency.

None of these goals will be achievable or sustainable without the creation of more metals.

And when it comes to copper, the costs of building a mine are so high that copper producers won’t build them unless prices are sustainably higher. If any of these “green” goals are to be achieved, demand will most certainly outstrip current supplies, leading to even higher prices.

This goes with almost all base, precious, and rare earth metals – with precious metals playing a role in both economic growth while acting as an inflation hedge.

Could this commodities boom be derailed? Sure. But that would likely mean a complete reversal of government policy.

Could we head into another recession? Sure. But global economic competition is so fierce, especially amongst China and the U.S., that I don’t foresee that happening just yet. The big players have too much to lose at this stage in the game.

Conclusion

Whether it’s COVID or inflation, we should always be asking questions.

We should never simply “trust” the system – and especially not the governments.

They have been telling us that inflation isn’t a concern for over a decade. Yet, the cost of living is higher than ever. Imagine if you bought a house ten years ago instead of trying to buy one today.

The same goes for COVID.

It’s crazy to think that there are so many rushing to receive experimental vaccines without asking questions – especially vaccines that don’t even prevent those who take it from getting COVID.

Just ask the New York Yankees.

Via NBC:

“New York Yankees shortstop Gleyber Torres has tested positive for COVID-19, the team confirmed Thursday afternoon, after being fully vaccinated and previously having been diagnosed with the virus in the offseason.

Torres becomes the eighth member of the Yankees to test positive this week — all of whom were fully vaccinated.”

Never in the history of civilization have we forced vaccines to those who are not at risk. And the data clearly shows that people under 50 have a very slim chance of dying from COVID – this doesn’t even factor in the misinformation based on how a COVID death is determined, as per Toronto, for example.

So if everyone at-risk takes the vaccine, why do those not at-risk have to take it?

It’s time for me to ask you some questions.

Have you read any of the research on these COVID vaccines?

Do you know the difference between all of them?

Do you know the side effects?

Most importantly, do you know the long-term side effects? This one I can answer: No one does.

Is there a lot of science behind these vaccines? Absolutely. But science is rarely black and white and is constantly changing.

How many drugs have been recalled or banned after years of use? Consider that, on average, about 4,500 drugs and devices are pulled from U.S. shelves each year.

Now consider that the COVID-19 vaccines took less than a year to develop – the fastest vaccines ever created. And there are many of them.

Do you know the fastest vaccine created before that? The mumps vaccine. It took four years. And this was in 1960. Despite all of our technology and new science, not one vaccine has been created faster since then – except for the COVID vaccines.

Doesn’t that make you wonder?

Yet, everyone is rushing out to get their jabs.

Such is the world we live in today – a world where people are no longer asking questions.

Before making your next decision, be it investing based on inflation data or taking the vaccine, ask yourself this: have you ever met a politician who never lied?

They’re telling us the vaccines are safe after only one year of testing.

And now they’re telling us once again not to worry about inflation. Will you “trust” them again?

I won’t. That’s why I am preparing to invest in the next commodities supercycle now. Remember, during every commodities supercycle, there are small-cap stocks within the space that see the same crazy gains as we have witnessed with cryptocurrencies.

Get ready.

Seek the truth,

Ivan Lo

The Equedia Letter

Equedia.com and Equedia Network Corporation are not registered as investment advisers, broker-dealers or other securities professionals with any financial or securities regulatory authority. Remember, past performance is not indicative of future performance. This article also contains forward-looking statements that are subject to risks and uncertainties that could cause actual results to differ materially from the forward-looking statements made in this article. Just because many of the companies in our previous Equedia Reports have done well, doesn’t mean they all will. It’s your money to invest and we don’t share in your profits or your losses, so please take responsibility for doing your own due diligence and consult your own professional advisers before investing in or trading in the securities mentioned in this newsletter.

a fascinating read and looking forward to the comments. Thx you

TOTAL DEATHS IN CANADA. WHO CARES?

TOTAL NUMBER OF NEW CASES. WHO CARES?

I WANT TO KNOW WHAT IS BEING DONE TO REDUCE THE CHANCES OF CATCHING THIS VIRUS AND HOW SOON BEFORE WE ARE “ALLOWED” TO RESUME SOME FORM OF SANITY!

CANADAS’ RECORD OF VACCINATING IT’S PEOPLE IS ABYSMAL AND THIS PRIME MINISTER SHOULD BE HELD RESPONSIBLE FOR IT!

To more accurately determine how many Covid deaths, you need to look at total deaths for time period versus the expected number from previous years. I think most numbers will show a much greater overall death count which can only be attributed to Covid.

I am of the same mindset on the total death count per se. My opinion is that death is a process and as such can be measured and monitored and tested statistically. We have 2 six-sigma events that have occurred over the COVID time period 1 negative (i.e. COVID) and the second positive (influenza). If we take the death outcomes of the time period before COVID hit and test it against the COVID period that will be the actual death rate, but it will be confounded by the lack of influenza deaths because of the mass usage of hand sanitizer, hand washing and masks. So we will get a sense of the effect after the fact but it will still only be a sense and not an actual. My take on the influenza effects is that from here on, it will likely be muted because the benefits of the masks, and hand maintenance is likely to continue.

Thanks Robert. Great call. Let’s do that also – if you take a look at the charts, for example in Canada, you’ll see that overall deaths haven’t changed much, if at all. https://www.statista.com/statistics/443061/number-of-deaths-in-canada/

As usual, you parrot all the right wing taking points using some half truth (or just omitting stuff) based on the one or 2 doctors whose ambiguity(or your willingness to pick and choose what they say) can used to support your positions VERSUS the tens of thousands of NON governmental doctors whose positions are pretty clear(to the extent that the science always evolves) and dont agree with you.

(1)Lockdowns were not instituted only(or even principally) because of testing(PCR or otherwise) but

because hospitals were filling up with sick Covid patients(I know you think this was a hoax-but

both in the NE and in the SE where I live this happened at different times).

(2)Most people(school children in particular) have a very slim chance of dying from measles or mumps or a variety of other diseases, but these are still”forced” on them to prevent lots of harm to them and

others(short of dying). Of course non vaxxers like you may be dont care.

(3)There is a chance that someone 18-49(with no underlying conditions) can still get sick(without dying) and /or spread the disease to others.

(4)The JNJ vaccine is only known to be effective 60% VS 95% for Moderna and Pfizer. Its no

surprise the Yankees got sick-the surprise is that they used JNJ in the first place,

(5)This is 2021 not 1960, Science is far more advanced now. No new vaccines lately as fast because

no new pandemics lately that required them(and the money needed for the speed) There has never been any known long term effectsto any vaccine(plenty from new drugs like thalidomide) so why should we assume the negative rather than the positive

(6)You may be the worlds foremost authority on inflation-but if you are, did you say 5 years ago

there would be zero inflation for the next 5 years? It is quite possible (even probable) there

will be inflation (above 2%) in the next few years, but the last few tears have shown that no one can

be certain what will happen(by the way ,back in the 60s 2% inflation was considered bad)

Great, let’s have a discussion! Let me start by rebutting your points.

Your first point, one or two doctors that you mention:

What one or two doctors are you referring to, and in reference to what? PCR tests? If so, the way PCR tests work is not an opinion – it’s just how it works. PCR test have Ct values and the Ct value used is the most important part of the test. Not considering Ct value is akin to taking your temperature without the numbers. Furthermore, with regards to vaccines, hundreds, if not thousands, of doctors around the world are trying to promote Ivermectin instead of vaccines. There are petitions from thousands of doctors/scientists/etc. to stop the vaccines and the lockdowns.

Your points by numbers.

(1)Lockdowns were not instituted only(or even principally) because of testing(PCR or otherwise) but because hospitals were filling up with sick Covid patients(I know you think this was a hoax-but both in the NE and in the SE where I live this happened at different times).

Overall, hospitals – especially in Canada – were never overrun. It may appear that some had a few cases of this, but that’s in relation to how COVID patients need to be isolated. As such, there aren’t as many beds available. Second, you haven’t factored in fear – those who have been hospitalized may not have needed to go to the hospital, but out of fear, they do. The media talks about ICU’s – this causes people to think that all of these patients need Intensive Care. When, in reality, many are in ICU’s because the ICU’s have isolated rooms to prevent the spread – regardless of how sick someone is. Lastly, why have all of the “pop-up” emergency COVID tents been removed? Because they weren’t being used. You sound like you live in Alberta – just ask Alberta why they shut down those tents. Because they were completely empty.

(2) Most people(school children in particular) have a very slim chance of dying from measles or mumps or a variety of other diseases, but these are still”forced” on them to prevent lots of harm to them and others(short of dying). Of course non vaxxers like you may be dont care.

First off, when did I say I was an anti-vaxxer? Second, this is a simple one to answer. Children ARE at risk of mumps developing into something serious and even death. So you are wrong. I have three boys, two really young – they get their shots because the shots they receive are to prevent them from getting really sick from these diseases. So yes, the children are at risk for the diseases their vaccines are meant to prevent. The COVID data for children getting really sick are extremely, extremely rare – if they exist at all.

Lastly, I am not anti-vaxx. I am just not going to be a guinea pig.

(3)There is a chance that someone 18-49(with no underlying conditions) can still get sick(without dying) and /or spread the disease to others.

There is also a chance someone who is 19-49 and vaccinated, can still get sick and spread the disease to others. To my point, if those over 50 are vaccinated, then they should be protected, no? Especially if, as you highlighted, the Moderna and Pfizer vaccines are 95% effective. Why do they have to worry if the 18-49 can give it to them?

(4)The JNJ vaccine is only known to be effective 60% VS 95% for Moderna and Pfizer. Its no surprise the Yankees got sick-the surprise is that they used JNJ in the first place,

I think you need to do more research here. Feel free to define effective rate, because those numbers are not only ever-changing, but were conducted on an extremely small subset of people.

(5)This is 2021 not 1960, Science is far more advanced now. No new vaccines lately as fast because no new pandemics lately that required them(and the money needed for the speed) There has never been any known long term effects to any vaccine (plenty from new drugs like thalidomide) so why should we assume the negative rather than the positive.

Sorry, this is where everyone gets it wrong. First, “there has never been any known long term effects to any vaccine.” That’s a completely false statement. There’s plenty of research showing negative effects. But that’s not point. Feel free to start here: https://www.cdc.gov/vaccinesafety/concerns/concerns-history.html, and here https://www.immunize.org/timeline/, and here even https://www.ncbi.nlm.nih.gov/pmc/articles/PMC2870557/

Second, it isn’t about how much more advanced we are – vaccines take a long time to develop because they need to “observe” long-term effects. That’s the most important part. Now we’re giving out not only experimental vaccines, but experimental techniques too (MRNA) without this observation. It really is simple as that – regardless of what technology is available now. You can’t speed up time – unless, of course, Pfizer or Moderna have a time machine? As the old adage goes, “time is money, but money can’t buy time.”

(6)You may be the worlds foremost authority on inflation-but if you are, did you say 5 years ago there would be zero inflation for the next 5 years? It is quite possible (even probable) there will be inflation (above 2%) in the next few years, but the last few tears have shown that no one can be certain what will happen(by the way ,back in the 60s 2% inflation was considered bad)

I am certainly not the foremost expert on inflation. However, yes, I said (can’t remember exact time, maybe 5 years ago?) that inflation, as the government/bankers tells us, would be low despite true rising prices, in the context of how they can manipulate prices via the financial market. I have actually been quite accurate about this and gave examples of how inflation data is not only manipulated, but how true inflation has been occurring – there are many past Letters on this.

Please feel free to rebut any of my comments above. I do wish to say thank you for your comment because you helped prove my point: I raised a subject, and you called me an anti-vaxxer and called my points “right wing.” My kids are immunized, so no, I am not anti-vax. How does wanting more research on COVID vaccines make me right wing? What is political about that?

Thank you for your comment and the opportunity to respond.

I agree with your view on copper. The Fed always was a corrupt idea to provide protection for the banking industry and the rich.(socialize the losses, privatize the profits) COVID is a disease. I avoid it and anything that is related to it.

I started reading your letter right from the first 1 in my mailbox. One reason being your use of independent research. I agree totally with the idea that today asking a ? is a minefield. I respect your point of view based on Present science that the PCR test is used as the Gold standard. But at the amplification rate used it can detect fragments that are so small they have 0 chance of growing into a full blown infection. I say this because I have been hearing this from scientists and Doctors over the past year. You are not an idiot or anything else derogatory that people may say. As I said I respect your view point and the research you do. Just today I saw on the CBC an older lady, not elderly, putting her small bungalow on sale for 1.8 million. Guess where? Vancouver. But there is no inflation!!

Well said Timothy! Thanks for your readership and comment. There’s no inflation, yet we’re all paying higher taxes on everything we buy – go figure!

Apparently, there is a great shortage of pure copper, and this is why copper pennies were to be removed from currency, and became obsolete. The elite are needing more copper to build more 5G towers, weather it’s true or not??………you may still find some articles o this.

How come Big Pharma don’t ever try to find a cure for anything? How come it’s only vaccines they are after?

Every day it gets clearer if one looks that the alleged covid virus was invented for the covid injection

God help us all

See this article from Science, Public Health Policy and the Law Vol 2:4-22 October 12, 2020. It is a very good explanation of how the CDC altered the reporting methodology to massively overreport Covid mortality.

https://www.ratical.org/PandemicParallaxView/C19dataCollection-C+FL-HistPerspec.pdf

Thanks for always seeking the truth!