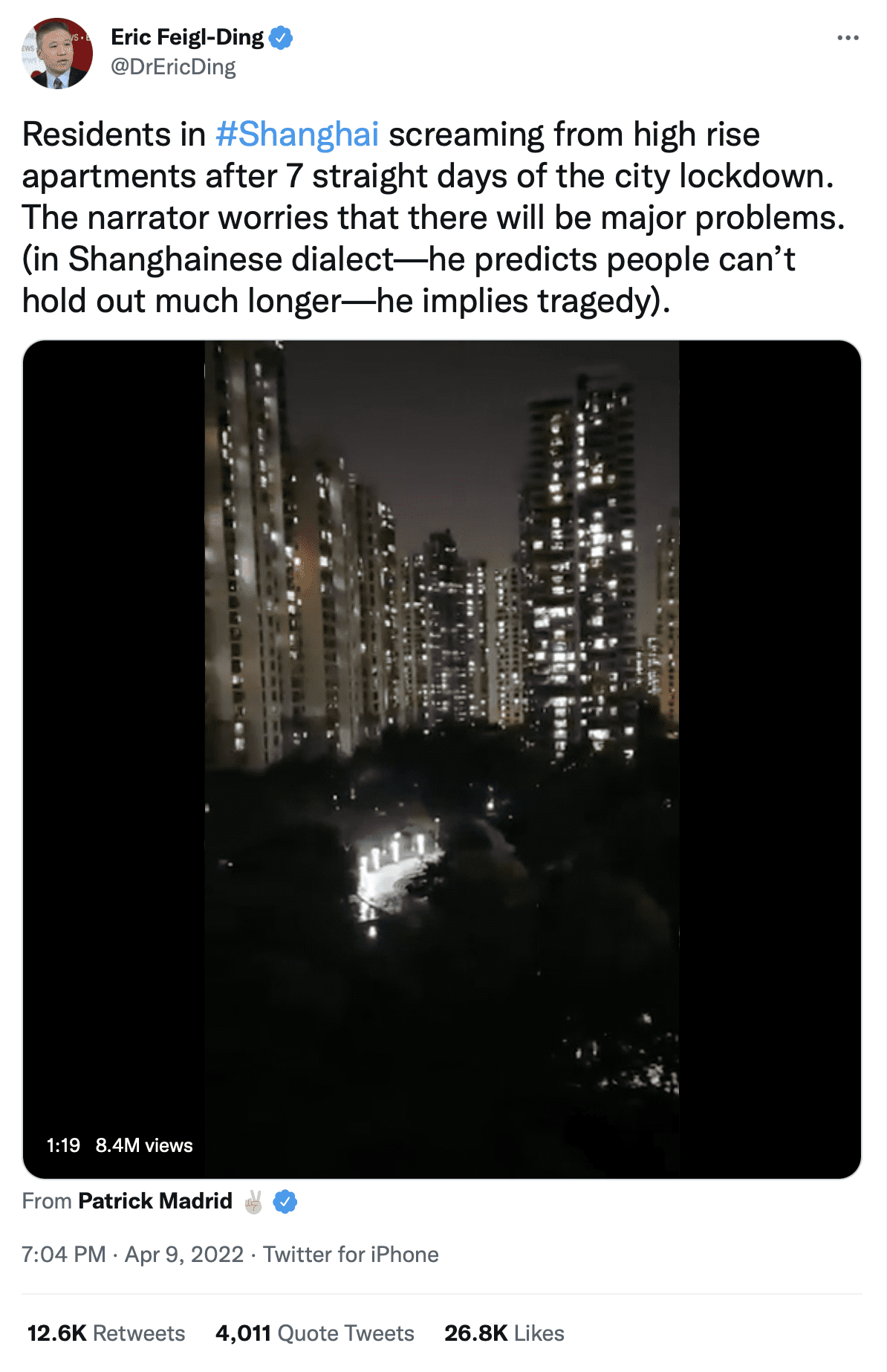

Last month, China revealed its authoritarian regime in full color. In pursuit of its “covid zero” policy, it put its second-biggest city, Shanghai, in total lockdown. For a month now, 25 million people have been locked up with limited food, medicine, and other supplies.

Like sci-fi cops, drones and robot dogs equipped with facial recognition tech are zipping around the city. They are ordering residents to “control the soul’s desire for freedom” and comply with lockdown rules.

Those who don’t obey are evicted to” quarantine centers.” They lose their social credit scores. And, according to a taken-down popular Twitter account, some are “fined directly from digital CBDCs [central bank digital currency] wallets.”

Shanghai is a real-world example of Big Brother.

It shows the unthinkable control the state can exert by quietly centralizing enforcement. And, how little by little, it can take away everything from you: from money to basic human rights.

Most important, they do it slowly, so you don’t bat an eye until it’s too late. And if you think it’s just China, think again. Just take a look at Quebec not long ago, when they tried to ban people from walking their dogs passed 10pm!

The End of Fiat = Full Government Control

Have you noticed the sudden hurry of central bankers to explore CBDCs? Could a CBDC USA be coming?

Shortly after China’s e-yuan launch, the Fed went to MIT to develop its own digital currency. They call it “Project Hamilton” (which is funny, and I’ll tell you why later).

This February, MIT released the Phase 1 prototype.

Then Biden signed an executive order urging the nation to prepare for a digital dollar rollout in case it’s “deemed in the national security interest.”

Later, Treasury secretary Yellen touted it as a vital step to secure America’s financial dominance:

“The development of our currency to its current form has been a dynamic process that took place over centuries. Today, monetary sovereignty and uniform currency have brought clear benefits for economic growth and stability. Our approach to digital assets must be guided by the appreciation of those benefits…Some have suggested a CBDC could be the next evolution in our currency.”

You can’t make this stuff up. Do you really think the timing of this is a coincidence? Do you really think everything is still a conspiracy?

Remember, Ivan called this many, many years ago.

Via “Is Bitcoin the New Stimulus?“:

“…there could be a reason why governments around the world are letting cryptocurrencies run rampant:

-

-

- To temporarily infuse free money into the system “off-the-books”.

- To implement Cryptocurrencies on their own once the technology is proven and accepted (or once it fails and they step in to save the day).”

-

So don’t think CBDCs are just a power play between China and America.

In March, MIT reached similar agreements with the Bank of Canada and the Bank of England.

Just ask Canada’s Liberal party, whose 2022 budget contains an allotment for CBDCs.

But that’s not all.

A recent report by the Bank of International Settlements (BIS) showed that nearly all central banks are building their own CBDCs:

“Nine out of 10 central banks are exploring central bank digital currencies (CBDCs), and more than half are now developing them or running concrete experiments… Globally, more than two thirds of central banks consider that they are likely to or might possibly issue a retail CBDC in either the short or medium term.”

Let that sink in for a moment.

A CBDC is no longer a far-fetched idea in some “future of money” TV segment. Lawmakers are explicitly hinting at the looming change in global monetary order; we are shifting away from fiat currencies to state-issued digital currencies.

And this marks the final step in the complete centralization of money that started in 1913.

From “National Bank Notes” to a Digital Dollar

With each monetary revolution, the state has gained more and more power.

Before 1913, money in America was issued by thousands of banks in the form of “national banknotes.” Then the Fed came along, introduced the unified currency, and monopolized its creation.

Still, its hands were mostly tied because Fed notes were backed by a real asset—gold.

Then Nixon took the dollar off the gold standard, and the dollar became a fiat currency. Because fiat notes didn’t need any collateral, the Fed could print them at will.

And we already know how it used that to its advantage.

Even so, the fiat system didn’t give the government absolute monetary control. That’s because the Fed can’t distribute and control fiat dollars outside bank reserves.

As I wrote in “The Biggest Dealer in the World”:

“The Fed doesn’t create most of the dollars that circulate in the economy. It’s the private sector—commercial banks—that do. They use monetary engineering called fractional reserve banking…

Central banks play an important role in this chain. They keep tabs on commercial banks, hold their reserve cash, and inject money when liquidity dries up. But it is commercial banks that multiply the dollars and shove them into the economy…”

So, while the Fed can print up as many dollars as it wants, it is at the mercy of private banks, wh0 may choose to keep the money to themselves*. Just as they did after the Great Recession.

*of course, these private banks are still governed by the rules set by the Fed.

But this is where the digital dollar comes in.

CBDCs Aren’t Cryptocurrencies

Policymakers often spin a digital dollar as a safer, state-backed alternative to cryptocurrencies. Yet, apart from the digital “wrapper,” it’s nothing like a cryptocurrency.

Take Bitcoin.

It’s a digital currency governed by an open-source software called a blockchain. It’s a distributed ledger system that has hard-coded rules in it that are enforced by millions of miners instead of one central authority.

Most important, anyone can change those rules – even you – as long as there’s a majority approval.

For example, Bitcoin had a number of changes to its blockchain (aka forks) when the majority voted in favor. They added new features and fixed Bitcoin’s weak points that surfaced after its wider adoption.

In theory, people could debase Bitcoin like the dollar by removing its core feature: the hard cap of coins available. But that didn’t happen because it’s not in the interest of Bitcoin holders to devalue their asset.

This is what a purely democratic monetary policy looks like.

No politician or elite hiding behind lobbyists can influence it because it’s literally those who hold the money that makes the decisions. And if there’s change, it actually represents what the majority wants.

It’s like an open-source Fed.

Meanwhile, a CBDC is 100% controlled by the issuing authority, in this case, the central bank. So the issuing bank can mint as many tokens as it wants and do whatever it wants with them with no oversight.

In fact, a recent 35-page Fed report and Boston Fed’s Project Hamilton Phase 1 summary confirm our worst fears:

- The digital dollar wouldn’t be built on a decentralized blockchain. Instead, it will be a centralized system controlled by the Fed:

“Despite using ideas from blockchain technology, we found that a distributed ledger operating under the jurisdiction of different actors was not needed to achieve our goals. Specifically, a distributed ledger does not match the trust assumptions in Project Hamilton’s approach.”

- There will be no privacy. The proposed system will have a record of everything you spend your money on, and that data will be exclusively available to the Fed.

- Not only that, the Fed will be able to bypass the banking system, and there’s not a single word about any auditing or oversight from other agencies (just like the Fed today.)

And the worst thing is, the digital dollar could be programmable. That means the Fed can introduce rules that regulate money in circulation and change them at its discretion in real-time.

Think Trudeau freezing the truckers’ bank accounts without enacting the Emergency Act.

Even worse, think Trudeau deleting all of their life savings…

Ethereum Goes Dictator

If you follow cryptocurrencies, you’ve most certainly heard of Ethereum’s “smart contracts.”

In the simplest terms, they are “clauses” programmed directly into tokens that trigger an action when certain conditions are met. For example, it can deduct money from your wallet when it comes time to pay interest on your loan.

The difference between legal agreements and smart contracts on a blockchain is that smart contracts are self-enforcing. So you don’t need a bank, a court, or any other third party to enforce those rules.

What makes this system democratic is that these contracts are transparent and immutable by default. And their fulfillment is backed by a decentralized blockchain governed by millions of people.

Policymakers are actively tossing around the idea of making CBDCs programmable, just like Ethereum.

Via the Telegraph:

“Tom Mutton, a director at the Bank of England, said during a conference on Monday that programming could become a key feature of any future central bank digital currency, in which the money would be programmed to be released only when something happened…

A digital currency could make payments faster, cheaper and safer, but also opens up new technological possibilities, including programming: effectively allowing a party in a transaction, such as the state or an employer, to control how the money is spent by the recipient.”

And they often compare it to Ethereum’s smart contracts, as if that’s some kind of validation:

“Earlier this month, Sir Jon Cunliffe, a deputy Governor at the Bank (of England), said digital currencies could be programmed for commercial or social purposes, even down to the way children spend pocket money.

He told Australia’s Sky News: “You could think of smart contracts in which the money would be programmed to be released only if something happened.”

But when smart contracts are built into a centralized system, they are no longer immutable. The powers that be can simply override the rules at any moment.

For example, the government can suddenly deduct a “tax” from your savings to fight climate change.

Or punish the unvaccinated with “health insurance surcharges.”

Or even straight up freeze digital wallets to censor opinions…

In other words, the programmable digital dollar is the ultimate enforcement system. And if, God forbid, it becomes the only legal tender, it would mark the end of any financial freedom there is left.

America’s First Treasury Secretary’s Dream Comes True

I’m going to end this letter with a chilling historical connection.

Call it a conspiracy, or coincidence, but the Fed’s digital dollar project is named after Alexander Hamilton—America’s first Treasury Secretary who served during George Washington’s presidency.

He was a diehard autocrat who believed that inequality was “the great and fundamental distinction in society.”

And that order in society, in effect, hinges on the elite.

As such, his policy aimed to tie the federal agenda to the interests of wealthy Americans.

And, surprise, surprise, he was the first to toss around the concept of a centralized banking system.

The Fed doesn’t often show its creative side, but damn, what a catchy name for the most autocratic enforcement system in America’s history.

Hamilton must be smirking in his grave.

I strongly urge you to forward this Letter to as many people as possible. Otherwise, CBDCs WILL happen.

Choose your leader accordingly, or you may soon have no choice.

Seek the truth and be prepared,

Carlise Kane

I

I’ve always believed in “human progress”; as a former teacher how could I do otherwise? After all, we grow and learn, move from Gr 1 to Gr.12 and beyond. Our huge blunder resides in devoting ourselves to “outer” or material growth instead of “inner” or spiritual growth, ie, learning how to not only accept ourselves and others but appreciare others, learn from others. Here’s my summary statement after years of contemplation and life experience: “The Whole is greater than any part, no matter how beautiful or essential the part may be,”, a philosophy I call “Full Spectrum Living”.

After reading this I’m glad I’m 77 and not 7 years old.

I’ve been wondering for years, when is our currency going to collapse?What gives anything any value? For the most part how everything works when it comes to these issues is way above my ability to comprehend.

I recently turned sixty, my wife and I have decided to sell everything we own and move to Mexico. Very excited to cash out of the real estate market at the top of the recent up swing. However I’m at a loss how to protect our savings. My biggest fear about moving to Mexico is what are we going to do when our Canadian dollar is worthless?

The whole idea of a digital currency is so scary to me. Governments around the world have proven how corrupt and incompetent they are but societies continue to be blindly led down the path. It’s unbelievable to me that so many people trust the governments of the world. To be in a situation where your government has the ability to control YOUR savings and how and where you can spend YOUR money is so absurd to me. Who the hell in their right mind would sign up for such an arrangement?

Love to hear any suggestions on how one can possibly protect my assets.

Steve.

scary stuff. Would you consider yourself a socialist? Or “Marxist”/communist in ideals? Not meaning to just throw out labels here… serious question.

There isn’t a snowballs chance in hell that the present liberal government in Canada or, for that matter, any future government, will be smart enough to manage a CBDC system. This particular government won an election based on the socks and “cuteness” of a guy barely intelligent enough to dress himself. Our future as a country is already at stake because of the Liberals and this digital currency scheme would drive us further down the rabbit hole!

Good questions… and thought. My thinking is to try to buy land (wherever there is water supply and decent growing seasons)… on which to live on and grow your own food (perhaps a couple goats and chickens or ducks if you’re not all vegan?). I’m now 52, and that’s what my wife and I are considering/hoping to do with her Mom… fairly soon!

Easier said than done, I know. Especially as we age. But we’re also hoping our young (now adult) sons will see the value (and soon need?) in “homesteading”… again. Peace.

I totally agree, this would be great .As long as you don’t use your CBDC wallet to purchase seeds to grow your own food and not purchase the food from a government authorised distribution centre. Trading items with your neighbours without cash like it used to be, sacks of vegetables for a sheep.

While I think you’re beating this drum in a distant forest, I hope you continue. I’ve foreseen the things you say for about 5 years already, but not a single person I spoken to believes this is coming or what it means for our lives – even after the evidence of Trudeau’s tyrannical conduct during the trucker’s protest. My expectation is that as long as the government’s follow ancient Rome’s tactic of providing ‘bread and circuses’, or in today’s context, ‘stimmie cheques’ and ‘political drama’, almost the entire populace will allow the governments to do what they want. When the goodies can no longer be provided, we will hopefully revert to another historical period, namely the French Revolution, when the people simply rounded up their leaders and ran them through the guillotine. I say hopefully because we might also just keep slipping further and further into the mire until all our countries are like North Korea. I fully agree with Andy, who is glad he’s 77 and not 7, as I also wouldn’t want to live in the conditions we soon will be. Seems rather unfortunate that gene editing techniques can’t be used to identify potential politicians and cause them to self-abort before they’re even born.

coitus,coitus and double coitus…………i am 75……born in europe at the end of ww 2…….understand what fiat money can mean to survival in a time of crisis……yes i am old school…..have gold,silver.art,land,collectibles etc. that are supposed to get me and mine through a crisis……..unfortunatly the bulk of assets are sitting in banks and the stock market….yup that CBDC is going to throw a royal coitus in my plans for survival for me and mine……and forwarding this message to people is just the second means of flagging my political bent….the first is me reading this piece…….hello china and the various feds you are showing the world the allegory(of 1984) of how to control most people who are basically sheep…sorry for the rant and the six letter words

Damned if you do and damned if you don’t:

The very anonymity and privacy that makes Bitcoin and other digital currencies attractive is also it’s biggest downfall in my understanding. It allows the criminal element to take advantage and either launder ill gotten fiat currency or it allows the manipulation of the price by the bigger players who move money in and out of the market in a similar way that the stock markets are manipulated by those same big players.

At least with a Central Bank controlled digital currency some of this activity might be regulated.

My understanding of the move to fiat by Nixon is that they needed to grow the economy in lockstep with the growth in population. By printing money as required they were able to achieve that end. and avoid market fluctuations/volatility in the price of goods and services and ultimately control extreme inflation and deflation events.

Its a very scary thought that the world is being hijacked into a total police/ government ruled civilization. This is all part of their total reset which bottom line means the end of freedom. You have no say or choice in anything. And its being implemented right now without the population having to vote for or against it . I see and hear a lot of rejection against it in the media but no physical alternatives to fight against this. I believe that there will be a massive uproar against it once it is thrust upon us, but a collective unified stand against this, as was done against the Cov-19 must be enacted now.

Control of personal finances is ludicrous, that would allow your personal habits to be charted and given a score based upon their societal norms. No individuality. Its literally terrifying…

I think this is just the FED playing defense in the mist of all these new digital cryptocurrencies & blockchain technologies emerging. Since the $ remains the world’s reserve currency today & the FED controls the monetary & financial systems, they are still the only game in town & want to remain so. By doing some research & experimentation into CBDC, it becomes a backup plan should one of these new cryptocurrencies & blockchain tech’s really start to challenge the $. Micromanaging everyone’s assets becomes apart of the solution should they have to implement the backup plan, but not really the goal here, protecting there supremacy status is # 1.

Makes wonder if this isnt the reason the XRP cryptocurrency is facing such a huge wall of resistance. It facilitates money transfer but cannot be controlled by any one entity. Since the dawn of time, it has been proven that corruption wins over truth and the righteous. Why? Because they understand the majority are sheep and lemmings. I mean seriously, think about it. They are outnumbered 7.49 billion to 10 million. Where in the war of worlds would those odds lose?? Here on earth, lemmings and sheep are no match for the human- landlords of the world.

“Damn” is right! Great article Carlisle. Thank you. Forwarding on (to those awake/enlightened enough) now.

Loved how you used phrases that would serve to stir fear and anger in conservatives, like “deduct a ‘tax’ to fight climate change” and “punish the unvaccinated by charging them ‘health insurance surcharges’.” There’s even an implied threat that funds could be frozen as a way to “censor opinions.”

And, of course, the CBDC program is named after an “elitist!” Face it – more than anything this is a political ad. It’s your way of planting the idea of a progressive government “bogey man.” I hate to clue you in, but your transactions are already known if you use any modern “centralized” way of paying for anything. And the IRS can already garnish your bank account or wages if you owe back taxes.

Also you’re already being spied on by your cellphone, Facebook, Google, the DMV, and a host of other agencies – both governmental and commercial. The only reason you’re making this sound so raw and threatening is that your trying to influence how people feel toward certain factions of their government. You’re using the old playbook of fear with a high-tech twist. Hey – whatever works, right?

Rest assured that the only scary outcome from your fear-mongering is another possible assault on an American institution. I mean really: you’ll be punished unless you take action! How about “Go fuck yourself!”

Whoa Michael… Whoa. Calm down sir. 😉 I agree that all you referred to could be construed as “fear mongering”… and could further trigger “conservatives” (who take a hell of a lot to trigger historically… comparatively). Not sure what you’re referring to in using the phrase “another possible assault on an American institution”… unless you actually consider the events of Jan. 6 an “insurrection”? The very meaning of the word “conserve” is to desire to uphold the time-tested “institutions” of the greatest country the world has ever known (and I don’t mean in regards to military might or financial opulence either; I’m referring to the freedoms/opportunities granted to every individual that ever had the privilege of being one of it’s CITIZENS; this coming from a man who was born and raised in Canada… and raised three sons there too). If “we” (that’s a collective usage there) should “fear” further destruction of America’s “institutions”… it is “feared” from the uneducated and/or uninvolved (civically or economically: employed and tax paying) “Left” (NON-conservative “types”). The burning of courthouses, looting of local/neighborhood businesses, murdering of police officers, tearing down of founding father statues, disrespect of the flag and national anthem, indoctrinating sexual confusion and unscientific “safety measure” in the schools… I could go on, unfortunately. Most of whom have not the least interest in preserving THE constitution of the United States of America. While not perfect, has proven to be the greatest in the history of this small world. Any disagreement? If so… do tell.

The only real advantages to a democratically designed Block Chain digital currency(BC), is to the authority designated to collect taxes and in the USA 95% of the Taxpayers. (I’m not suggesting that the authority would or should have the ability to immediately “Glom” any tax owed).

Citizens or non citizens would be given digital credits based on what they put in during a “Transitioning” period to a $Digital currency. Assets that are stated would be worth their parity value in BC. If you don’t declare cash or other fungible assets they’re worthless to you. If one enters one’s net worth in an honest fashion, one stands to lose nothing.

There isn’t enough gold, silver rare earth Elements in or on this planet to cover all the wealth gold has created, so pegging the value of a fiat currency to its GNP is not a bad idea for judging the wealth of Nations..

95% of Individual taxes would go down as it isn’t fabrication to assume that 5% of wealthier citizens are taking advantages of illegal methods of not reporting income or net worth; this would be very difficult to do in BC reporting. Theoretically, the government would have a larger tax pool to pay its bills from, so those who are the 95% of citizens would pay less or get a rebate. Of course, governments being governments, would have more money and instead of a rebate might put the additional fund to some cockamamie projects too, but that’s what legislatures are for when used according to their authorized Constitutions.