The concept of buy low and sell high could not be easier to understand.It is the single most important rule when it comes to investing. Yet, it is also the hardest rule to follow.

Just ask all of the bagholders who thought it was wise to buy Gamestop up to $483 – when shares were less than $20 just a few weeks earlier.

I understand the hate toward Wall Street short-sellers. In fact, I wholeheartedly agree with them – those who have followed this newsletter have experienced this pain.

Many years ago, we tried to beat a notorious short-seller who shorted one of the stocks I was a huge fan of. In order to try and crush the short seller, who posted and orchestrated numerous anonymous and misleading reports, I never sold when the stock ran during the squeeze.

The stock I am talking about was introduced to our readers at $0.34. It ran to over $3 and was one of the most heavily traded stocks on the TSX Venture. I didn’t sell at the highs because my ego didn’t want the short sellers to win.

We sent numerous complaints to the regulators about what happened. But nothing happened.

As a result, I – and many other investors – lost out on the potential to make a lot of money.

But more importantly, it eroded confidence in the stock and severely hurt the company moving forward.

I learned two important lessons…

Lesson 1: Take advantage of the short squeeze by taking profits.

Diamond hands are cool. But stupid.

Suppose retail traders actually orchestrated the Gamestop short squeeze on Reddit* as a way to attack the short-sellers. In that case, they should have done something completely different: move onto the next short squeeze.

(*I still think it was orchestrated by the hedge funds, using Redditers as a scapegoat.)

You see, most retail investors don’t understand just how easy it is to cover a short – especially if the stock is up over 2300% in a few weeks. All the short funds have to do is offer money to the company (as AMC did), and shorts are covered overnight.

Want to beat the shorts?

Squeeze them, and move on to the next one.

And never let them know you’re coming. Just be sure the short funds don’t already have a cover such as a convertible note that can be converted into shares. You can find this in Edgar and SEC filings in the U.S. and Sedar filings in Canada.

As a side note, I know marijuana is back in the limelight – so, if you’re trying to short squeeze a marijuana stock, beware that many of them have raised a ton of money using convertible notes – hence the wild swings you see within the sector. If a short fund gets caught in a squeeze and they have these notes, they can exercise to cover their shorts without ever having to buy in the open market.

Lesson 2: Short sellers always get away.

And that is the most important topic for today.

8 years…and nothing has changed

Back on May 26, 2013, I wrote the Letter, “Why the TSX Venture is Failing.” In that letter, I detailed two critical factors affecting the Canadian stock market – which also applies, to some degree, in the U.S.

- Lack of Transparency

2. Illegal/Naked Short Selling

Let’s start with the first.

Via “Why the TSX Venture is Failing:”

“The biggest and most important aspect of any stock-trading platform is transparency.

Investors should be able to see exactly how many bids and sell orders are available for a stock at any given time – especially for an exchange that has minimal liquidity and, therefore, much easier to manipulate. This is how investors calculate at what price he/she should place a buy or sell order.

The market depth can be seen using a paid service called Level II that gives you access to the order book in real-time. I have always said that anyone who trades should pay for such a service. However, even with this service, you’re far from being protected.

Especially since regulators decided to enforce what they believe to be fair competition on the TSX and TSX Venture…

Multiple Trading Platforms

Many retail investors I speak with have no clue that there are multiple parallel trading platforms for the stocks they buy in Canada.

Canadian regulators forced the TMX Group, the parent of the TSX and TSX Venture exchanges, to allow trading through alternative trading systems operated by third parties because they felt there should be fair competition in the market of buying and selling stock in Canada.

As a result, there are now many alternative market centers that process trades for stocks listed on the TSX and TSX Venture. Some of these include Alpha Trading Systems, Chi-X Canada, Pure Trading, Omega ATS, and dark pool Match Now. According to Stockwatch:

“Alternative trading systems in Canada handled 33.7 per cent of trading volume during the week ended May 3, 2013.

…The Toronto Stock Exchange and the TSX Venture Exchange handled the other 66.3 per cent.

…Looking at securities listed only on the TSX, the exchange captured 61.2 per cent of volume. Chi-X handled 18.3 per cent, Alpha had 11.7 per cent and together the other ATSs handled the rest, 8.8 per cent.”

As you can see, these alternative trading systems handle a large portion of the trading volume in Canada, yet most regular Canadian investors don’t see this because most quote systems do not include transactions from all of these different platforms.

Furthermore, while volume of trade can be seen by the select few quote platforms that incorporate the volume between these exchanges, none of them combine them in the same bid/ask level II depth because they are being traded on different platforms via parallel order books.

In other words, while you may be trading stock on one platform, that same stock is being traded on different platforms at the exact same time. This not only removes transparency – especially for the average retail investor – but it also removes visible liquidity for any particular stock.

The retail investor using his/her online trading quote system doesn’t stand a chance – especially when playing on an exchange with little volume, such as the TSX Venture.

But if parallel order books are such an issue, why is it allowed?

Fair Competition

Canadian regulators often do too much in order to solve problems where none exists.

Their job is to protect investors, but sometimes their actions have repercussions that actually end up doing the opposite.

Regulators believed they were doing the right thing in the spirit of fair competition by forcing the TMX to accept alternative trading platforms.

However, not only did this cause transparency issues for investors, but it also created a domino effect of other problems that regulators tried to combat with other regulatory amendments.

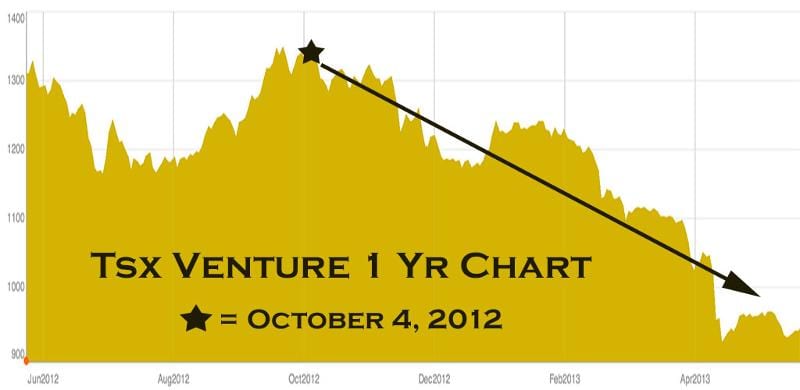

The October 4, 2012 Notice

On October 4, 2012, the TMX Group sent notice to confirm “trading enhancements,” set to begin on October 15, 2012.

The enhancements in the notice reflected recent regulatory amendments respecting short sale regulation, the introduction of a short marking exempt designation, amendments respecting dark liquidity on Canadian equity marketplaces, and functionality introduced as a result of client demand and market quality initiatives.

When you try to fight one problem with another problem, the result is never positive. I will explain what’s happened in a bit. But first, take a look at the one year chart for the TSX Venture Composite since the rules were announced:

It doesn’t take a rocket scientist to breakdown this chart:

Since the notice of the “Trading Enhancements Update” by the TMX, the TSX Venture has dropped like a rock.

Why?

The Death Spiral

When regulators forced the TMX Group to allow trading through alternative trading systems operated by third parties, it caused real-time transparency issues.

When you combine the lack of transparency in parallel trading platforms with the use of High-Frequency Trading (discussed last week), regulators had no choice but to eliminate the tick test rule, or uptick rule, for short selling.

Let me explain.

Discontinuing Price Restrictions of Short Sell Orders (Tick Test)

Historically, you could only sell a stock short if the price is higher than the last different price; simply put, you can only short a stock as it was moving up.

However, this rule only works when there is a strict sequence of orders in the order execution book; when bid/ask orders are placed in line on a first-come-first-serve basis. But with parallel trading systems, a definitive sequence of different prices can’t be established at any exact given point in time because one order book might show a down-tick, while the other an uptick.

As a result, it would be extremely difficult to enforce the uptick rule.

By allowing competing trading platforms and encouraging HFT (which was believed to create more liquidity), regulators had no choice but to remove the tick test rule. In the October 4th announcement, the rule was eliminated:

“TSX, TSX Venture Exchange (TSXV), and TMX Select will no longer constrain short sell orders to the last sale price. Short sell orders entered will be permitted to trade down to their limit price establishing a last sale price on a down tick. Short Crosses will no longer be constrained by the last sale price.”

This means we can now short a stock anytime we want. That’s great news for shorters, but for companies trying to raise money at higher prices to hire more staff or move their projects forward, this rule change can cripple them – especially under the liquidity constraints of the Canadian market.

It doesn’t take a lot of money to control a stock via short selling on the TSX Venture. As a matter of fact, institutions often hammer stocks via short selling and back up their shorts with warrants they obtained in a previous financing. They often force the price of a stock down to finance the same companies they’re shorting to get a better financing price, or to force a company into a financing arrangement.”

The removal of the uptick rule essentially caused a massive influx of illegal short selling, dubbed Naked Shorting, in Canada’s capital markets.

Via my Letter, Canada’s Stock Market Manipulation and Transparency Issues, from May 2017:

“Short selling is believed (or so “they” say) to be a necessary part of the market, providing balance and efficiency.

While this may be true in some instances, especially with the advent of high-frequency trading and ETF’s, the basic idea of short selling is completely absurd.

As I mentioned in a previous Letter:

“Short selling is simply selling stock you don’t have.

You borrow stock from someone (who likely doesn’t know you’re borrowing it), sell it, and hope that the stock goes down so you can buy it back at a lower price.”

To put that into context, it’s like saying:

You go away for vacation.

While you’re away, a stranger rents your house out on Airbnb without your knowledge.

You come home only to find your house is trashed – and now worth less than it was before.

You lose money on your house, but the stranger legally made money renting your house out.”

It’s no secret that short selling can and often does hurt companies. While short selling can provide efficiencies in the market and create more liquidity, Canada’s market doesn’t stand a chance.

This is because of yet another Canadian regulatory hurdle.

This regulatory hurdle (removal of the uptick rule) has caused short selling in Canada to run rampant – especially on Canada’s small-cap exchange, the TSX Venture.

Just how much has short-selling grown?

According to IIROC, short sales as a percentage of trades on the TSX Venture from Jan 2009-April 2010 averaged 4.39%.

But then, in the January 21, 2013 Short Sale Report, short sales as a percentage of trades on the TSX Venture averaged 6.89% for the two weeks prior.

Two years later, in the January 1, 2015 Short Sales Report, short sales as a percentage of trades on the TSX Venture averaged 7.90%.

In the most recent Short Sale Report, short sales on the TSX Venture averaged 8.57% – nearly double the average in 2009.”

Now, almost ten years later, these short sale percentages have remained and are still around the 8% mark.

But that may be just the tip of the iceberg.

SEC CHARGES TWO CANADIAN BROKER-DEALERS WITH CAUSING VIOLATIONS OF REGULATION SHO

On December 21, 2020, via the SEC’s File No. 3-20181:

“The Securities and Exchange Commission today announced settled charges against Cormark Securities Inc. and ITG Canada Corp., n/k/a Virtu ITG Canada Corp., two Canadian-based broker dealers, for providing incorrect order-marking information that caused an executing broker’s repeated violations of Regulation SHO.”

What is Regulation SHO?

Regulation SHO, or RegSho for short, is a rule that requires broker-dealers to identify a source of borrowable stock before executing a short sale in any equity security with the goal of reducing the number of situations where stock is unavailable for settlement.

For example, if I wanted to short 100 shares of ABC, my broker must have 100 shares of ABC in their system through one of their client’s margin accounts, or know where 100 shares exist for borrow somewhere else, in order for me to short it. This way, all shorted shares are accounted for in the system because any shares sold short were borrowed. The shorter has to eventually return the borrowed stock by buying it in the open market – ideally at a lower price than what he sold it for.

If a broker or myself doesn’t have access to this “borrowable stock,” and I still short it, it’s called a naked short.

The illegality of this matter is quite simple:

Company ABC has a total of 100 shares outstanding.

A shorter short sells 10 shares of ABC, without a borrow.

Does that mean there are now 110 shares of ABC? Technically, no. But on the trade books, yes. Imagine the destructive nature of this practice on a bigger scale. It’s like selling a fake Mona Lisa for the same price as the real thing.

It’s no wonder naked shorts are illegal in almost every major country, including Canada, the U.S., and many parts of the world.

However, in Canada, the rules are just “grey” enough for shorters to wreak havoc. In fact, there really isn’t a consistent rule on what naked short selling really is.

Via the OSC:

“There is no legal definition of “naked short selling” in Canada. The concept appears to have different meanings in different jurisdictions. In some jurisdictions, it refers to short selling without borrowing in time to make delivery on T+3. In others, a “naked” short sale is viewed as a sale where the seller does not own, and has not borrowed or made arrangements to borrow, securities at the time of the sale.”

T+3 essentially means a short has 3 business days to settle it, not including the transaction day. T= transaction date and +3 = plus 3 days. So if you shorted a stock on Monday, you have until Thursday to settle it.

The problem with this is that the big hedge funds have so much capital that they can afford to naked short – if the price goes up, they just buy in the open market to cover. The brokerages often look the other way because not only do they know these big accounts can afford to cover, but they give the brokerages so much business.

Just take a look.

Via the SEC’s File No. 3-20181 continued:

“According to the SEC’s order, from August 2016 through October 2017, Cormark and ITG Canada caused more than 200 sale orders from a single hedge fund, representing total sales of more than $660 million, to be mismarked as “long” in violation of Rule 200(g) of Regulation SHO.

The SEC’s order finds that Cormark and ITG Canada provided incorrect order-marking information to the hedge fund’s executing broker, causing that broker to mismark the hedge fund’s sales as “long.” The order further finds that it was not reasonable for Cormark or ITG Canada to rely on its customer’s assurances that the orders were properly marked “long” because both brokers were on notice of the customer’s repeated failures to deliver the securities by the settlement date.

According to the order, as the hedge fund’s sale orders were, in fact, short sales, Cormark’s and ITG Canada’s incorrect order-marking information also caused the executing broker to violate Rule 203(b)(1) of Regulation SHO by failing to borrow or locate the shares prior to effecting those short sales.

The SEC’s order finds that Cormark and ITG Canada caused the executing broker’s violations of Rules 200(g) and 203(b)(1) of Regulation SHO of the Securities Exchange Act of 1934. Without admitting or denying the findings, Cormark and ITG Canada each agreed to cease and desist from committing or causing any violations and any future violations of Rules 200(g) and 203(b)(1) of Regulation SHO. In addition, Cormark agreed to pay a penalty of $800,000, and ITG Canada agreed to pay a penalty of $200,000.”

$660 million worth of fraudulent trades, and it only cost the brokerage houses $1 million.

And the penalty for the hedge fund that orchestrated those illegal sales? Zero.

So while other outlets claim that the delay in short reporting caused Gamestop stock to reach over 100% short interest, the real culprit could simply be that many institutions are lying.

Perhaps they are simply marking a short position as a “long” – as per the SEC charge above.

If you think that’s bad, it gets even worse for Canadians.

Scare Tactic Engaged

Via Canada’s Stock Market Manipulation and Transparency Issues continued:

“…The removal of the uptick rule has created a breeding ground for short funds to make a lot of money betting against companies – especially companies that trade on the TSX Venture.

When you consider that companies that trade on the TSX Venture are likely companies that are speculative and often negative cash-flow businesses, short selling can immediately hurt a company’s ability to finance.

Furthermore, short funds can use computer trading to add additional pressure on stocks to the downside by making it look like there is a lot of stock for sale. In other words, stock manipulation.

And yes, stock manipulation is illegal.

So how do they do this?

How to Manipulate Stock Through Short Selling

When the removal of the uptick rule was implemented on October 4, 2012, a short marking exempt designation (SME) was also introduced.

Via IIROC:

“The “short-marking exempt” designation is required to be applied to orders for qualifying accounts of arbitrageurs, market makers and “high-frequency traders” that typically generate a high volume and speed of orders on a fully automated basis, may have orders on both sides of the market on various marketplaces at the same time, and that adopt a “directionally neutral” strategy such that generally, the position in each security in the account is flat at the end of the trading day.”

In other words, as long as a firm adopts a “directionally neutral” strategy, such that generally, the position in each security in the account is flat at the end of the trading day, it doesn’t have to declare the short sale.

This was done because IIROC believes that the use of the SME order designation allows them to separately monitor the trading activities of those accounts which are actively buying and selling the same security without taking a directional position and that of actual short sale activity on accounts that may have adopted a “directional” position.

While this may have good intentions, it actually makes it easier for firms selling short to manipulate the price of stocks.

Spoof Trading

Here is Bloomberg’s take on Spoof Trading:

“Spoofing is when a trader enters deceptive orders tricking the rest of the market into thinking there’s more demand to buy or sell than there actually is.”

In the case of short selling, a trader would show pressure on the sell-side through stacked sell orders but remove them if the market begins to move higher.

These stacked sell orders are often viewed – especially by retail investors with a lack of market data – as weakness in a stock.

You may be wondering: What happens if buyers come into the market? Wouldn’t the sell orders be on the hook to buy the stock?

You see, these sell orders are often in small board lots (usually 100 shares) so that anytime the lead sell order is hit, the firm only has to sell a few shares short.

When this happens, the computers automatically adjust their sell orders higher while still maintaining pressure on the stock by maintaining the multiple stacked sell orders – oftentimes behind a real sell order.

This allows the short sellers to put downward pressure on a stock without having to declare a short because they remain “neutral” by buying just enough shares to end up with a flat position in the account at the end of the trading day.

And because the uptick rule was removed, short funds can now downtick a stock and still short the next day.

What is Downticking?

Downticking is when a trader sells stock so that the most recent change in the share price is negative. This is usually done right before the market closes using very small amounts of stock.

And since stock charts only follow the closing price of a stock, you can see how easy it is for a short seller to create a nasty-looking downward chart by spoofing and down-ticking.

These practices are illegal but happen to many Canadian stocks.

Just ask the Ontario Securities Commission.

Most retail investors don’t see this type of activity because most trade without the use of Level II data. They only see the last bid/ask price, which may not even be correct as I already mentioned earlier.

The next time you see a stock in the green for the whole day, only to end up in the red with less than a minute to go, you now know what could have happened.

The problem for Canadian regulators is that they can’t keep an eye on the thousands of stocks that trade every day.

Even when they do catch it, it’s extremely difficult to find the culprit behind the trades since the short-sellers have multiple accounts at different financial brokerages and often work with other short-sellers.

Furthermore, regulators often rely on complaints.

But how can a retail investor make a complaint if they don’t even see this “spoofing” or the down-ticking because of the lack of mandate for consolidated market data?

Retail investors don’t get to see the Level 2 data because it’s expensive. How can an investor react to this type of predatory short selling?

How can an investor report manipulative trading to IIROC or the Canadian Securities Administrators (CSA) if they don’t have access to the data?

If there was a regulatory mandate to provide consolidated market data in Canada, we could make much more informed investment decisions.

If Regulators could mandate market data transparency with new short sale regulations such as the re-implementation of the uptick rule and more frequently updated short reports (currently only reported semi-monthly), then maybe we could prevent the Canadian market from failing.

… Combine the lack of required consolidated market data, the removal of the uptick rule, the introduction of the SME designation, with the illegal practice known as “short and distort,” and many Canadian companies and Canadian-born innovations listed on Canada’s stock market could be doomed to failure.

And it makes it even harder for retail investors to succeed.

In the U.S., they have already reintroduced an alternative uptick rule…”

It really isn’t that hard to offer transparency to retail traders. However, the stock exchanges make a lot of money selling this transparency to institutions. If they offered this for free, they would lose out on billions of dollars.

But times are changing, and hopefully for the better.

We are now seeing discount brokerages offer bigger trading discounts. We are now seeing commission-free trades. We are now seeing a massive influx of spending by financial institutions geared towards the retail trader.

Could we see the first retail trading platform to offer free level 2 data?

I bet the first to offer this will become the biggest retail trading platform. Whose in?

Conclusion

The dark side of Gamestop is that many retail traders have lost their shirts.

The bright side is that it has brought serious attention to not just the entire stock market in the form of retail participation, but it also exposed just how evil short-sellers are.

As I said in October 2020, and before Gamestop happened, retail investors are just beginning to participate. Heck, I was at the dentist last week only to overhear an ex-banker quit his job to daytrade. One look at the small-cap index, famed for its massive potential for gains, and anyone can see just how much risk money is pouring in.

Let’s not let a few short sellers destroy the potential of what retail investors can bring to the table.

Is it really that hard to implement stricter rules?

If you steal a car, you go to jail. If you steal from a bank, you go to jail. So if you steal someone’s else stock, shouldn’t you go to jail?

Well, if you’re in Korea…

Via BNN Bloomberg:

“Naked short-sellers, or investors who sell stocks they haven’t even borrowed, will be punished by at least a year’s jail term or fined up to five times their profit from the trade, according to a statement from the Financial Services Commission. Currently, naked short selling, which has always been illegal in Korea, is punished by lower fines.

Fearing volatile markets, Korea imposed a broad short-selling ban in March as the coronavirus outbreak worsened, then extended it in August for another six months. Korea remains one of the few countries globally that continues to bar such a practice.

“Regulators seem to be trying to improve Korea’s current short-selling system before the ban on it is lifted next year,” said Han Byung-hwa, analyst at Seoul-based Eugene Investment & Securities.

Seoul is now considering a partial lift of the ban in March and even plans on giving retail investors the privilege of trading borrowed stocks to put them on a level playing field with institutional investors, according to Financial Supervisory Service, the top watchdog, two months ago.

The FSC said in its Wednesday statement that it is becoming stricter about naked short-selling to “boost trust” in the country’s stock market, adding, however, that legal short-selling remains a positive tool in making markets more efficient.”

So how did Seoul’s stock market perform without short selling?

Via CNBC:

“The Kospi index, South Korea’s stock-market benchmark, rallied 30.8% for the year, its biggest annual jump in more than a decade.

The iShares MSCI South Korea ETF (EWY) rose 38.4% in 2020, outperforming most developed and emerging markets. The ETF’s year-to-date gains top those of other widely followed emerging markets as well as the S&P 500 in the U.S.”

Wow, it really is that simple: ban short selling and the market outperforms. Go figure.

Seek the truth,

Ivan Lo

The Equedia Letter

www.equedia.com

Equedia.com and Equedia Network Corporation are not registered as investment advisers, broker-dealers or other securities professionals with any financial or securities regulatory authority. We are also not doctors or experts on viruses. Remember, past performance is not indicative of future performance. This article also contains forward-looking statements that are subject to risks and uncertainties that could cause actual results to differ materially from the forward-looking statements made in this article. It’s your money to invest and we don’t share in your profits or your losses, so please take responsibility for doing your own due diligence and consult your own professional advisers before investing in base metals or trading in base metal securities.

If there is a way for retail investors to pressure the Canadian regulators to impose Korea style controls, how about sharing that information with us?

You can try but contacting https://www.iiroc.ca/Pages/Contact-Us.aspx but good luck with that. Industry professionals have been trying for years!

I only have level 11 on the non TSX-V exchanges. We used to have it, but TD charges us $20 a month and we didn’t think it was worth it. Maybe we were wrong in our assessment. I really do not know just what happened regarding GME, despite the hundreds of pages of information I have read about it. Much of the information is wildly opposing, so it is hard to tell what the truth is. As for short selling, I have NEVER agreed with it, and never will.

I do not short. I assume that is what happened to NXO not long ago.

I love what Korea did. I’m curious how their ban on shorts affected liquidity? I’m guessing its as strong as ever as sideline investors are more inclined to become active.

Great question on liquidity. Every institution will say short sales contribute to liquidity. Try telling that to South Korea’s stock market, where trading volume has now doubled since 2019, and is at the highest it has ever been.

YOU BET I’M WITH YOUR TRAIN OF THOUGHT

Ivan, Thank you, that was very informative and thought-provoking. I had never thought about what short-selling really means before. I essence, somebody borrows someone else’s property, without their permission, in order to destroy the value of that property for profit. Of course this practice should be banned!

The problem is, even if a short sale was executed properly, many times, retail traders have no clue that their shares are being lent out if it sits in a margin account. And very rarely are they paid interest on these shares.

Mr. Lo,

You asked for opinion on short selling:

1.It is an incentive for those who uncover fraud/shenanigans/or just corporate dissembling and misleading hype to legitimately profit from their research. Examples WKHS, NKLA, Luckin Coffee etc, etc. Yu do not mention those benefits to keeping the market honest. Many US investors refuse to buy Canadian stocks because of the atrocious hype in promoting many companies — particularly in the mining areas that are your expertise. It would be good for you to at least address this issue.

2. You equate short selling with “stealing” the borrowed shares. What an exaggeration. Borrowing is not stealing. If you have a margin account you agree to let your shares be borrowed. If a cash account your shares cannot be borrowed without your permission. A few US brokerage companies will pay individual investors a fee to lend your shares. Major institutional investors including mutual funds and ETFs make a lot of money lending shares. It helps reduce expenses for the fund owners.

3. The idea that Koreas 2020 performance in the stock market was due to the ban on short selling is close to being a howler. You pick one market factor short selling ban and attribute the performance to that. Well, the NASDAQ 100 was up 48% in US in 2020 and other indexes also beat Korea, all of which allowed short selling. You conveniently ignore that maybe squeeze of the shorts contributed to that.

4. I will agree that big money on both sides was more responsible for GME volatility than individual traders alone. Big funds and institutions made millions on both sides.

All in all I would have to say this was one of your more ax grinding one sided reports.

Hey Chip, thanks for your points. Surely, there are arguments to every side. So will do my best to be fair here. And clearly, it would appear you are a much more experienced investor than most, based on your comments.

1. Overvaluation is one thing, fraud is another. How many “frauds” have short seller reports actually uncovered relative to the amount of shorts out there? Maybe 1%, if that? How many short and distort reports have destroyed companies that weren’t fraudulent? Please send me just one short company that bats 100% on uncovering fraud. Mining is a very different beast – it’s often hit or miss. While I have seen overly promoted companies that ended up missing drill results, to call them fraudulent maybe too far? Guess this depends on who is behind the deal and what their intentions are.

2. No, I didn’t say short selling is stealing – I said naked shorting is. If a short is borrowed legitimately, that’s much better than naked. But as I mentioned in this article, shorts can easily be marked “long,” even if they’re a true short. So yes, I’d say that is wrong and illegal, no? And still, no one should be able to short a stock without the uptick rule in place, especially for lower market cap companies. Now, let me ask you this: how many retail traders actually short stocks? 0.13% of all trading volume is from retail investor short sales. When you consider that on average, short sales make up a min. of 5.5% of trades, you see just how much short sales favour only the big funds. Feel free to do the math here on what percentage of short sales is from retail traders – its tiny, very tiny. This is a game primarily played by much bigger funds to take advantage of retail markets. Here’s a research report that shows these stats: https://www0.gsb.columbia.edu/faculty/ptetlock/papers/Kelley_Tetlock_May16_Retail_Short_Selling_and_Stock_Prices.pdf

3. “You conveniently ignore that maybe squeeze of the shorts contributed to that.” Not at all. Shorts didn’t squeeze over an entire year – every stock market rebounded also. Comparing the Korea stock exchange to the NASDAQ 100 is silly – you’re talking about the biggest tech companies in the world that benefitted from the pandemic. You’re also talking about stocks with significantly more volume than any other exchange in the entire world. It really is simple: the removal of short selling helps stocks go up and not down. Why do you think they banned short selling on financials back in 2008? In EVERY case where short selling was banned by a regulator, it was to prevent stocks from going down.

4. And they still do to this day 🙂

Thank you Equedia,(Ivan) for a well written article dealing with a such complicated issued that is human behaviour(physcology)!

When you let an entities or someone take advantage of the financial market using different scheme, questionably legal as mentioned in your article. Unless you stop them from doing so , it will continue until a catastrophe happen because as human we seek our best interest first in short term view whereas our collective interest in the long run are somebody else problem.

More regulation will just make the professional (finance) find other tricky way to take advantage of the system and us. Until the inevitable happen then the government will borrowed money under our name to save the ones who created the problem first!!

Wide Open market information available on real time to all would be ultimately the financial market democratisation which unfortunately is for now an utopia. Technologically it is probably feasible (we’re about to send people on Mars) but we won’t because to many hands takes their taken.

Personally for the time being i diversify my portfolio with 3 sectors; personal ownership of Real estates, Retirement funds managed by professionals firms (LOL) and finally secured term deposit.

In the future, I way decide to re-invest directly in the market but the more i read about it the more i get speticcal.

Good luck all!