There is a heist happening right now.

It’s not in a Hollywood film, a novel, nor the evening news.

This is a real one.

It’s unfolding 80 feet below the streets of Manhattan, in steel vaults beneath Basel, in unmarked warehouses on the outskirts of Shanghai, and in the back rooms of every major central bank on Earth.

And nobody — I mean nobody — in the mainstream press is telling you about it.

So I will.

Last year alone, the world’s central banks quietly bought 863 tonnes of physical gold.

The year before that, over 1,000 tonnes.

The year before that, another 1,000+.

That’s nearly 3,000 tonnes of physical gold, all vacuumed off the market by the most powerful institutions on the planet.

And they’re not done.

Last month, the World Gold Council surveyed the world’s central banks and published a number that should’ve been on every front page.

95% of them plan to buy more gold over the next twelve months.

This is the highest share ever recorded.

Meanwhile, Wall Street is busy trying to sell you an AI chatbot that can summarize your emails.

Let me tell you what I think is really happening.

The U.S. dollar — the asset that has anchored global finance since 1944 — is being quietly, surgically, and strategically dethroned.

And gold has become the weapon of choice.

On January 29, 2026, gold closed at a record $5,595 an ounce.

Let that sink in for a second.

In my lifetime, gold has crossed $1,000, $2,000, and even $3,000 an ounce. And then, in the span of a few months, it crossed $5,000.

Today, it sits above $4,700 an ounce.

JPMorgan is now calling for $6,300.

Some respected analysts are even calling for $7,000.

And most retail investors have no idea what’s driving it – if they’re even participating at all.

This is not a trade, nor is it a simple trend.

This is a generational re-pricing of the world’s oldest asset.

And it is happening as we speak.

Now here’s where this gets interesting for you and me.

When gold moves like this, a small group of companies — sitting on the right rock, in the right jurisdiction, at the right time — all of a sudden become takeout targets.

We’ve watched it happen before with many of our past featured companies.

- Millennial Lithium — bought out for $400 million.

- MAG Silver — acquired for $4 billion.

- Newmarket Gold — taken over for more than $1 billion.

- Corvus Gold — sold to AngloGold Ashanti for $570 million.

Each of these companies was once a small, obscure name. Each one got to a market cap that looked “too high,” yet kept climbing. Eventually, each one handed its shareholders significant returns before a major came calling.

The pattern repeats because the math is the same.

And today, I want to introduce you to a company I believe is next in line.

A company whose shareholder register includes VanEck, the largest gold ETF manager on Earth.

A company with a strategic option deal signed with Kinross Gold, one of the senior producers in the sector.

Research initiated this past January by ATB Cormark Capital Markets with a price target implying triple-digit upside.

A company with a market cap of under C$200 million, yet it is sitting on what I believe has the potential to be one of the largest and highest-grade open-pittable gold projects that’s not already in production, in the lower 48.

In just a moment, I’ll tell you who it is.

But first, if we’re going to understand why this opportunity exists, and why timing matters so much right now, we need to step back and look at the forces rearranging the global financial map.

The World Is Moving On

For nearly 80 years, the U.S. dollar has sat on the throne of global finance.

Every major commodity, whether it’s oil, copper, wheat, or gold, has been priced in U.S. dollars. Every sovereign treasury has held a meaningful amount of U.S. debt. And every global bank has cleared its biggest trades through New York.

But something has fundamentally changed.

In 2022, the United States, alongside its allies, did something no one thought possible: it froze over $300 billion of Russia’s dollar reserves.

In one keystroke, Washington turned the world’s reserve currency into a weapon.

The signal this sent was unmistakable. If your country is one bad headline away from being on the wrong side of U.S. foreign policy, whether you’re a friend, a frenemy, or a full-blown adversary, then holding your reserves in dollars is no longer just inefficient; it’s a liability.

And the world responded.

Since that moment, central banks have collectively purchased more than 3,000 tonnes of gold.

That’s nearly three years of global mine output.

According to the World Gold Council, 2024 marked the third straight year central bank gold demand exceeded 1,000 tonnes, while 2025 closed with another 863 tonnes added.

In the most recent survey, 95% of central banks said they expect to grow their gold reserves over the next twelve months – that’s the highest share ever recorded

The message is clear: the rest of the world is diversifying away from the dollar, one ounce at a time.

The BRICS Aren’t Coming. They’re Already Here.

In October of last year, something historic happened. And almost no one in the Western financial press talked about it.

A BRICS-affiliated body known as the International Research Institute for Advanced Systems launched a pilot digital settlement unit.

A system 40% backed by gold and 60% backed by a basket of BRICS currencies.

This isn’t just some flashy new coin for traders. This is the quiet scaffolding of a real alternative to the U.S. dollar for international trade.

And get this: BRICS+ member states now collectively control roughly 50% of global gold production.

Between them, they hold over 6,000 tonnes of gold on official books:

- Russia: 2,335 tonnes

- China: 2,298 tonnes (and that’s just what they’ll admit to)

- India: 879 tonnes

Every month, another country signs a bilateral settlement deal with Beijing or Moscow that’s denominated in yuan, rubles, or commodity-linked baskets, bypassing the dollar entirely.

And while the dollar still dominates today, its dominance is diminishing.

In the early 2000s, the U.S. dollar accounted for 72% of global reserves.

By 2015, it was 65%.

Today, that number has dropped to roughly 57%.

Not only has the trend been one-way, it has accelerated.

$300 Trillion in Debt. Nowhere to Hide.

Now layer on top of all this the elephant that lives in every room you walk into.

Global debt has crossed $300 trillion.

The U.S. alone is approaching $38 trillion in national debt, growing by more than $1 trillion every hundred days.

Interest on that debt is now the single largest line item in the federal budget, surpassing defense spending.

There is mathematically no path out of this that doesn’t involve one of two things:

Default, or dilution.

And since defaulting on debt as a sovereign nation is economic suicide, dilution remains the only viable option.

That means more dollars printed, more inflation, and more pressure on real assets.

Central banks know this, and that’s why they’re buying gold — not as a speculation, but as a sovereign hedge against their own currencies.

When you have trillions of dollars that will eventually need to be inflated away, you need to own something that can’t be printed.

Gold fits the bill. Literally.

And Then Came the Trump Factor

On January 15, 2026, President Trump signed an executive order titled “Adjusting Imports of Processed Critical Minerals and Their Derivative Products into the United States.”

The executive order expanded the definition of “critical minerals” for the first time in U.S. history to include copper, uranium, potash, and, yes, gold.

Gold is now, officially, a matter of U.S. national security.

This sent gold ripping to record highs as traders poured in.

But think about what that really means.

Under the same national-security framework that governs semiconductors, rare earths, and defense equipment, domestic gold production is now priority infrastructure.

That means permitting timelines, often a major roadblock for gold mining assets, have been formally compressed. Tier-1 U.S. mining projects are being fast-tracked.

And most importantly, U.S.-produced gold is being positioned as strategic supply.

If you’re a major gold producer, you are scrambling right now to find high-quality, near-surface, domestic ounces.

But they have a problem: there aren’t many left.

U.S. gold discoveries have been in decline for thirty years because the easy deposits were found decades ago.

In other words, genuinely high-grade, near-surface, gold systems on patented ground in a Tier-1 state are vanishingly rare.

Now let me connect the dots.

The Setup

When you combine a rising gold price, shrinking reserve currency, desperate majors, and a tier one gold district in the U.S., you get one of the best setups I’ve seen from a junior mining company in a long time.

This is why institutional money is already positioning itself quietly.

And this is why I’m writing you today.

Because I want to introduce you to a company sitting right in the middle of this shift.

A company that already has on its shareholder register:

- VanEck — the world’s largest gold ETF manager, which holds approximately 10% of the company

- Kinross Gold — one of the world’s senior gold producers, which has signed a strategic option agreement on one of the company’s Nevada assets

In fact, earlier this year, ATB Cormark Capital Markets and SCP Resource Finance gave this company a C$2.75 and C$ 2.40 price target, respectively, nearly double where the company trades today.

And a company that just recently announced metallurgical results that demonstrate its potential to be a mine.

Introducing…

West Point Gold

(TSX-V: WPG | OTCQB: WPGCF)

Disseminated on behalf of West Point Gold.

Let me tell you why I believe this is one of the most important junior gold stories of the year.

“Underground grades at open-pit depths.”

“Gold Chain has the potential to be one of the highest grade development-stage open-pittable gold projects of significant scale in the lower 48.” – CEO Derek Macpherson

A Familiar Playbook — With a Bigger Prize

We’ve been covering junior miners for nearly twenty years – introducing our readers to less than one or two ideas per year.

But in that time, we’ve not only shared multiple ten baggers with our readers, but we also watched one pattern repeat itself over and over again.

It always starts with a small company. Then drill holes. A clear geological model. And a skeptical market.

Then, hole by hole, the rocks start to talk, and the system comes into focus. And somewhere along the line, a major steps in with an offer that would’ve been unthinkable a year prior.

For those who have followed this Letter from the beginning, you’ll surely recognize some of the following names that we featured:

- Millennial Lithium — “One of the Largest and Most Advanced Undeveloped Lithium Assets.” Sold for $400 million.

- MAG Silver — “The Most Important Silver Project in the World.” Sold for $4 billion.

- Newmarket Gold — “One of the Best and Most Undervalued Opportunities You Never Heard Of.” Sold for over $1 billion.

- Integra Gold — “Canada’s Next Takeover.” Sold for $590 million.

- Corvus Gold — Sold to AngloGold Ashanti for $570 million.

And these are just some of the ones that have been acquired. Many of our ideas are still trading at significant multiples today from our first introduction.

But we’re not mentioning this to boast about our track record. These examples are important because each of those stories started very similar to where West Point Gold sits today.

These aren’t just stories. They’re high returns and exits.

And the people running West Point Gold? They built several of them.

More on that in a moment. But first, let’s talk about the asset.

The Right Jurisdiction at the Right Time

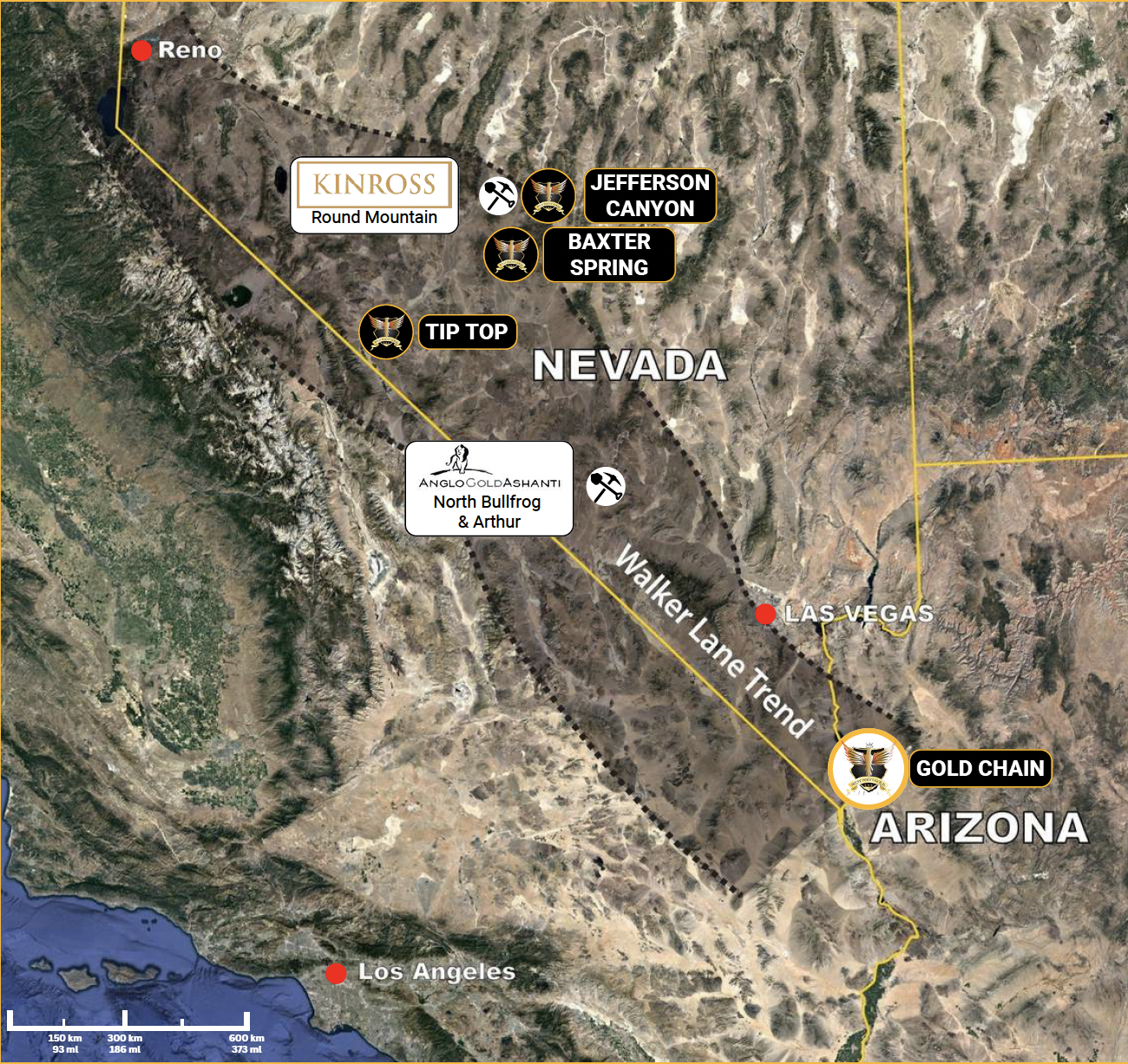

West Point Gold’s (WPG) flagship asset is the Gold Chain Project, a large-scale low-sulfidation epithermal gold system that sits on an 11,760-acre land package of patented and BLM ground in northwestern Arizona.

When we think of large-scale low-sulfidation epithermal gold systems and friendly mining jurisdictions, Nevada is the first state that pops up.

But here’s what many investors miss: Arizona is the only state in the U.S. that produced more non-fuel minerals than Nevada in 2022.

In fact, the Fraser Institute consistently ranks Arizona among the global top-5 mining jurisdictions.

This means friendly permitting, a cooperative Bureau of Land Management, and most importantly, a portion of West Point Gold’s project is on privately owned, patented land, with water rights.

And water rights are not only extremely advantageous for mining projects, but they are also an absolute necessity.

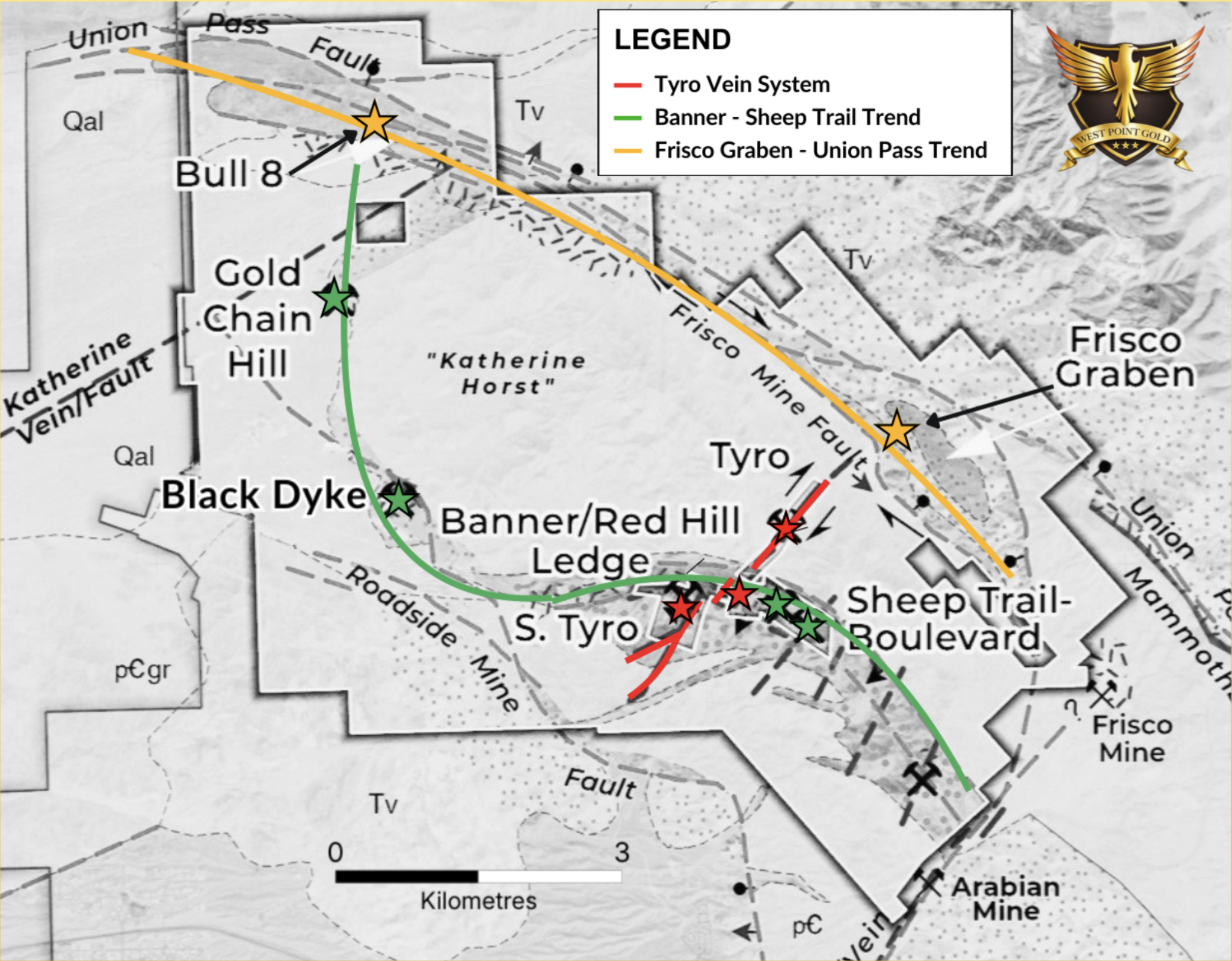

WPG’s Gold Chain sits right on the southern extension of the Walker Lane Trend.

If you know the Walker Lane, you know exactly why this is important.

This is the same geological corridor that produced:

- Round Mountain — Kinross, 20+ million ounces

- Bullfrog / North Bullfrog — AngloGold, 16 million ounces combined

- Goldfield, Tonopah, Rawhide, Aurora — the names that built American mining history

The Walker Lane runs diagonally from northwest Nevada across the state line into Arizona, and Gold Chain sits right on its southern extension, just 90 miles southeast of Las Vegas.

Corvus Gold’s North Bullfrog project, which was purchased by AngloGold Ashanti for $570 million in 2022, sits 90 miles northwest of Vegas. You can literally draw a straight diagonal line and hit the two projects.

For those who have been with us for many years, you’ll recall when we first introduced you to Corvus Gold and all of the reasons why we knew it would one day be acquired. We believe WPG is in a similar situation.

You see, Gold Chain sits on the same trend, has similar oxide-hosted mineralization, and has a similar near-surface profile.

The difference between Corvus Gold and WPG?

We believe WPG has better infrastructure, friendlier permitting, and direct access to water rights on its own patented land claims (Corvus did not have access to its own water rights).

And at a current market capitalization of less than C$200 million, West Point Gold has a lot of runway before the market starts pricing it like Corvus – especially since the price of gold has more than doubled since Corvus was acquired.

The Rocks: What’s Actually Happening on the Ground

We’ve been interested in WPG since it was restructured in 2024, but we wanted to see if our intuition on the Gold Chain project was correct before presenting it to you.

Of course, the only way to know is to see drill results.

Since 2024, West Point Gold has drilled approximately 120 holes totalling more than 35,000 metres at Gold Chain, with an 80%+ hit rate.

And that’s the result of a methodology, not luck. CEO Derek Macpherson and his team work from the known to the unknown by starting where mineralized structure is exposed at surface, prove it carries gold, then chase it laterally and at depth. That’s why the drill collars look scattered across the property: each one is anchored to a known mineralized outcrop that traces a 15-kilometre regional trend.

Their flagship target is the Tyro Main Zone, a 3.4-kilometre vein system hosting near-surface gold mineralization.

Take a look at some of the results from the last twelve months:

- GC25-87: 4m @ 9.56 g/t Au, including 13.7m @ 18.00 g/t

- GC25-88: 2m @ 5.46 g/t Au, including 18.3m @ 12.04 g/t

- February 25, 2026: 3m @ 13.48 g/t Au AND 32.0m @ 4.48 g/t Au in the same hole, extending the Northeast Tyro high-grade zone to over 300 metres of confirmed strike length

- Hole 49: 49m @ 4.73 g/t Au, including 30.48m @ 9.05 g/t

- GC26-116: 22.9m of 3.11 g/t Au from 102.1m to 125.0m

- GC26-125: 184.4m of 1.00 g/t Au from the surface and included 10.7m of 8.11 g/t Au from 96.0 to 106.7m and 35.1m of 1.31 g/t Au from 106.7 to 141.7m.

What does that mean for those who don’t really understand drill results?

(CLICK HERE to learn more about mining)

Let me put that into context.

The global average for open-pit gold mines is below 1.0 g/t, while the average open-pit gold mine in the southwestern United States runs at roughly 0.5 g/t.

West Point is hitting 3 to 18 times that grade — consistently — at depths that are still open-pit accessible.

Again, we stress that a mining company can get lucky with one hole. But when you add up continued positive drill results like that, it’s no longer luck – it’s geological signs pointing to a promising gold system.

April 9, 2026: A Third Resource Area Just Opened Up

Here’s where the story gets even more exciting.

First, a few kilometres from Tyro, drilling has just wrapped at a target called Black Dyke — a wide-open structural setting with historic mining and gold at surface, where management itself frames the size scope at 500,000 to 1,000,000 ounces if it works. Assays from the first six holes are pending, and an additional four-hole follow-up is already planned.

Then, just weeks ago, West Point announced drill results from its Sheep Trail target — located about 600 metres south of the Tyro Main Zone.

The highlight?

32.0 metres of 1.05 g/t gold, starting from just 9.1 metres depth.

Along with intercepts of 19.8m @ 1.42 g/t and 7.6m @ 2.41 g/t.

Those numbers alone would be a respectable discovery for most juniors.

But the real story is what those results could mean.

Sheep Trail has now shown a strike length of over 1 kilometre of shallow, near-surface mineralization — pointing to a third potential resource area on the same property.

Let that sink in.

Tyro Main is already a great discovery on its own, and Tyro NE was already a high-grade system.

But now a third potentially standalone zone is emerging, and it’s all in the same district.

As of this Letter, the Company has completed 15,173 metres of its 20,000-metre fully-funded drill program, with drilling set to continue at least until the end of May 2026.

This appears to be the beginning signature of a true district-scale system.

And the market is still only pricing in the first zone.

Recovering the Gold

Of course, having great drill results means little if you can’t get the gold out of the rocks.

Just last week, West Point Gold announced positive Phase 2 metallurgical results from the Tyro Main Zone.

And they look good:

- Gold recoveries up to 92% on milled material

- Gold recoveries up to 69% on crushed material via heap leach

What does that mean in plain English?

It means this gold can likely be extracted using conventional, well-understood, and lower-cost mining techniques — the same heap leach and milling methods used by many major Nevada and Arizona gold mines in operation today.

When you combine:

- Open-pit mining

- Near-surface oxide mineralization

- 90%+ recoveries

- And today’s ~$4,700 gold price…

You get what could potentially be one of the lowest-cost, high-margin gold operations you can build in the United States.

ATB Cormark Capital Markets modelled an all-in-sustaining cost (AISC) of approximately $950 to $1,100 per ounce for Gold Chain.

At $4,700 gold, that implies a margin of roughly $3,600 per ounce.

You don’t need a calculator to know what that does to project economics.

The Prize Below the Prize: Frisco Graben

Despite the continued positive drill results, there’s a piece most of the market hasn’t even begun to process. And it’s something that I am most excited about.

The high-grade Northeast Tyro zone doesn’t flatten with depth, and it doesn’t pinch out.

It actually gets better.

Most low-sulfidation epithermal gold systems cap out at about 300 metres of vertical extent, maybe 400 on a good day. Once the high-grade zone keeps getting better past that envelope, geologists call it telescoping — the signature of a fundamentally larger and rarer system underneath. Tyro’s high-grade zone is already plunging past the textbook 300-metre limit. If West Point pushes that envelope to 400, 500, 600 metres, the implications get very large, very fast.

Up until March 2026, West Point’s drilling at Tyro was effectively constrained by where its patented claims ended. Hole 91, the 21.3 metre @ 13.48 g/t intercept that drove the stock to a 52-week high, was the last hole drillable from that pad.

With newly granted federal permits, West Point can now set up rigs off the patented ground and drill underneath the claim block to a 300-metre vertical extent across the full one-kilometre Tyro strike, and chase the high-grade Northeast zone outward and plunging toward a structural feature called the Frisco Graben.

In gold geology, a graben is a down-faulted basin — the kind of structural trap where hydrothermal fluids concentrate over millions of years. These are the settings that built Comstock Lode, the Carlin Trend, and Goldstrike.

The Frisco Graben is a 4-kilometre by 750-metre covered target defined by major faulting, strong alteration, and geochemical anomalism.

West Point’s 2025 drilling already intersected widespread steam-heated alteration, a signature of a productive epithermal system sitting at depth.

The team now knows where to drill to test it.

There are two ways the market gets de-risked on Frisco between now and year-end.

The first: the new northeast step-out holes already drilled (assays pending) are designed to chase Tyro’s high-grade zone toward the Frisco Graben. If they hit, the high-grade zone strike could extend from roughly 300 metres to as much as 600 metres — a 30% scale increase in the highest-grade portion of the entire deposit, not in some lower-grade halo. Connecting Tyro structurally to the Frisco Graben fundamentally re-rates the entire camp.

The second is a brand-new target called Bull-8, sitting roughly 6 to 7 kilometres from the Frisco Graben, and on the same 10-kilometre Frisco Mine Fault that hosts it. High-grade rock samples have already been collected at surface. Assays from the first drill holes are pending. If Bull-8 hits, it proves that the very same regional structure carries gold from one bookend to the other, turning the Frisco Graben from a geological hypothesis into something very special.

If Frisco Graben turns out to be a productive deeper system, this could be a massive discovery.

In fact, that is why Mark Reischman came out of retirement for this project.

Reischman spent 40 years in the Walker Lane. He was Exploration Manager at Corvus Gold through its acquisition by AngloGold Ashanti. After that deal, AngloGold’s team went on to discover Merlin, a ~14-million-ounce deposit, with mineralization extending down to roughly 1,500 metres — extraordinary depth for a low-sulfidation epithermal system — right next door.

Reischman didn’t come out of retirement for Tyro.

He came out for Frisco.

The People Behind the Rocks

In junior mining, you bet on rocks — but you ride with people.

Let me introduce the ones steering West Point Gold.

- Anthony Paterson — Chairman. Helped structure and finance Prime Mining, sold to Torex Gold in 2025 for $450 million CAD. Founder of Patriot Critical Minerals Corp., the largest SEC-compliant tungsten resource in the United States.

- Andrew Bowering — Director. Co-founder of Prime Mining and Millennial Lithium (acquired by Lithium Americas). Chairman of Apollo Silver and American Lithium. Over $300 million raised in the past five years alone. Every public company he has launched since 1989 either remains listed or has been acquired.

- Derek Macpherson — President & CEO. Lead Director of Omai Gold Mines (market cap now approaching $1.5 billion). Former senior banking and research at Red Cloud Securities. Trained as a metallurgist. Understands both the ore body and the capital structure.

- Mark Reischman — Technical Advisor. Forty years in the Walker Lane Trend. Exploration Manager at Corvus Gold through its acquisition by AngloGold Ashanti. Came out of retirement for this project. Focus: the Frisco Graben — the target he identified on this property from day one..

Prime Mining, Corvus Gold, Millennial Lithium – all acquired.

In other words, the team has not only done it before, but they’re expecting to do it again.

Valuation: The Market Hasn’t Caught Up Yet

West Point Gold currently trades at roughly C$1.37 per share, giving it a market capitalization of approximately C$185 million.

At this price, West Point Gold sits in an interesting spot. Back in late February, the stock punched a 52-week high of $2.17 on the back of strong drill results out of the Tyro system, before it fell back to current levels (along with most gold stocks).

As most of our readers know, we share ideas based on a company’s long-term merits, not on short-term market trading fluctuations. Take our last antimony deal we first featured at C$0.50 (and again when it fell below $0.36). Well, it just hit a high of $2.28. In other words, the climb wasn’t straight up, but we stuck to our guns based on the merits of the project, and not just trading fundamentals.

That’s why you should know about the overhang.

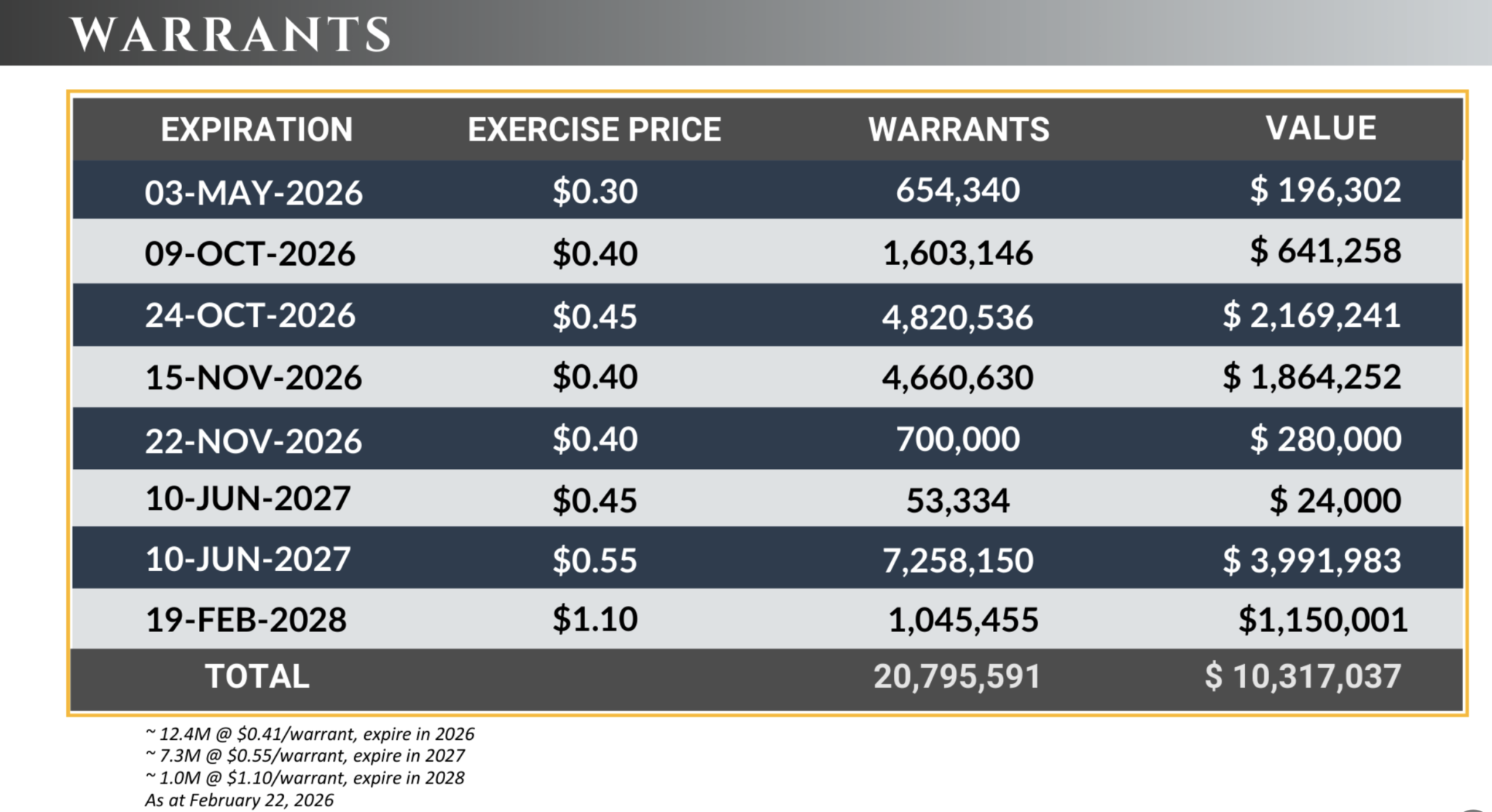

According to WPG’s disclosure dated February 22, 2026, the company has just over 20 million warrants outstanding, with an aggregate exercise value of roughly $10.3 million.

Here’s the breakdown:

All the warrants are currently in the money at $1.37.

When a stock has a meaningful pile of in-the-money warrants, it can act like a ceiling. As the share price rises, warrant holders have an incentive to exercise and sell into strength. That selling pressure can suppress the share price, particularly into resistance levels. New shares hit the float, and existing holders get diluted. It’s a real dynamic, and anyone who has watched junior miners long enough has seen it play out.

In WPG’s case, if all 20.8M warrants were exercised today, the share count would expand, adding to the market cap.

There’s also timing: roughly 60% of those warrants expire in 2026. Holders facing expiry have a forcing function: exercise or lose the option. That can compress selling into a tighter window.

Now, that doesn’t mean all of those shares will hit the market because the same overhang that looks like a headwind on a quiet day can look very different on a catalyst day.

The market already showed us what happens when strong drill results are released. When WPG shares hit $2.17 in February, it happened with this warrant structure already in place. The market cut through the overhang because the news was good enough. When you’ve got a company on the cusp of a maiden resource and continued positive drill results, the catalyst flow can override the supply pressure.

And WPG has a stack of catalysts coming.

Another thing to note is that if the $10.3 million of in-the-money warrants come in, it is essentially a pre-funded treasury. If those warrants get exercised, that’s $10 million in cash flowing into West Point Gold’s bank account. without a brokered financing, without a marketed deal, without warrant-and-share dilution at a discount to market. For a junior explorer that’s about to ramp drilling and march toward a resource estimate, $10 million of non-dilutive (relative to a financing) capital is the difference between cap-in-hand and cap-on-head. It funds the next drill campaign without management having to grovel for a bought deal at a 20% discount.

Furthermore, the strikes themselves anchor a floor. Warrant holders sitting on $0.30 to $0.45 paper are unlikely to dump everything at $1.37. They’re already up 3-4x and have been up even more when shares were trading about $2. Many of them are likely insiders, family, friends, and supportive institutions who participated early. In other words, they have skin in the longer-term story.

Lastly, WPG has a maiden resource targeted for the back half of 2026, plus 10,000+ metres of pending assays from the spring program, plus the metallurgical work continuing to de-risk the project. If the company delivers on what management has been telegraphing, “two at two” (2 million ounces at 2 g/t), the share price re-rating can happen while warrants are getting exercised. That’s a healthy distribution where WPG’s treasury fills, float expands, and the story keeps moving forward.

If management hits the milestones they’ve laid out, we believe the warrant exercises become a feature, not a bug. WPG ends up cashed up, drilled out, and walking into a maiden resource without ever having to do a dilutive raise to get there.

Now that you understand the warrants, you should also know that the company is fully funded through its 20,000-metre drill program.

ATB Cormark Capital Markets NPV5% on Gold Chain, modelled at $4,000 gold, came in at roughly $1.5 billion USD.

Gold is now $4,700.

A typical M&A premium for high-grade oxide gold in the U.S. is $500 to $700 per ounce in the ground, on the higher end for those in mine-friendly jurisdictions with water rights.

Cormark’s base case analysis for WPG’s gold resources is 1.5 million ounces. The company’s own exploration target is 19.5 to 31.2 million tonnes grading 2.0 to 3.0 g/t, which could potentially translate to 2 million ounces when the maiden resource is published later this year.

So let’s run some back-of-the-napkin math for a takeover value if WPG can show a 2-million-ounce resource later this year.

- 2 million ounces × $500/oz = $1 billion USD

- At $700/oz? $1.4 billion USD

Current market cap? ~C$185 million.

I’ve been doing this long enough to know that mathematical mispricings like this don’t last forever.

Especially if WPG continues on the same trend with drill results.

The Catalysts Between Now and Year-End

Here’s what sits on the calendar over the coming months:

- Ongoing drill results from the ~4,000 metres of unreleased assays already in the pipeline and 4,000m left to drill — dropping every two to three weeks through mid-July (drilling completes end of May)

- Pending assays from the new Bull-8 and Black Dyke targets — either of which could materially expand the camp narrative

- Maiden resource estimate at the Tyro Main Zone — targeted for late Q3 / early Q4 2026

- Potential Jefferson Canyon drilling — funded by Kinross, with results expected later in 2026

All of those can be catalysts for share price appreciation. But that last one is a big one.

When a maiden resource drops, a junior explorer stops being an “exploration story.” It becomes a valuation story where analysts (and potential buyers) are forced to apply a dollar-per-ounce framework.

And in a market where gold is above $4,700, and U.S. production is a matter of national security, the per-ounce valuations that follow could surprise a lot of people.

Conclusion

We are in the early innings of a generational shift in how the world views money.

For eighty years, U.S. Treasuries were the “risk-free” asset.

Now, sovereign after sovereign is waking up to the fact that “risk-free” comes with an asterisk when the issuer of that asset can freeze it with a phone call.

So they’re buying record amounts of gold.

BRICS+ nations now control roughly 50% of global gold production. They’ve launched a 40%-gold-backed digital settlement unit, while building a parallel financial architecture.

Meanwhile, the U.S. government just added gold to its list of critical minerals. This means permitting timelines are being compressed to encourage domestic production, which has been elevated to a matter of national security.

And underneath all of this, the supply side of gold is collapsing.

Global gold production has been flat for seven years. You cannot bring a new mine online in response to a price signal because it takes at least a decade to discover, permit, build, and ramp up.

So when you add it all up:

- Record central bank demand

- De-dollarization as a sovereign policy

- National security priority for U.S. producers

- Collapsing supply

- Gold above $4,700 — and some analysts calling for $6,000+

You get one of the most asymmetric setups in the commodity complex. And within gold, the juniors — the small, discovery-stage explorers — are the ultimate leverage.

In our view, West Point Gold represents one of the more compelling names in that bucket.

Because, unlike 95% of juniors, it checks the boxes that matter:

- High-grade, near-surface gold — with open-pit potential

- Patented ground in a globally top-5 mining jurisdiction

- Up to 92% metallurgical recoveries

- District-scale system with a second and third potential resource area already emerging

- A plunging, telescoping high-grade zone pointed at the Frisco Graben

- A CEO, Chairman, and Technical Advisor who have all built and sold mining companies to majors

- VanEck and Kinross on the register

- ATB Cormark Capital Markets coverage with a C$2.75 price target

- Fully funded through mid-2027

- Maiden resource estimate coming in late Q3 / early Q4 2026

This is Corvus Gold all over again (which was a previously featured company in this Letter) — except with gold at $4,700 instead of $1,800, and with a team that already knows how to cross the finish line.

Macpherson, who used to sit on the other side of the table as a senior gold-sector banker, framed it best himself. The corp-dev teams at the big gold producers such as Newmont, Kinross, Barrick and AngloGold are all hunting for the same checklist: 100,000 to 300,000 ounces a year of potential, first-quartile cash costs, a Tier-1 jurisdiction, and exploration upside. WPG already checks every one of those boxes.

As he put it: “Pre-resource, we’re a white pony with a little horn-nub. Once that resource comes out, we could be a unicorn.”

And that resource is coming out later this year.

Two years ago, when I first laid eyes on the Gold Chain project, it wasn’t time.

Today, it is.

West Point Gold Corp.

Canadian Trading Symbol: WPG

US Trading Symbol: WPGCF

German Trading Symbol: LRA0

Seek the truth and be prepared.

Carlisle Kane

The Equedia Letter

www.equedia.com

Disclaimer

Equedia.com and Equedia Network Corporation are not registered as investment advisers, broker-dealers or other securities professionals with any financial or securities regulatory authority. Remember, past performance is not indicative of future performance. This article contains forward-looking statements that are subject to risks and uncertainties that could cause actual results to differ materially from the forward-looking statements made in this article. Just because many of the companies in our previous Equedia Reports have done well, doesn’t mean they all will. We are biased towards West Point Gold (WPG) because the Company is an advertiser on www.equedia.com. We currently own shares of WPG. You can do the math. Our reputation is built upon the companies we feature. That is why we invest in every company we feature in our Equedia Special Report Editions. It’s your money to invest and we don’t share in your profits or your losses, so please take responsibility for doing your own due diligence and consult your own professional advisers before investing in WPG or trading in WPG securities. WPG and its management have no control over our editorial content and any opinions expressed in this article are our own. We’re not obligated to write a report on any of our advertisers and we’re not obligated to talk about them just because they advertise with us. For a complete disclosure of the compensation received by us from WPG, please review our Terms of Service and full disclaimer at www.equedia.com/terms-of-use/.

As of the date of publication of this Newsletter, Equedia (on behalf of itself and any partner, director, officer or insider of Equedia) may have a financial or other interest in the parties featured in this Newsletter, within the meaning of National Instrument 31-103. Equedia and its directors own shares of West Point Gold (WPG) at the time of this writing. West Point Gold has engaged Equedia as part of a paid advertising engagement; all expenses for third-party site advertisements arranged for WPG have been paid for by WPG. All drill results, resource targets, and forward-looking statements referenced in this Newsletter are sourced from West Point Gold Corp. public disclosures, including press releases dated February 25, 2026, April 9, 2026, and April 22, 2026, and the Cormark Securities initiation report dated January 13, 2026. Gold price referenced as of April 26, 2026.

Additional Forward Looking Statements

Certain statements contained in this presentation constitute forward-looking information. These statements relate to future events or future performance. Forward-looking statements include estimates and statements that describe WPG’s (the Company) future plans, objectives or goals, including words to the effect that the Company or management expects a stated condition or result to occur. The use of any of the words “could”, “intend”, “expect”, “believe”, “will”, “projected”, “estimated” and similar expressions and statements relating to matters that are not historical facts are intended to identify forward-looking information and are based on the Company’s current belief or assumptions as to the outcome and timing of such future events including, among others, assumptions about future prices of gold, silver, and other metal prices, currency exchange rates and interest rates, favourable operating conditions, political stability, obtaining government approvals and financing on time, obtaining renewals for existing licenses and permits and obtaining required licenses and permits, labour stability, stability in market conditions, availability of equipment, availability of drill rigs, and anticipated costs and expenditures.

The Company and Equedia cautions that all forward-looking statements are inherently uncertain, and that actual performance may be affected by a number of material factors, many of which are beyond the Company’s control. Such factors include, among other things: risks and uncertainties relating to West Point Gold’s ability to complete all payments and expenditures required under the Company’s Option Agreement with Kinross; and other risks and uncertainties relating to the actual results of current exploration activities, the uncertainty of reserve and resources estimates; the uncertainty of estimates and projections in relation to production, costs and expenses; risks relating to grade and continuity of mineral deposits; the uncertainties involved in interpreting drill results and other exploration data, the uncertainties respecting resource estimates, the potential for delays in exploration or development activities, the geology, grade and continuity of mineral deposits, the possibility that future exploration, development or mining results, statements about expected results and future dividends may not be consistent with the Company’s expectations due to accidents, equipment breakdowns, title and permitting matters, labour disputes or other unanticipated difficulties with or interruptions in operations, fluctuating metal prices, unanticipated costs and expenses, uncertainties relating to the availability and costs of financing needed in the future and regulatory restrictions, including environmental regulatory restrictions.

The possibility that future exploration, development or mining results will not be consistent with adjacent properties and the Company’s expectations; operational risks and hazards inherent with the business of mining (including environmental accidents and hazards, industrial accidents, equipment breakdown, unusual or unexpected geological or structural formations, cave-ins, flooding and severe weather); metal price fluctuations; environmental and regulatory requirements; availability of permits, failure to convert estimated mineral resources to reserves, the inability to complete a feasibility study which recommends a production decision, the preliminary nature of metallurgical test results, fluctuating gold prices, possibility of equipment breakdowns and delays, exploration cost overruns, availability of capital and financing, general economic, political risks, market or business conditions, regulatory changes, timeliness of government or regulatory approvals and other risks involved in the mineral exploration and development industry, and those risks set out in the filings on SEDAR made by the Company with securities regulators.

Although the Company believes that the assumptions and factors used in preparing the forward-looking information in this corporate presentation are reasonable, undue reliance should not be placed on such information, which only applies as of the date of this Press release, and no assurance can be given that such events will occur in the disclosed time frames or at all. The Company expressly disclaims any intention or obligation to update or revise any forward-looking statements whether as a result of new information, future events or otherwise, other than as required by applicable securities legislation.

Qualified Person

Robert Johansing, M.Sc. Econ. Geol., P. Geo., the Company’s Vice President, Exploration is a qualified person (“QP”) as defined by NI 43-101 and has reviewed and approved the technical content in this corporate presentation. Mr. Johansing has also been responsible for overseeing all phases of the drilling program at the Gold Chain project, including logging, core cutting, labelling, bagging and transport from the project to American Assay Laboratories of Sparks, Nevada. Samples were then dried, crushed and split, and pulp samples were prepared for analysis. Gold was determined by fire assay with an ICP finish, over limit samples were determined by fire assay and gravimetric finish. Silver plus 15 other elements were determined by Aqua Regia ICP-AES (IM-2A16), over limit samples were determined by fire assay and gravimetric finish. Both certified standards and blanks were inserted on site along with duplicates, standards and blanks inserted by American Assay. Standard sample chain of custody procedures were employed during drilling and sampling campaigns until delivery to the analytical facility.

Mineral resources which are not mineral reserves do not have demonstrated economic viability. With respect to “indicated mineral resource” and “inferred mineral resource”, there is a great amount of uncertainty as to their existence and a great uncertainty as to their economic and legal feasibility. It cannot be assumed that all or any part of a “measured mineral resource”, “indicated mineral resource” or “inferred mineral resource” will ever be upgraded to a higher category. Historical resources do not meet NI 43-101 standards, have not been independently verified by the Company and should not be relied on.

I always appreciate the effort that goes into the Equedia Letter. You work very hard to deliver outstanding ideas and opportunities.

Gold is an interesting topic. On the one hand, it is hard to fathom why it should have any value at all. It does not really do too much.Yet it is one of the first true tokens representing something it is not. Any commodity could work just as well. Why gold? Maybe sea shells or arrowheads were once the ticket.

I suspect there is something much deeper behind the value. Throughout history, it gets dug dug up out of the ground, formed into jewelery or bars and stashed away. It mostly just sits there. Hardly a useful item. It does not disappear through use. It can move around the planet with the rise and fall of empires. Because of its perceived value it became an object to be stolen, seized or manipulated.

At some point in human history the value of gold was implanted into the mind of man. It could be connected to the allegory of Cain and Abel. Cain represents the farming culture which destroyed the herding culture, represented by Abel. Once humanity started to settle in farming communities and cities they started t accumulate a lot of stuff. This attracts theives. The prosess of stealing the other guys stuff became a lucrative means of survival.

The reaction was protection, administration, armies, bureaucracies , walled cities, kings and a strata of classes. All this costs a lot of money which was not invented yet. Enter gold and taxes.

We are still stuck in the same situation today. There is no end to the methodology of stealing stuff from each other.

However, the future value of gold may be quite surprising. There is some speculation that it can be ionized and seeded into the atmosphere thus saving our planet or someone elses. Inertesting that it was chosen to be the commodity we hoard.