Dear Readers,

Dear Readers,

Surprise. The Fed didn’t taper.

Of course, those of you who have been reading this letter already knew that tapering was unlikely to happen.

The mainstream media has a very short-term memory. Instead of talking about the details of Quantitative Easing (QE) and the Fed’s goals, they only focus on the new term of the day: Tapering.

So let’s refresh their memories.

From my letter in December 2012:

Quantitative Easing 4: $2 Trillion

The Fed will now “print” $85 billion a month until the unemployment rate falls below 6.5% and inflation projections remain no more than half a percentage point above 2% for two years out. In addition to buying Both Treasuries and Mortgage Backed Securities with the $85 billion, the Fed will also begin rolling over its maturing Treasuries as of January.

But here’s the big kicker: For the first time, the Fed is now pegging QE directly to quantitative thresholds – namely, inflation and unemployment data, as opposed to its normal calendar-based guidance. That means it will print until the problem is solved. Furthermore, now that the inflation neutral operation twist is out of the picture, the additional $45 billion per month is coming directly from the printing press. How can you not call that Quantitative Easing 4?

As I mentioned last week, QE3 would cost over $1 trillion if calculated over a one-year span. With QE4 now in place, we’re going to see an $85 billion stimulus per month for at least 2 more years. That’s a total of more than $2 trillion in additional stimulus.

To get a better sense of the Fed’s direction and quantitative thresholds, let’s take a look at where the economy stands, or rather where the government wants you to think we are.

Let’s start with the inflation rate.

Inflation Rate

The Fed uses the personal consumption expenditure price index (PCEPI) to come up with its inflation numbers, and not the Consumer Price Index (CPI) as most journalists often quote against Fed statements.

The Fed bases its calculations on core PCEPI, which excludes energy and food prices (but now includes restaurant meals under food services, and pet food under pets), because the Fed thinks that food and energy prices are too volatile when making their long-term calculations – even if food and energy are the two most important aspects of human life.

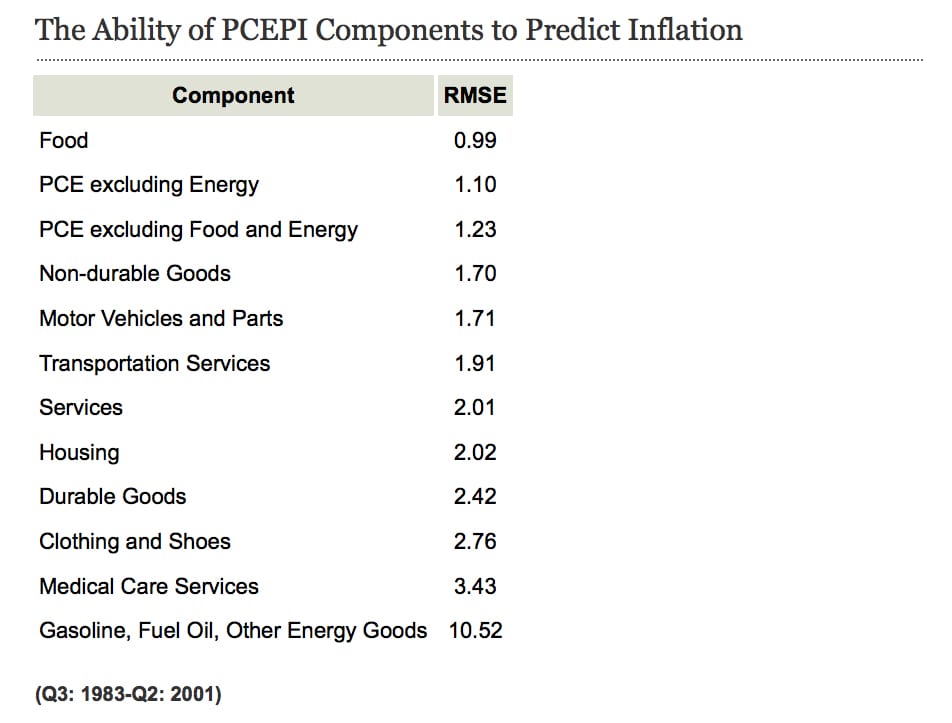

And while energy prices can be volatile, food has actually been one of the best indicators for future inflation.

Take a look:

(*The better that past inflation in a component of the PCEPI is able to forecast overall inflation, the better an indicator it is of the true inflation trend. The root-mean-square-error (RMSE) measures how far away a forecast is from the actual measured value and is, therefore, a measure of how good a forecast is. Components with a smaller RMSE are better at forecasting future overall inflation. Here, we see that food has the lowest RMSE, indicating that we might be losing valuable information about trend inflation by removing it from our measure of core inflation.)

But the Fed loves to print because the more it prints, the more money banks make via lending, which leads to more borrowing, which is supposed to lead to more spending. So the Fed continues to base its stimulus calculations on core PCEPI.

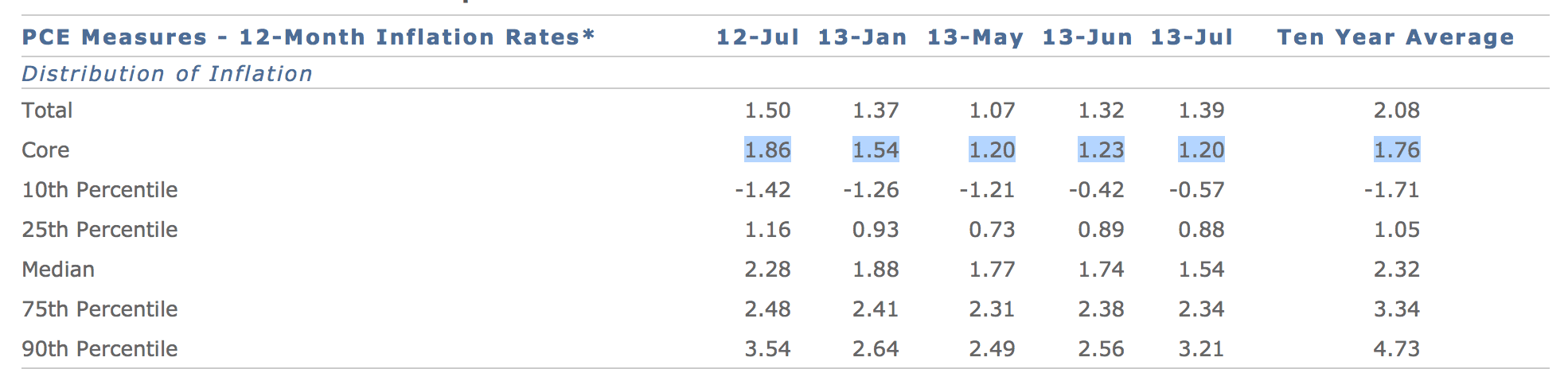

And the inflation rate based on core PCEPI, as of July 2013, was a dismal 1.2%:

As a matter of fact, over the last 10 years, core PCEPI averaged only 1.76%:

The Fed is looking to print until the core PCEPI-based inflation rate reaches between 2% and up to 2.5% for two years out. Considering that the 10-year average is 1.76%, reaching 2% anytime soon seems like more hope than reality.

This gives significant ammunition for the Fed not to taper.

Now let’s look at unemployment.

Unemployment Data

The Fed wants to see unemployment below 6.5%.

As of August 2013, unemployment is 7.3%.

The last time unemployment fell below 6.5% was in 2008, just before the market crashed:

While the above chart shows that the unemployment rate has been falling over the past year, don’t be fooled; it was more the result of people leaving the workforce than actual jobs being created.

Earlier this month, the Bureau of Labor Statistics (BLS) said the economy added just 169,000 jobs in August, while the Labor Department said 312,000 people dropped out of the workforce.

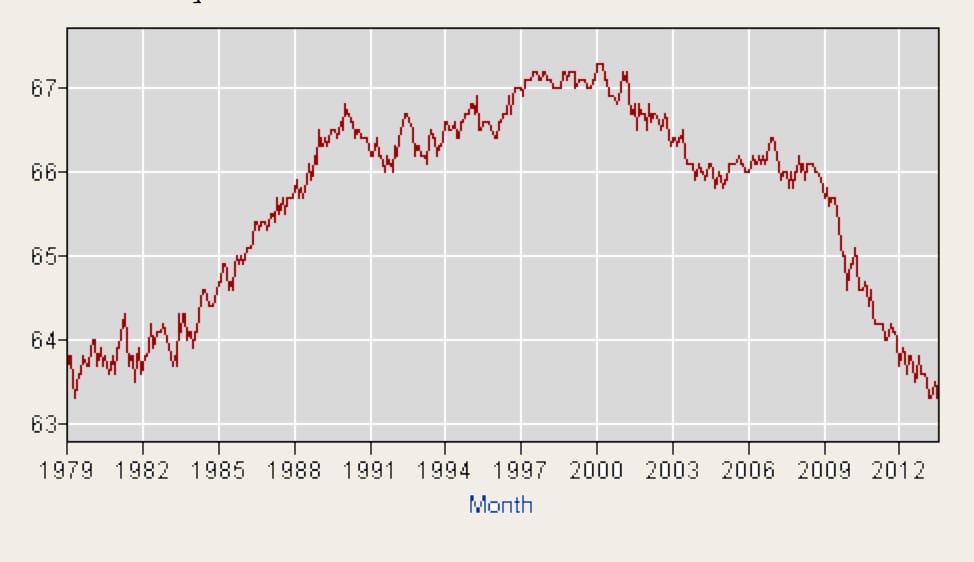

In fact, the labor-force participation rate, which tracks the percentage of working-age Americans who are actually employed or looking, fell to 63.2 percent in August.

Take a look at how the labour participation rate has dropped since 2008:

The country hasn’t seen that few eligible people actually working since August 1978:

That means more people are leaving the workforce, likely giving up on looking for work and relying on government support their survival.

And let’s not forget the quality of jobs being created. As I wrote in a past letter:

According to the Bureau of Labour and Statistics’ (BLS) household survey, part-time jobs in June soared by 360,000 to 28,059,000 (seasonally adjusted) from 27,699,000 – an all time record high. Full time jobs? Down 240,000, from 116,238,000 to 115,998,000.

Since the beginning of the year, the U.S. has added 557k part-time jobs, but only 130,000 full-time jobs. Perhaps that’s because of the jobs created, 239,000 went to minimum wage restaurant and bar jobs. As for manufacturing jobs: 13,000.

The Fed’s Magic Number

The Fed said it will begin to entertain the removal of stimulus measures (low rates and QE) once unemployment reaches 6.5% or less.

So how many jobs need to be created for the Fed to reach its 6.5% unemployment target rate?

In order to calculate this, let’s assume the following:

| Labor Market Statistics | Current Statistics* | ||

| Civilian non-institutional population, 16yr+, (CPS, Household Survey) | 245,959,000 | ||

| Employment (CPS) | 144,170,000 | ||

| Employment (CES, Establishment Survey) | 136,133,000 | ||

| Average monthly CES/CPS employment ratio (previous 12-month avg.) | 0.941 | ||

| Number of unemployed (CPS) | 11,316,000 | ||

| Civilian labor force (CPS) | 155,486,000 | ||

| Unemployment rate (CPS) | 7.3% | ||

| Labor force participation rate (CPS) (as of Aug 2013) | 63.2% | ||

| Average monthly population growth rate (last year’s rate of growth): | 0.077% | ||

| Based on the assumed labor force participation rate and monthly population growth rate, the following monthly growth rate for the labor force is implied: | 0.0748% |

*August data, updated September 6, 2013, seasonally adjusted. Sources: U.S. Bureau of Labor Statistics, Current Employment Statistics (CES), and Current Population Survey (CPS), Federal Reserve Bank of Atlanta.

If we base the calculation on the average monthly change in payroll employment, we would need 197,222 new jobs every month, over the next 12 months, to achieve the target unemployment rate of 6.5%.

If we based the calculation on average monthly change in household employment, we would need 209,588 new jobs every month over the next 12 months to achieve an unemployment rate of 6.5%.

While data show that job creation is growing, revisions to expected data continue to prove the metrics wrong:

“The change in total non-farm payroll employment for June was revised from +188,000 to +172,000, and the change for July was revised from +162,000 to

+104,000. With these revisions, employment gains in June and July combined were 74,000 less than previously reported.”

America will need to create at least 200,000 jobs every month for the next 12 months to reach an unemployment rate of 6.5%.

Of course, as more people leave the workforce and give up looking for jobs, we could reach this number sooner.

Furthermore, as I mentioned in my letter, “The Shocking Truths About the Labour Market”:

While the media continues to tell you that job numbers are improving and unemployment is shrinking, the real labor market and recent unemployment numbers may actually be a lot worse than the Bureau of Labor Statistics (BLS) will have you believe.

And this isn’t just coming from me – even though I have written many letters in the past regarding true unemployment numbers and how they are derived.

This is coming directly from a previous BLS commissioner, Keith Hall.

Via the NYPost:

“Keith Hall believes the US economy is a lot sicker than the 7.6 percent unemployment rate would lead you to believe.

And he should know.

Hall was, from 2008 until last year, the guy in charge of Washington’s Bureau of Labor Statistics, the agency that compiles that rate.

“Right now [it’s] misleadingly low,” says Hall, who believes a truer reading of those now wanting a job but without one to be more than 10 percent.

The fly in the ointment is the BLS employment-to-population ratio, which is currently at 58.7 percent. “It’s lower than it was when the recession ended. I think that’s a remarkable statistic,” says Hall, a senior research fellow at the Mercatus Center at George Mason University in Fairfax, Va.

That level tells Hall the real unemployment rate is actually about 3 percentage points higher than the BLS number. If the jobless rate is unacceptable at 7.6 percent, it’d be shockingly bad if he is right and the true rate is 10.6 percent.

How could they be so different?

…Hall confirms that the jobless rate that makes the headlines – called the U-3 by BLS – doesn’t take into account people who have stopped looking for work but does count as employed folks who have worked as little as an hour during the preceding month.

A broader (and more accurate) measure of the state of US labor – called U-6, which includes the underemployed – jumped sharply in June to 14.3 percent from 13.8 percent the month before.

Hall reckons there are millions of U-6 people on top of the 4.5 million long-term unemployed.

…”This has been a very slow, very bad recovery,” he says. “And I think the numbers have really struggled as a result. In fact, I’ve been very disappointed in the coverage of the numbers.”

…There are other problems with numbers coming out of BLS, according to Hall. And they will just add to the confusion.

All parts of Washington’s data-collecting machine adjust to smooth out the bumps caused by the seasons of the year. But the recession that started five years ago was so severe and the recovery so anemic that the seasonal adjustments have been thrown off.”

Whether it’s via the printing press (QE) or keeping rates ridiculously low (free money), the Fed won’t stop until it reaches its targets.

The Fed’s goal of artificially inflating asset prices, and thus building confidence, has worked – especially on the stock market.

But the problem is that while confidence is often a self-fulling prophecy on Wall Street, it generally doesn’t last.

So what happens when this confidence is taken away? What happens when the Fed actually tapers, and eventually stops stimulus altogether?

Despite the fact that tapering means reducing the amount of stimulus without actually removing it, it will begin to remove confidence from the market.

The Fed’s Double-Edged Sword

On one hand, announcements of continued stimulus means that stimulus hasn’t been working; on the other, removing stimulus removes confidence.

Remember when QE1 was first launched? Bernanke had already been talking about an exit strategy, for which I had written that we would likely see QE2 and 3 and beyond.

So here we are many years and QE’s later and the thought of a QE exit strategy has been replaced with the thought of tapering.

Despite trillions of dollars already injected into the system, labour participation continues to fall, food and energy prices are up, energy usage is down, consumer confidence is dropping again, and wages remain flat.

I won’t say much about how savings continue to shrink while debt continues to grow, because that’s exactly what the Fed wants.

The Fed is attempting to fix the 2008 over-leverage crisis, with more leverage.

QE has persuaded the market into believing things are better via artificially inflated asset prices as a result of borrowed money, but the real economy is nowhere near as rosy as the stock market makes it out to be.

Once the free money stops, the economy will come to a screeching halt.

But will the money stop?

Upcoming Concerns

We may be looking at a new Fed Chairman and the upcoming debt ceiling debates are likely to bring more volatility; even if the latter really is a non-event, as it has been for the past few years.

Europe still has many structural problems and most of them have never really been addressed. Emerging Markets appeared to have bottomed, but weak growth relative to expectations isn’t painting a clear enough picture. Countries with current account deficits are beginning to feel pressure in their forex and bond markets and I believe this is only the start of something much worse.

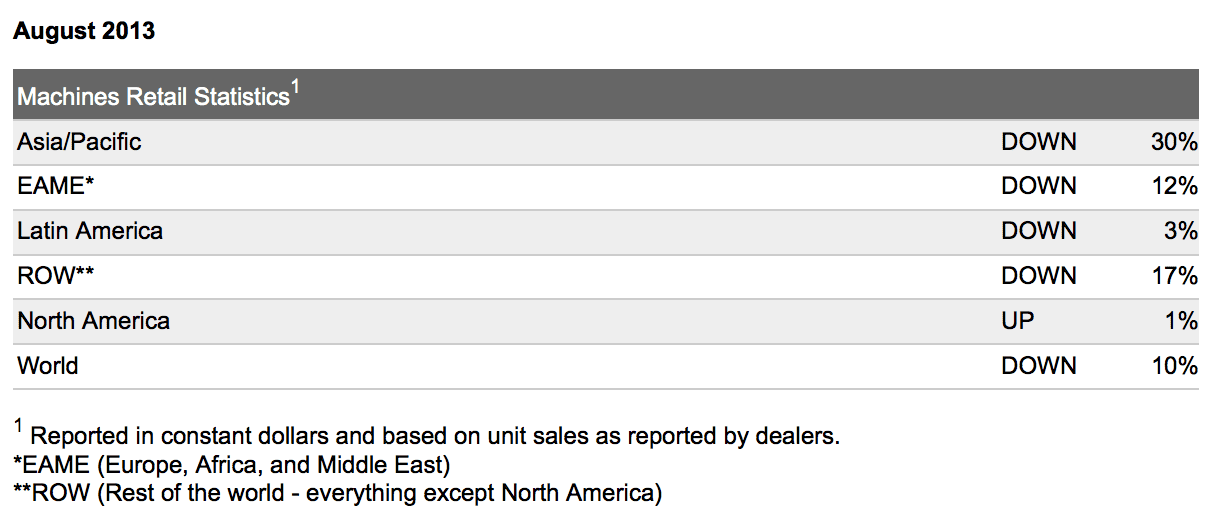

To get a small glimpse of how the world is contracting, let’s look at the retail sales of Caterpillar, a bellwether company, for the last month:

Overall, the economic backdrop is weak, the so-called housing recovery has been halted by rising rates, and there is a strong potential for tail risk events over the next few months that suggest we have likely peaked in consumer confidence. All of these are early warning signs for equity markets.

The debt ceiling will likely be raised dramatically, somewhere between $750 billion to $1 trillion – which proves that we’re riding a debt bubble that continues to grow at a very rapid rate.

While the Fed continues to give the media the grand illusion that tapering is a near-term October possibility and that a plan is in place to end QE, the truth is very simple: The Fed has no clue how all of this money printing will play out, let alone how to end it.

If the Fed wants to reach its targets, America needs to create at least 200,000 jobs every month for the next 12 months and overall prices needs to rise above the 10-year average.

If $85 billion a month in stimulus hasn’t even come close to achieving those numbers, do you think reducing stimulus (tapering) will?

Unless the American economy magically and ferociously roars back to life, don’t expect rates to rise or stimulus tapered.

If tapering is announced before the end of this year, its time to short the market. If we get a sniff of rising rates, short American automakers like GM and housing stocks first.

Gold and Silver Side Note

Bank of America decided to close their short position on silver, while Goldman all of a sudden sees near-term upside in gold, while also initiating buy signals on gold miners.

But don’t take this as a sign of higher gold and silver prices yet; we know Goldman is infamous for telling people to sell gold, even as they buy it, i.e. in Q2 when they added a record 3.7 million ‘shares’ of GLD while telling everyone to sell gold.

Perhaps they are selling into the buying.

Until next time,

Ivan Lo

The Equedia Letter

Of course we sell our gold and they buy it, so good reason to keep price down, when they have enough or not much selling then watch it go up up up and Goldman wins sellers lost!

Seems to me we have lost sight of the word RECESSION!!

THE CARROTS ARE COOKED. THERE IS NO WAY OUT WITHOUT DESTROYING THE ECONOMY ONCE AND FOR ALL AND START ALL OVER ON A NEW AND MORE SOLID FOUNDATION. AS FOR GOLD SOONER OR LATER IT HAS TO EXPLODE. IT IS SIMPLE. STOP QE. THE ECONOMY GOES BELLY UP STOCKS GOES DOWN, REAL EASTATE GOES DOWN, EVERY ASSET GOES DOWN. LETS NOT TALK ABOUT MONYE. IT WILL BE WORTH NOTHING. IT LEAVES YOU ONLY WITH GOLD..

If all assets go down, so will gold. Gold is an asset