This massive bull market has nothing to do with the S&P 500, the NASDAQ, or the Dow.

Yet, it is outright crushing its competition.

In fact, it’s the best-performing stock exchange in the world right now.

While everyone is focused on Brexit, the Fed, and Hilary vs. Trump, this one stock exchange has quietly edged up an astonishing 36% this year.

And it’s all happening right here at home.

The TSX Venture is back.

Welcome Back Canada

Last year, I wrote:

“While 2016 won’t be an easy year for investors, I do believe that positive change is coming – at least in the Canadian capital market space.”

While the US market is now flirting with fears of uncertainty and capital outflows, Canada’s TSX Venture is in a full-fledged bull market with growing capital inflows, supported by the recent rebound in commodity prices.

Via Bloomberg:

“The Bloomberg Commodity Index, which tracks a basket of 22 resources from crude to soybeans, closed 21 percent above its low on Jan. 20 to meet the common definition of a bull market.”

This doesn’t mean the TSX Venture – or commodities – is completely back. The exchange did just reach an all-time low in December 2015, with its index composite closing the year at 525.66, down by about 24% from the end of 2014.

But volume has been strong, despite the “Sell in May” and summer sentiment we’re accustomed to.

More importantly, there is real money flowing back into the sector.

In fact, the total number of financings on the TSX Venture in 2016 has already surpassed that of 2015.

In 2015, the total number of financings on the TSX Venture was 551 with a total value of:

$1,274,935,381.

In just five months, between January to May 2016, there have already been 591 financings with a total value of $1,400,196,478.

The desperate tone is gone and it’s been replaced by excitement.

This is a drastic change in sentiment from the previous years.

But while this is great news, it’s not all sunshine and lollipops.

When Will We Learn?

Just a couple of years ago, many Canadian investors left the market and said they were never coming back.

They were tired of the same moose pastures being flipped from one public vehicle to the next, being touted every time as the next new big discovery – even though they weren’t.

Many of the deals that were promoted a few years ago no longer exist today; they simply weren’t good enough to survive the downturn.

While I believe this current sector turnaround is real and should continue, I am quite worried that many investors are being duped once again.

I am seeing a lot of deals trade heavy retail volumes, which is great, but some are being promoted with nothing more than a Letter of Intent (LOI). That means investors are literally buying into a story that hasn’t even come to fruition yet.

So before you go investing in a new mining deal, do your homework. Make sure the people are good, the project is good, and there is money in place to advance the asset.

If you’re being promoted a Company that tells you they’re onto the next great gold discovery, yet all they are doing this year is collecting some grab samples, that’s a red flag.

The great thing about the recent downturn is that there are many great companies that are extremely undervalued with the potential to give us great returns if this market boom keeps up.

There’s no need to gamble on grassroots exploration plays, where only 1 in 5,000 to 1 in 10,000 of them ever reach the production stage.

I believe that the market will be strong for mining stocks – especially gold and silver – in the coming years and lots of money will be made.

Don’t let the poor deals take you out of the market early.

The Gold Run

You may recall back in July 2015 when I said it was time to get back into the gold sector.

“…Gold stocks are now trading at fundamentally ridiculous price levels today and have never been cheaper relative to the gold price itself. This is an anomaly that simply isn’t sustainable.

Which is why I believe that gold’s actions this week may have just set us up for an incredible opportunity.”

Then, in May 2016, I showed you just how well the sector has performed since then, and why I expected it to climb higher:

“…Aside from blatant manipulation (and that’s a possibility), there just isn’t a scenario where I can see gold falling much further, but many scenarios that suggest it will climb higher.

Even if gold maintains its current price, there will be many gold stocks that will do very well – especially the producers with low all-in sustaining costs.

But if gold moves higher – which I believe it will – a lot of money will be made in gold stocks.

And that’s why I am looking to add more.”

Just after writing that Letter, gold fell sharply lower.

I addressed this in a follow-up Letter:

“…A couple of weeks ago, I explained why I believed the stock market rally could end this year and why I believed gold could climb higher.

But last week, the rally didn’t end and gold didn’t climb.

Instead, the stock market moved higher, while gold was smashed back down to the low $1200’s.

So was I wrong?

I don’t think so. In fact, I believe we’re being set up.”

Turns out, we were set up.

Over the next two weeks after that Letter, gold rebounded and spiked passed US$1300 for the first time in two years.

Meanwhile, the S&P 500 posted its worst week since April.

The rise in gold and the poor performance of the US market over the last two weeks was the direct result of two things:

- Fed not raising rates

- Brexit Fears

Of course, there was no way to know for sure that the Fed wasn’t going to raise rates, and we still don’t know what the Brexit outcome will be.

So why did I believe so strongly that gold was going to climb higher?

One of the most important things I urge investors to do is to focus on what we know rather than what we don’t.

There was no way of knowing that the Fed wouldn’t raise rates, and there was no way of knowing that the Brexit vote would be postponed following Thursday’s slaying of politician Jo Cox.

So what do we know?

The Primary Theme

Everything from Brexit to China’s economic and financial bubble, to the thought of the Fed raising rates, all of these near-term nuisances of politics and financial maneuvering converge into one overall theme: debt.

More importantly, how debt is managed.

Over the past years, I have talked about how the debt bubble – short of a global financial reset – has no choice but to get bigger.

And that’s precisely what’s happening.

Global debt continues to climb to record new highs.

We’re not talking a small amount either; the world is now issuing trillions upon trillions of new debt every year.

In China, total debt (China’s total corporate, household and government debt) grew to a ratio of over 280% last year.

In the US, it grew to a staggering 331%.

In Japan, over 400%.

Many countries in Europe such as Ireland, Portugal, Belgium, Netherlands, Greece, Spain, and Denmark are all over 300%.

In other words, the total-debt-to-GDP ratio in the nations that contribute to the four main world currencies – the Dollar, Yen, Euro, and Yuan – all have exploding debts that are continuing to, well, explode.

Which is precisely why central banks around the world are not only NOT raising rates, but some have already deployed negative rates, including Japan and the EU – home to two of the five world reserve currencies.

So while most central banks are talking about negative rates, the Fed is the only one talking about raising them.

But if the Fed raises rates too soon, the US will certainly see a decline in exports, which then makes it harder to collect the necessary taxes to pay for its growing debt.

Negative Interest Rates

So it was no surprise that the Fed announced that it would keep interest rates at 0.25% this week.

The Fed and other central banks believe that if they lower rates, people will spend more, or invest in riskier assets because the cost of storing cash becomes too high.

And since governments around the world (including the US) are the biggest borrowers of money, low interest rates are great.

It means these governments can continue to borrow money and go deeper into debt. The government’s idea is that by spending cheaply borrowed money, they can pull themselves out of debt through economic growth and tax collections.

It also means that banks can borrow money for next to nothing – literally free cash – and then earn profits from that money by lending or other activities such as investing.

On the flip side, if you’re responsible with your money and save – say for your kid’s college tuition or your retirement – low interest rates aren’t so good.

That’s because when you leave your money in the bank, you might earn a small interest rate. Given how low rates are today, that’s likely 0.1% interest.

In the US, inflation has averaged over 2% since 2000. That means that when you adjust for inflation, people who keep their money in the bank are actually losing money every year.

The problem is that no matter how much our governments spend, they simply can’t fix the growing debt problem because of the amount of money required just to service that debt.

The Double-Edge Sword

The lower the interest rates, the more we go into debt.

The more we go into the debt, the more the central banks – the primary holders of this debt – maintain control.

So we’re really in a lose-lose situation.

If we raise interest rates, nations around the world are crippled because their ability to pay off this debt is diminished as a result of the mass amount of debt they accumulated at a low interest rate.

Global debt has grown by at least $57 trillion (2014*) to $199 trillion and no major economy has decreased its debt-to-GDP ratio since 2007.

*We’re well beyond that number today.

But at the same time, leaving interest rates low just leads to more borrowing, and the only way to service that debt is by more borrowing.

In the end, the central banks win by maintaining direct control of the world’s governments through monetary policies. If a central bank says jump, a country has to ask, “how high?”

If our governments don’t do as ordered, the central bank simply raises rates and the country falls into money trouble.

And Canada is no exception, especially since Trudeau is now leading us on the same path.

Canada and Trudeau

Last week, I talked to a mortgage broker about interest rates.

He said that it’s probably best to lock something in because Canada is likely raising rates since we often follow in the footsteps of the US, whose central bank has suggested that rates will be raised.

But then I asked him about the housing bubble we currently face.

I asked, “If rates are raised, wouldn’t our housing market be crushed because so many new homebuyers have taken out massive mortgages based on low rates?”

He said that could happen, but banks are very strict with their lending practices in Canada.

Then I asked, “What about Trudeau’s plan of spending billions upon billions of borrowed dollars, based on the assumption that interest rates will remain low?”

He started to scratch his head.

My point is this:

With Trudeau’s budget and our current housing situation, the likelihood of Canada raising rates anytime soon is highly unlikely.

Especially when Trudeau tells us that this year’s $30 billion deficit is not a hard limit.

Via Toronto Sun:

“Prime Minister Justin Trudeau suggested on Thursday that a $30 billion budget deficit was not a hard limit as the government’s focus should be on spurring economic growth.

In a wide-ranging interview, Trudeau, 44, said he was not obsessed with a “perfect number” for the budget deficit and instead vowed to find the right path to economic growth, saying that was more important than a specific deficit target.”

Perhaps this is yet another reason why Canadian investors, including institutions, are becoming more speculative. Money is cheap and will likely remain cheap, and the cost of holding money is more than it would be to deploy it in riskier assets.

So what’s the solution?

CONTENT LOCKED

Enter your email to get instant access (it's free!)

to this special content post:

*By entering your email, you are agreeing to our privacy policy and terms of use. You will also receive a free weekly subscription to the Equedia Letter, one of Canada's largest private investment newsletters. Don't worry, it's free and you can cancel at anytime.

Government Experiments on Free Money

The only way out is to either raise taxes exponentially, which hurts the economy, or the last and final resort: helicopter money.

What is helicopter money?

Helicopter money is exactly what it sounds like: free money from the skies.

To make things simpler, imagine a tax break, or a tax refund given directly to you by the government, who borrowed it from the central bank.

Of course, it’s only temporarily free. The money is still owed by the government to the central bank.

And government debt equals taxpayer debt.

It’s essentially forcing you to borrow money from the central bank.

Don’t think for one second that this is a far-fetched idea.

In fact, not only did Janet Yellen not raise rates this week, she actually alluded to the fact we could see helicopter money coming:

“It is something that one might legitimately consider.”

In Europe, lawmakers are already urging the central bank to deploy free money to citizens.

“In an open letter to ECB president Mario Draghi, 18 members of the European Parliament’s social democrat, leftwing and green groups, say that the ECB should look at helicopter money as well as buying bonds from the European Investment Bank “as possible solutions to enhance economic development through direct spending into the real economy.”

Don’t think Canada is out of the question. In fact, basic income experiments are underway – an experiment whereby the government gives people money for free, for nothing.

Don’t believe me? Check Trudeau’s pre-budget report, it’s in there.

In Japan, this is already happening through government asset purchases of stocks.

So what’s wrong with free money (aside from the fact it’s not really “free”)?

The more there is of something, the less it’s worth…

Protection from Currency

While I can’t say for sure what the Fed or government will do, or what monetary and fiscal policies they unleash, there is one thing I can say with the utmost certainty won’t happen:

No central bank or government will give you gold.

In fact, they’re doing the complete opposite: they’re hoarding it.

We already know central banks have been, and continue to be, net buyers of gold since 2010*.

(*With the exception of Canada, which just sold our last bit of gold this year to fund Trudeau’s budget. But here’s a thought: Canada has a lot of gold in the ground. If gold were to climb, or play an even bigger role in world currency, I would bet that a hefty tax would be placed on gold miners in Canada.)

India has even created gold bonds to not only prevent gold from leaving the country but to take gold directly from the private hands of citizens and into the public ledger.

And now, multi-billionaire moguls are doing the same thing.

George Soros, the multi-billionaire hedge fund manager, and one of the richest and most powerful men in the world has already been selling and going short stocks, while diversifying into gold and shares in gold mining companies.

BlackRock, the world’s largest asset manager, told the world last month that:

“…Although central banks have been the primary architect of this surreal state of affairs, even if they decide to reverse course, real borrowing costs are likely to remain low relative to the historic norm.

Factors such as demographics and tepid economic growth are contributing to the unusually low level of real interest rates (i.e. after inflation).

All told, this is a serious problem for yield-starved investors. Ironically, one potential remedy is to take a second look at an asset class that provides no income: gold.

…This is exactly the type of environment that has historically been most favorable to gold.”

Smart money investors – or rather BIG money investors – have been diversifying into gold at an astonishing rate.

And while they continue to soak up gold at depressed prices, the majority of the world continues to fall into the illusion that there isn’t a global financial and economic crisis brewing.

Which, in the end, means many investors will suffer losses once again.

This is precisely why my tone has changed over the last year. Stocks are exhausting and gold is just revving up.

When we first talked of Negative Interest Rates or NIRP a few years ago, many thought it wasn’t real. Since then, six central banks have deployed it, only to realize that it may or may not be effective.

Just over two years ago, there wasn’t a single government bond with a yield below zero.

Today, more than $10 trillion of government debt worldwide is now trading below zero yield.

But the problem is even bigger than that.

“Lurking in the bond market is a $1 trillion reason for the Federal Reserve to go slow on interest-rate increases.

That’s how much bondholders stand to lose if Treasury yields rise unexpectedly by 1 percentage point, according to a Goldman Sachs Group Inc. estimate.

A hit of that magnitude would exceed the realized losses since the financial crisis on mortgage bonds without government backing, Goldman Sachs analysts Marty Young and Charles Himmelberg wrote in a note published today.”

Simply put, a small rise in rates could cause a financial crisis far beyond that of the one that triggered the 2008 crisis.

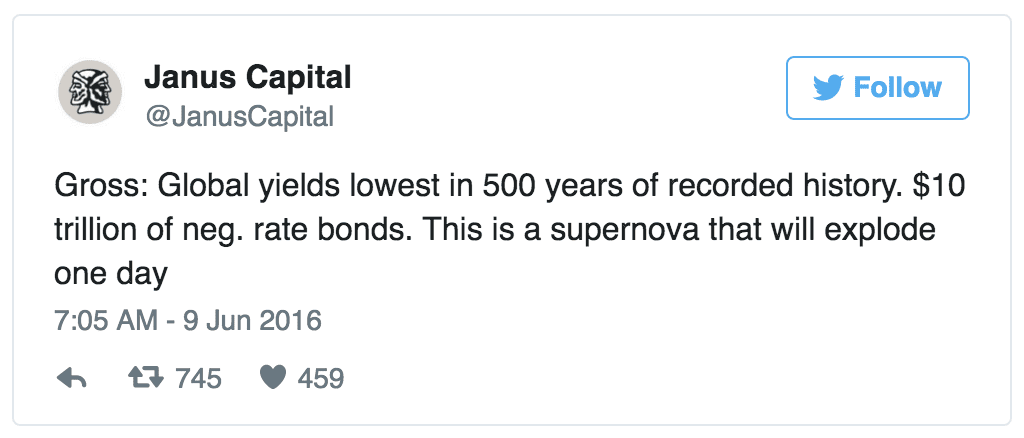

It’s no wonder why Bill Gross, the man who managed and co-founded the world’s largest bond fund, PIMCO, tweeted earlier this month:

I don’t think he’s bluffing.

I don’t think he’s bluffing.

Perhaps that’s why foreign investors continue to dump US Treasuries at the fastest rate since 1978.

Via Reuters:

“Foreign investors sold a record amount of U.S. Treasury bonds and notes for the month of April, according to U.S. Treasury Department data on Wednesday, as investors priced in a few more rate increases by the Federal Reserve this year.

Foreigners sold $74.6 billion in U.S. Treasury debt in the month, after purchases of $23.6 billion in March.

April’s outflow was the largest since the U.S. Treasury Department started recording Treasury debt transactions in January 1978.

Private offshore investors sold $59.1 billion in U.S. government bonds, while foreign official institutions, which include central banks, sold $12.3 billion.”

Could the private offshore investors who just sold a whack load of US bonds know something we don’t?

Based on what we know for sure, I believe gold’s run will continue throughout the coming years. Real diversification and an allocation to gold bullion coins and bars remain the key to weathering the second global financial crisis.

The BIG money is quietly positioning themselves by investing in gold and silver bullion and coins, ETF’s, and miners.

I am too.

I’m sure you’ve looked at Pretium Resources and I expect it will do extremely well in the future, especially once it goes into production. I have analyed this prospect for several clients during the last 5 years.

Since Canada divested itself of gold, I would expect taxation of miners. I wonder if the Canadian government would ever consider nationalizing miners.

Jim

I want to compliment you on you inciteful messages. I look forward to them.

Thanks