Dear Reader,

We normally don’t do this. But one company just made an announcement that changes the entire sector.

Before we get there, it’s important you know what’s happening first.

Over this past weekend, American aircraft and warships struck roughly 140 military targets inside Iran — the second night of strikes in a row, and the heaviest barrage since President Trump declared the ceasefire over on July 7, after Iranian attacks on commercial ships in the Strait of Hormuz.

You’ve seen the headlines.

“US forces complete fresh wave of strikes in Iran, hit “dozens” of targets: CENTCOM”

“IRGC says it struck US base in Bahrain, Fars reports”

“Iran launches new wave of strikes toward US bases, IRGC says”

But there’s one headline from this weekend that you probably didn’t see, and it’s the one that EVERY investor should take notice of.

Buried beneath the war coverage, CNN reported that U.S. weapon stocks are becoming dangerously depleted, drawn down so far by the Iran conflict that Pentagon planners are now openly worried about America’s ability to fight the next war.

Via CNN:

“Key US weapons stockpiles remain significantly depleted and will come under even more intense pressure if strikes against Iran continue at the current rate, as President Donald Trump reiterated Friday that the ceasefire in the conflict is “over.”

The situation with armaments could impact the American military’s ability to fight a potential future war with China or even North Korea, experts told CNN.”

Just how bad is the situation?

“…If the war continues at the rate it’s been going for the last [five] days … it would reduce stockpiles enough that there would be a new, higher level of risk … with the Indo-Pacific,” said Mark Cancian, a retired Marine Corps colonel and defense analyst at the Center for Strategic and International Studies think tank.”

In other words, the most powerful military on earth is burning through its arsenal in real time.

Every strike package launched over Iran, every missile, every guided bomb, every round of ammunition, has to be replaced.

And here’s what almost nobody in the mainstream press will tell you:

America cannot currently replace them without China’s permission.

Now that is a problem.

Especially when you consider that, “the situation with armaments could impact the American military’s ability to fight a potential future war with China or even North Korea…”

This is where the story we’ve been tracking for over a year, is reaching a turning point.

The Metal Behind Every Trigger

Inside virtually every munition the United States fields, such as the primers that ignite the round, the detonators, the tracers, the infrared sensors that guide missiles to their targets, is a brittle, silvery metalloid most investors can’t pronounce.

Antimony.

The Department of Defense uses it in more than 200 types of ammunition alone because it does so many critical things. It hardens bullets and artillery shells, enables night vision, and flame-proofs aircraft electronics.

In other words, no antimony, no arsenal. It’s that simple.

But the supply situation isn’t.

In fact, it’s a disaster:

- The United States mines essentially zero antimony domestically.

- China controls roughly half of global mined supply and dominates the refining that turns ore into usable metal.

- In December 2024, Beijing banned antimony exports to the United States outright — and prices went vertical, from around $12,000 to nearly $60,000 per tonne.

- The November 2025 trade truce suspended that ban — but only until November 27, 2026, and the prohibition on sales to U.S. military end-users was never lifted.

So while American forces empty their magazines over the Persian Gulf, the Pentagon remains locked out of the world’s dominant antimony supply with the National Defense Stockpile sitting at its lowest levels since the Cold War.

We laid out this entire chain of dependency in April, in our letter “They Left a Fortune in the Desert,” and again in June in “A Trillion-Dollar Trade Hiding in Plain Sight” — where we showed you how critical minerals sit at the very bottom of the economic pyramid, holding up everything above them: the AI boom, the energy grid, the entire defense industrial base.

Remove the top of the pyramid, and you lose a product.

Remove the bottom, and everything collapses.

Washington finally understands this and is now urgently rectifying the matter. That’s why it has begun doing something the United States government almost never does: Picking winners.

And making their shareholders rich.

The $2.4 Billion Parable

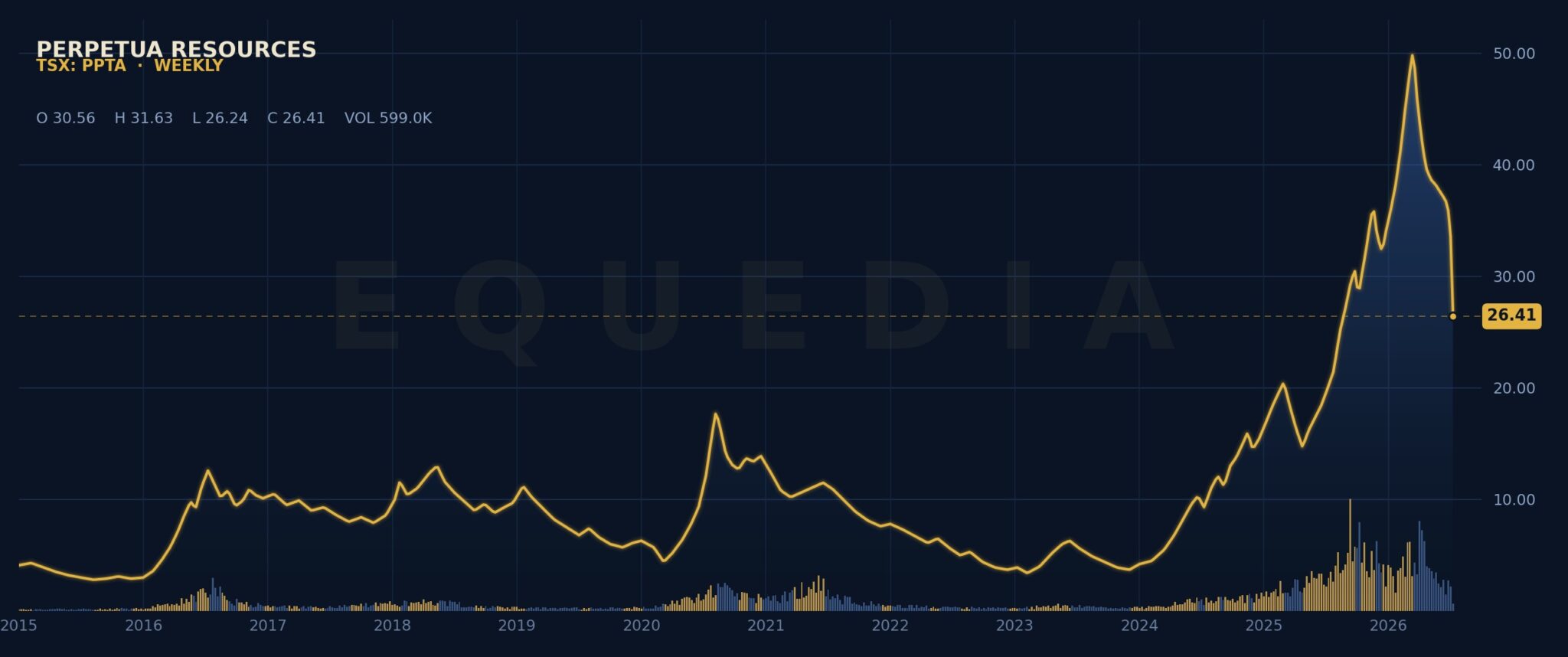

If you want to know what happens when Washington decides a mining company is a matter of national survival, you only need to study one stock: Perpetua Resources.

For the better part of a decade, almost nobody wanted this company.

It was called Midas Gold back then — a junior trying to redevelop the old Stibnite mining district in the mountains of central Idaho. On paper, it was a gold story. And as a gold story, it was, frankly, an underperformer: year after year grinding through one of the slowest permitting processes in American mining history, burning money, and seemingly going nowhere. The kind of stock that tests shareholders’ patience and then tests it again.

But buried in Stibnite’s ore body was something the market treated as a footnote: antimony.

The district had supplied America’s antimony during World War II, hence the name, Stibnite, after the antimony sulphide mineral itself.

Then the world changed.

China weaponized its antimony supply, waking up the Pentagon.

And that ignored footnote became the entire story.

Watch the sequence of what happened next:

- The Department of Defense awarded Perpetua approximately US$75 million to advance the project.

- The Export-Import Bank of the United States approved a staggering US$2.9 billion loan — one of the largest financings in American mining history.

- The U.S. Army showed up, literally, to celebrate the project as the future domestic source of antimony for its ammunition plants.

- Construction of the $1.3 billion mine is now underway.

And the stock? From under $4 to over $37 at its high. Today, Perpetua is a company worth roughly US$2.4 billion — and it isn’t expected to produce a single pound of antimony until at least 2029.

Now here’s the part we want you to hold on to, because it’s the key to everything that follows.

Perpetua’s asset is still the same, and the rocks didn’t change. The antimony was sitting in that Idaho mountainside the entire time the stock languished.

What changed is that Perpetua had a defined, compliant, independently signed-off resource of antimony — a hard number Washington could underwrite — at the exact moment the United States became desperate for domestic antimony.

You see, the government can’t fund a rumour, nor can it fund a project based on promising drill results. EXIM can’t lend $2.9 billion against a geologist’s hunch. The entire machinery of strategic funding — the DoD awards, the loans, the offtakes — switches on only when a deposit has been counted.

A defined resource is the ticket to the dance.

Which brings us to what just happened.

Because today, there’s a new number in America’s antimony ledger.

And it’s bigger than Perpetua’s publicly disclosed resource.

Its higher grade than Perpetua’s.

Its composition is fundamentally easier to refine. And because of that special composition, it could potentially produce antimony by next year.

And best of all, it belongs to a company trading at a tiny fraction of Perpetua’s value…

NevGold Corp.

TSX-V: NAU | OTCQX: NAUFF | Frankfurt: 5E50

Disseminated on behalf of NevGold Corp.

Longtime readers know this name well. NevGold’s Limousine Butte project is the story of gold miners at the old Golden Butte mine in Nevada who, back in 1989, stacked antimony-rich rock on their leach pads and walked away because nobody tested for antimony.

Readers who acted on our first coverage of this company have already had the chance to see their shares multiply.

At the time, our thesis rested on sampling, drilling, and our back-of-the-napkin math.

That era just ended.

On July 15, 2026, NevGold released its maiden Mineral Resource Estimate for Limo Butte — the first resource ever defined at the project in modern history, and the first by anyone in over seventeen years.

Before we show you the numbers, take a minute to understand what this actually is, because this is where the Perpetua lesson pays off.

The Counting House

A Mineral Resource Estimate (“MRE”) is the mining industry’s equivalent of a certified audit.

Until a company has one, drill results are mostly anecdote – especially from the perspective of the government. A spectacular drill hole is a fact about one skinny cylinder of rock, ten centimeters wide, in a mountain that stretches for kilometers. It can be impressive, but by itself, can only lead to speculation.

An MRE is what happens when an independent geologist takes every hole — in NevGold’s case, 977 drill holes totaling over 130,000 meters, drilled across four decades — builds a three-dimensional block model of the deposit, and estimates, block by block, how much metal is truly there.

The estimate comes in confidence categories (see Mining 101 to learn more):

Think of it like a business counting its wealth.

Inferred is metal the drilling strongly suggests is there, but hasn’t yet been pinned down — stock the manifest says should be in the warehouse, but nobody has walked the aisles and counted it shelf by shelf. Real enough to plan around, not yet something you’d sell as inventory.

Measured & Indicated (M&I) is metal drilled densely enough for the geologist to say: it’s there, we know its shape, we know its grade. That’s the audited inventory which has been counted, verified, and signed for. What it costs to turn that inventory into cash is the question the next studies answer.

That study is Reserve status, which is what M&I becomes once engineering and economic studies prove it can be mined at a profit. That’s money in the account. It’s the summit Perpetua spent a decade climbing, and it’s why a maiden resource is the milestone that starts the clock, not the one that ends it.

And the rock only counts at all if it clears the cut-off grade — carrying enough metal to plausibly pay for its own extraction, inside a conceptual open pit calculated here at US$3,000 gold and US$35,000-per-tonne antimony. Conservative assumptions, given where both metals trade.

This is the kind of geological report that transformed Perpetua from a story into a strategic asset.

And NevGold just told us where the starting point is.

The Numbers

Here is the maiden resource at Limo Butte, effective July 15, 2026:

Antimony — the defined higher-grade antimony zones:

- 29,600 tonnes of antimony, Measured & Indicated, at 0.26% Sb

- An additional 48,100 tonnes Inferred at 0.18% Sb

Antimony — total across the full resource:

- 31,800 tonnes M&I plus 75,700 tonnes Inferred — roughly 107,500 tonnes of contained antimony, or about 237 million pounds

Plus the gold, because Limo Butte is a dual-commodity system:

- 181,400 ounces Measured & Indicated at 0.37 g/t gold

- 1.20 million ounces Inferred at 0.32 g/t gold

- 100% oxide, starting at surface, amenable to heap leaching — the simplest, cheapest method of producing gold

Let’s run a crude estimate on the antimony alone: 107,500 tonnes at the US$35,000 per tonne used in the resource — the conservative price, well below the ~$60,000 highs — is roughly US$3.8 billion of in-situ metal.

NevGold currently trades at a market cap of 323.93 Million CAD, or approximately $230.57 Million USD (using a conversion rate of $0.7118 USD per CAD).

In-situ means what’s in the ground, before mining costs and recoveries.

And remember our back-of-napkin estimate from April?

We calculated the old Golden Butte leach pads, which are material already mined, crushed, and sitting in engineered piles on surface, held roughly 6,800 tonnes of recoverable antimony.

The MRE’s verdict on that at-surface, already-mined material, what NevGold calls “Project Jumpstart”: 6,900 tonnes of antimony, Measured & Indicated, at 0.28% Sb, plus another 500 tonnes Inferred at a remarkable 0.99% Sb.

Sometimes the napkin wins, but the MRE calculations did this time.

That surface material is the near-term production story, which is now advancing toward a Prefeasibility Study, targeting antimony production as early as 2027 – two years before Perpetua’s anticipated production.

In other words, there’s no blasting required, and they don’t need to create a new mine pit. The mining was done, and paid for, thirty-seven years ago.

Now line this up against the yardstick.

David, Meet Goliath

Perpetua’s Stibnite hosts the only antimony reserve in the United States: 149 million pounds, which is roughly 68,000 tonnes, at a grade of 0.06% to 0.07% antimony — within a total mineral resource of 216 million pounds at 0.07%.

NevGold’s maiden resource: roughly 237 million pounds of total contained antimony at an average grade of roughly 0.11% Sb across every tonne assayed for antimony.

NevGold’s antimony resource is not only bigger, but the grade is meaningfully higher than Perpetua’s — roughly 0.11% versus 0.06% to 0.07%.

But here’s what the average hides: antimony doesn’t spread itself evenly through the rock — it concentrates. The defined higher-grade antimony zones grade 0.26% Sb Measured & Indicated — roughly four times Perpetua’s grade. And “Project Jumpstart,” the already-mined material sitting at surface, runs 0.28% Sb Measured & Indicated, with the Pre-Strip Dump portion grading a remarkable 0.99% Sb.

What does that mean?

Picture it in physical terms: a tonne of Perpetua’s ore carries about a pound and a half of antimony. A tonne of NevGold’s resource averages more than two pounds. A tonne from the defined higher-grade antimony zones carries nearly six pounds — every truckload doing four times the work. And a tonne of the Pre-Strip Dump material sitting at surface? Nearly twenty-two pounds.

Now, to be fair — and we always are — Perpetua’s number is a reserve which has now been engineered, permitted, and financed. NevGold’s is a maiden resource, the earlier milestone, and much of it sits in the Inferred category that requires more drilling to firm up. Perpetua has earned its lead, and it’s significantly higher share price.

But that’s precisely what makes the comparison so compelling.

The market has already told you the price of a large, strategic, government-backed American antimony deposit: about US$2.4 billion, as of today. And early Perpetua investors have already reaped the rewards.

Meanwhile, NevGold just defined more contained antimony than Perpetua’s publicly disclosed resource, at a higher average grade — with Measured & Indicated zones grading four times Perpetua’s reserve grade, yet it trades at a small fraction of Perpetua.

Not only does Nevgold now have the largest antimony resource in the US, with Measured & Indicated antimony zones grading four times Perpetua’s reserve grade, there’s one more thing that makes NevGold’s antimony asset arguably superior.

And it’s a big one.

There’s a structural difference between these two deposits that could matter more than either the size or the grade – especially for Washington.

Stibnite vs. Oxide

Perpetua’s antimony is locked in stibnite, the sulphide mineral the project is literally named after. Sulphide antimony must be concentrated and then smelted, and the world’s antimony smelting capacity lives, almost entirely, in China. Sulphide chemistry is the industry’s standard headache, and every Western sulphide project has to solve it.

Consider this: even Perpetua — with more than US$80 million of Department of Defense backing and a massive multi-billion-dollar loan — is still at the pilot-plant stage of proving domestic processing, partnering with the Idaho National Laboratory on a modular demonstration facility to test whether military-spec antimony trisulfide can be produced from its ore on American soil.

Meanwhile, Nevgold’s antimony is oxide — minerals like stibiconite, which is what stibnite becomes after a few million years of Nevada weathering. Nature has effectively pre-processed the ore: rust instead of raw. This is important because oxide antimony dissolves in a controlled leach — closer to dissolving sugar than cracking a safe — and can be recovered as high-purity antimony metal right at the project site.

NevGold’s metallurgical test work has already demonstrated antimony recoveries of up to 85%, with sequential leaching recovering up to 99% of the remaining gold.

That means no concentrate, no smelter, no detour through Beijing, and no unknown refinery complications.

One deposit needs a supply chain that doesn’t yet exist in the West.

The other one is the supply chain.

And here’s where this letter stops being a direct comparison and becomes something far more interesting.

Scratching the Surface

While NevGold’s maiden MRE is now the largest antimony resource in the US, it’s actually still missing something.

It’s missing what could be the best rocks on the property.

In May, NevGold’s geologists sampled a feature called the Pre-Strip Dump, a pile of rock the 1989 miners shoved aside to reach the gold, taken from ground immediately beside two historical antimony mines: the Nevada Antimony Mine and the Lage Antimony Prospect. Both produced high-grade antimony during World War II — the last time Washington cared this much about the metal.

Here’s what they sampled:

- 53.71% antimony. More than half the rock, metal.

- 35.62% Sb. 24.32% Sb. 16.68% Sb. 16.27% Sb. 11.89% Sb.

- Six samples over 10%. Fourteen samples over 2%.

For context: the current grade of Perpetua’s resource is between 0.06-0.07% Sb. A surface sample running 53.7% isn’t a drill target; it’s practically inventory! One sample showed coarse, well-formed stibiconite crystals, large enough to see with the naked eye, embedded in a silica-hardened matrix. When a geologist sees crystals like that, they don’t think “fluke,” they think source.

And this is where the potential climbs even higher.

That dump material was dug from ground adjacent to those two WWII-era antimony mines — ground that, due to access constraints, NevGold has never drilled.

But they’re about to.

Those historical mines are being drilled this year. Two rigs are already turning at Limo Butte in a fully funded, 20,000-meter program, and the Nevada Antimony Mine and Lage Prospect are key targets on the list.

You know what that means?

The 237-million-pound resource was just defined without the highest-grade antimony ground on the property. The rocks lying on the surface next to those undrilled targets run as high as 53.7% antimony.

And the drills arrive this year.

That is what “scratching the surface” means when a geologist says it.

The Rug and the Floorboard

There’s a second reason this resource looks like a floor rather than a ceiling, and it’s written in the rocks themselves.

Limo Butte is a Carlin-type system, the same family of deposits that made Nevada the greatest gold jurisdiction in the world. In Carlin systems, hot mineral-rich fluids rise along faults and dump their metals into one particularly reactive rock unit.

At Limo Butte, that unit is the Pilot Shale — a dark, carbon-rich shale that acts like a chemical sponge, soaking gold and antimony out of any fluid that touches it. Where those fluids flooded it with silica, the shale hardened into jasperoid flinty, armored rock that is the system’s calling card.

Find the Pilot Shale, and you may have found the biggest prize.

For forty years, everyone believed the Pilot Shale had been eroded away east of NevGold’s Resurrection Ridge, because all you can see at surface there is older dolomite. So nobody drilled east.

Forty years later, NevGold’s team asked a different question: what if that dolomite isn’t below the shale — what if it was shoved on top of it?

It’s called a thrust fault: a slab of older rock pushed over younger rock, like a rug shoved across a floor until it buries the floorboards. Earlier explorers saw the rug and assumed the floor was gone.

But last year, in 2025, NevGold drilled through the rug.

Every single hole — a 100% hit rate — passed through the dolomite thrust plate and struck gold-antimony mineralization in the preserved Pilot Shale beneath. They called it the Bullet Zone discovery.

And mapping now shows the preserved shale extends more than a kilometer east of the old drilling — an entirely new corridor, essentially untested, now supported by geophysics.

But that’s not all.

The Northern Zones, which contribute 255,000 ounces of inferred gold to the new resource, carry no antimony numbers at all, because the historical operators never assayed for it — Just like in 1989 and just like the leach pads that were left behind. On a property where antimony accompanies gold nearly everywhere, those zones enter this resource without even being counted at all!

Now add it up. The undrilled WWII antimony mines: not in the number. The kilometer-long corridor under the thrust plate: barely in the number. The Northern Zones’ antimony: literally zero in the number.

In other words, despite being the largest antimony resource in the US, the maiden MRE is only the starting count.

Why This. Why Now.

Let’s connect the dots one final time.

- American weapon stocks are being depleted in real time by a shooting war with Iran — and every replacement round needs antimony.

- China’s export ban suspension expires November 27, 2026 — and its ban on military end-users never lifted at all.

- Washington has shown you its playbook, and its price: US$75 million in DoD awards and a US$2.9 billionEXIM loan for Perpetua — a company the market now values at US$2.4 billion, with production not expected until ~2029.

- The trigger for all of that government capital was one thing: a defined resource.

- As of July 15, NevGold has one: roughly 237 million pounds of contained antimony — larger than the only antimony reserve in America, at a higher average grade, with Measured & Indicated antimony zones grading 0.26% — roughly four times Perpetua’s — plus 1.38 million ounces of oxide gold, in Nevada, the top-ranked mining jurisdiction on earth.

- Its at-surface, already-mined material offers a path to production by 2027 — potentially the first new domestic antimony supply of this war.

- Its oxide chemistry means finished antimony metal on U.S. soil — no Chinese smelter or experimental modular refinery required.

- And the highest-grade ground on the property — surface rocks up to 53.7% antimony — hasn’t even been drilled yet. The rigs are turning now.

The company has stated it is advancing “strategic discussions around near-term antimony production.”

As CEO Brandon Bonafacio put it, “The Limo Butte Project in Nevada is one of the largest, most strategic, antimony-gold resources in the United States.”

And it hasn’t even scratched the surface.

In a market where the U.S. government has demonstrated — twice — that it will deploy billions behind domestic critical mineral supply, we’ll let you consider who might be sitting on the other side of that table.

Perpetua’s shareholders needed a decade of patience for their moment.

NevGold’s shareholders may need until November.

Seek the truth and be prepared,

Carlisle Kane

The Equedia Letter

NevGold Corp.

Canadian Trading Symbol: NAU

US Trading Symbol: NAUFF

German Trading Symbol: 5E50

Disclosure: This letter is disseminated on behalf of NevGold Corp. Equedia owns shares in NevGold Corp. Mineral resources are not mineral reserves and do not have demonstrated economic viability; inferred resources are considered too speculative geologically to have economic considerations applied to them that would enable them to be categorized as mineral reserves. Comparisons between NevGold’s mineral resource and Perpetua Resources’ mineral reserve involve different levels of geological confidence and project development. All resource figures are sourced from NevGold’s news release dated July 15, 2026; Perpetua figures from Perpetua Resources’ public disclosures, including its January 2021 Feasibility Study technical report (mineral resource statement effective December 22, 2020) and May 2026 investor presentation. Always conduct your own due diligence before investing. See full terms and disclaimer at equedia.com/terms-of-use.

Equedia.com and Equedia Network Corporation are not registered as investment advisers, broker-dealers or other securities professionals with any financial or securities regulatory authority. Remember, past performance is not indicative of future performance. This article also contains forward-looking statements that are subject to risks and uncertainties that could cause actual results to differ materially from the forward-looking statements made in this article. Just because many of the companies in our previous Equedia Reports have done well, doesn’t mean they all will. We are biased towards Nevgold (NAU) because the Company is an advertiser on www.equedia.com. We currently own shares of NAU. You can do the math. Our reputation is built upon the companies we feature. That is why we invest in every company we feature in our Equedia Special Report Editions. It’s your money to invest and we don’t share in your profits or your losses, so please take responsibility for doing your own due diligence and consult your own professional advisers before investing in NAU or trading in NAU securities. NAU and its management have no control over our editorial content and any opinions expressed in this article are our own. We’re not obligated to write a report on any of our advertisers and we’re not obligated to talk about them just because they advertise with us. For a complete disclosure of the compensation received by us from NAU, please review our Terms of Service and full disclaimer at www.equedia.com/terms-of-use/.

This newsletter (this “Newsletter”) is provided by Equedia Network Corporation (“Equedia”, “we” or “us”). Your access to and use of this Newsletter is subject to and governed by this disclaimer and Equedia’s Terms of Use, which is available at http://www.equedia.com/terms-of-use (the “Terms”). Please read this disclaimer and the Terms carefully. This Newsletter is not an offer to sell or a solicitation of an offer to buy any securities or commodities. To the extent that anything contained in this Newsletter may be deemed to be investment advice or a recommendation in connection with a particular company or security, such information is impersonal and is not tailored to the needs of any specific person. In addition to historical information, this Newsletter may contain forward-looking statements, including statements with respect to third parties regarding product plans, future growth, market opportunities, strategic initiatives, industry positioning, customer acquisition, the amount of recurring revenue and revenue growth. In addition, when used in this Newsletter, the words “will,” “expects,” “could,” “would,” “may,” “anticipates,” “intends,” “plans,” “believes,” “seeks,” “targets,” “estimates,” “looks for,” “looks to,” “continues” and similar expressions, as well as statements regarding a third party’s focus for the future, are generally intended to identify forward-looking statements. Each of the forward-looking statements we make in this Newsletter involves risks and uncertainties that may cause actual results to differ materially from these forward-looking statements. Factors that might cause or contribute to such differences include, but are not limited to, those disclosed by the parties referred to in this Newsletter in their public securities filings. You should carefully review the risks described therein. You should not place undue reliance on the forward looking statements in this Newsletter, which speak only as of the date such statement was published. Equedia undertakes no obligation to publicly release any revisions to the forward-looking statements or reflect events or circumstances after the date of their publication, except as required by law. As of the date of publication of this Newsletter, Equedia (on behalf of itself and any partner, director, officer or insider of Equedia) may have a financial or other interest in the party or parties featured in this Newsletter, within the meaning of National Instrument 31-103 – Registration Requirements, Exemptions, and Ongoing Registrant Obligations, published by the Canadian Securities Administrators. For full details of our compensation, please visit https://www.equedia.com/terms-of-use/.

As of the date of publication of this Newsletter, Equedia (on behalf of itself and any partner, director, officer or insider of Equedia) may have a financial or other interest in the party or parties featured in this Newsletter, within the meaning of National Instrument 31-103 – Registration Requirements, Exemptions, and Ongoing Registrant Obligations, published by the Canadian Securities Administrators. Equedia and its directors own shares of Nevgold (NAU) at the time of this writing. In July 2026, Equedia was paid $250,000 for three months of advertising services. We have also previously been compensated by NAU for advertising contracts, which have expired.