Dear Readers,

I am about to introduce you to a very special company.

Let me explain.

If there was one thing that mattered in my investment decisions, it would be people.

Nothing is more important than a management team’s ability to produce results.

I don’t mean just getting lucky with the drill by hitting high grades somewhere – lots of people can do that. I mean the uncanny ability to do it over and over again, while giving shareholders an incredible return for their hard-earned investment dollars.

This year, I’ve introduced many companies that have shown our readers great returns. I’ve reported on:

- A producer that’s increasing production and decreasing costs, while lagging in price when compared to peers

- Two takeover target, high-grade explorers directly next to producing, or near production, mines

The key similarity between all of them? A stellar management team with a track record of success.

Now I am about to show you the complete package; a potentially massive game changer in the Land of Gold.

This Company is a near-term producer with strong preliminary economic assessment numbers and blue sky, take-over target potential. It has:

- Strong capital structure with a low float, and only 325,000 broker warrants which should be exercised next month

- Excellent infrastructure; next to a major highway, power, and experienced local workforce

- Minimal production start-up costs

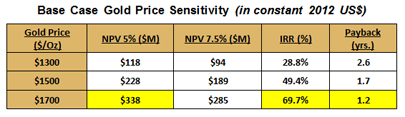

- Initial PEA highlights a payback period of just over one year (1.2 years) with current gold prices and 1.7 years at $1500 gold.

- A new high grade gold-silver vein discovery that is attracting the attention of majors everywhere

They’re also operating in one of the world’s most mine- friendly jurisdictions, and a place that has produced more gold per unit area than anywhere else in the world.

However, none of that would matter if the Company wasn’t backed by a stellar management team.

You Want Success?

How about a team that just recently raised more than $250 million and turned a $1 stock into a stock that climbed higher than $10?

How about a CEO that has led the discovery of five precious metal deposits in North America, all with over 1 million ounces of gold?

How about a CEO that has led the discovery of five precious metal deposits in North America, all with over 1 million ounces of gold?

We’re just getting started.

How about a CEO whose led the discoveries of nearly 40 million ounces of gold? This CEO has:

- Just recently led the discovery of the new Livengood Gold Deposit in Alaska which now has a total resource of 19.7 million ounces of gold and continues to expand.

- Led the discovery and development team for the Cripple Creek Deposit in Colorado, which is operated by AngloGold Ashanti and contains over 15 million ounces of gold.

- Led the discovery work on two other Nevada gold deposits; Yankee Mine & Elder Creek Mine.

That is an amazing track record. Just amazing.

Investors who missed their last venture, which turned a $1 stock into a stock that climbed higher than $10 in just a two short years, now has another chance at winning with the same management team.

They’ve changed the lives of many investors, turning average Joes into multi-millionaires.

Now they’re attempting to do it again. Only this time, management has a much bigger stake in this new company, than they ever had before.

They’re about to embark on a new project in one of the world’s best gold mining jurisdictions.

Nevada: The Land of Gold

Nevada has led the U.S. in gold production for many years; a strong feat considering the U.S. is the world’s third largest producer of gold.

In 2010, Nevada’s gold production represented 73% of all the gold produced in the U.S. That means Nevada alone accounted for 7% of worldwide gold production.

Before this year is over, Nevada will have cumulatively produced more than 200 million ounces of gold, representing 3.6% of all the gold ever produced in the world.

That’s all as a result of Nevada’s highly favorable geology.

While Nevada has produced millions of ounces of gold, it still has tremendous potential for the discovery of additional mineral deposits. Areas where prospective rocks exist beneath a cover of young, valley-filling sediments or volcanic rocks have only been explored to a limited extent, and ore deposits continue to be discovered in and near Nevada’s 526 historical mining districts.

In my view, Nevada is the single best overall jurisdiction for gold mining.

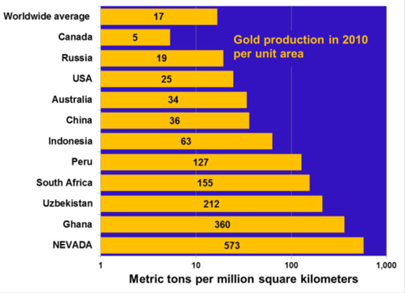

Take a look at this chart:

|

| Comparison of gold production in Nevada, measured in metric tons per million square kilometers of total area, versus the worldwide average (using area of land mass) and major producing countries.Source: Nevada Bureau of Mines and Geology 2010 |

It shows that Nevada is the world leader in terms of gold production per unit area.

|

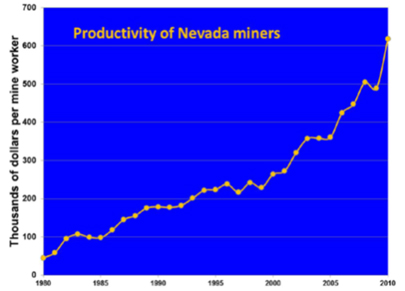

| Source: Nevada Bureau of Mines and Geology |

Productivity of Nevada mining operations is exceptionally high. Measured simply by the value of the commodities produced divided by the number of employees, productivity of Nevada miners is outstanding.

On the average, every one worker in the non-energy mineral industry each produced $618,000 in mined products in 2010, an all-time high. With mineral prices soaring since 2010, this number has grown.

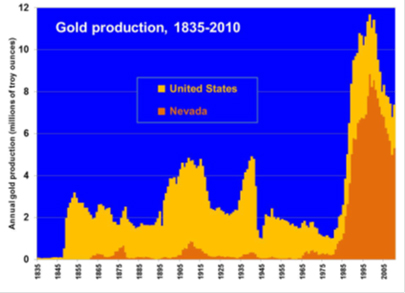

As a result of favourable geology and super friendly mining laws, Nevada continues to be in the midst of the biggest gold boom in U.S. history. Take a look:

|

| Source: Nevada Bureau of Mines and Geology |

It’s clear that Nevada is one of the world’s best gold mining jurisdictions.

Do the Math

What happens when you combine an extremely capable management team who’s made millions for investors, with an extremely favourable project in the world’s best gold mining jurisdiction?

You get my next big investment:

Corvus Gold Inc.

(TSX: KOR)

(OTCQX: CORVF)

Corvus Gold Inc. is led by Director and CEO, Jeffrey Pontius. He’s the CEO I just told you about that has made nearly 40 million ounces of gold discoveries.

After making millions of dollars for investors recently, he and his team are now completely focused on Corvus Gold Inc. (Corvus) Corvus’ main asset is its 100% owned North Bullfrog project in Nevada, which is on the fast-track to gold production by late 2014.

It already has a resource of over 1 million ounces and an initial PEA that shows a payback period of 1.2 years at current gold prices.

The near-term production story, low market cap, strong capital structure, and incredible management credentials are more than enough to make institutions take notice.

But there’s something more in the works.

Corvus is onto something that is attracting serious attention from a lot of majors; this something could be a massive game changer.

I needed to see this story for myself.

So I flew into Vegas last week to take a look.

The Site Visit

After a nice breakfast, we drove out on the desert highways of Nevada. The drive was easy and was no more than two hours away from downtown Vegas where I was staying.

Some minutes before reaching the site, we drove by Barrick Gold’s historic Bullfrog mine. There was no doubt that this area was once a booming mining county.

As a result of low gold prices, however, gold mining stopped. You can see this clearly reflected in the town’s distraught energy. But I could tell there was hope.

Along the way we stopped by a small candy shop near Beatty, a town just a few km’s away from Corvus’ planned mine site and it seemed the locals clearly knew about Corvus’ plan to put North Bullfrog into production.

|

| Source: Adam Kliczek / Wikipedia. CC-BY-SA-3.0 |

The locals need jobs and they were extremely pleased that Corvus could potentially give their little town new life. After a few minutes of driving, we arrived at North Bullfrog.

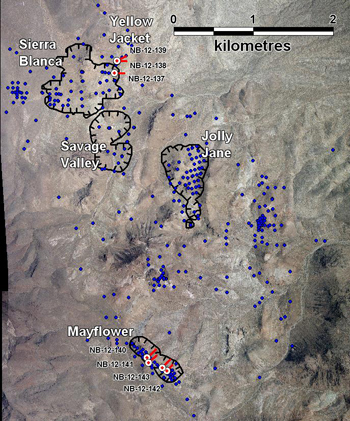

The North Bullfrog Project

The North Bullfrog project is located in north-western Nye County, Nevada in the northern Bullfrog Hills. It covers approximately 43 square kilometres in southwestern Nevada and is less than 2 hours away from Las Vegas.

The project lies within the Walker Lane structural terrain, just north of Barrick Gold’s Bullfrog mine, which produced 2.31 million oz. of gold and 3.0 million oz. of silver between 1989 and 1999.

It consists of several gold-bearing zones including the south area and Phase 1 Mayflower target and north area targets of Yellow Jacket, Jolly Jane, Sierra Blanca, and Savage Valley.

It consists of several gold-bearing zones including the south area and Phase 1 Mayflower target and north area targets of Yellow Jacket, Jolly Jane, Sierra Blanca, and Savage Valley.

The project site is just metres off the main highway and most mineralization sticks up out of the ground in several hills and shallow valleys, as a result of being a deposit primarily hosted in a volcanic unit known as the Crater Flat Tuff. The oxide mineralization covers several hills and it’s so big that the visible alteration in the best host rock goes on for kilometres. Much of the mineralization are in these hills which means Corvus can start mining ore right out of the gates, with no “pre-stripping” requirements; a major advantage, especially for the first few years of operation where costs can run high. As a result, the whole project has a minimal strip ratio of 0.41:1, with the initial stages having almost no strip.

(Strip ratio refers to the ratio of the volume of overburden (or waste material) required to be handled in order to extract some volume of ore. For example, a 3:1 stripping ratio means that mining one cubic meter of ore will require mining three cubic meters of waste rock. The lower the strip ratio, the better.) Furthermore, the many valleys on the property make it extremely easy to place waste dumps and leach pads. One look at the topography and you can see exactly where Corvus plans to put these things.

Take a look below. I am standing right on a hill at the Mayflower zone where they will be mining and you can clearly see the areas where the leach pads and waste dumps could go:

The site has great infrastructure. There is a power line that goes right onto the project, a workforce nearby all needing jobs, and it wouldn’t take them much to get water to the site. As a result, upfront capital costs for Phase I is less than $30M.

There’s a lot of potential at North Bullfrog and my site visit clearly confirmed that. Corvus has already announced a high grade feeder zone (a very significant event which I’ll explain in a bit) and their geo’s have identified changes in rock alteration and chemical signatures that appear to lead to more high grade veins. That means they could, and should, find more high-grade zones; this could add a whole new dynamic to Corvus’ near-term, low cost production story.

Corvus’ President Dr. Russell Myers is out there right now drilling the high grade zone and I think he is onto it. There should be about 3 to 4 holes coming from that side soon and over the next few months, results should be coming out. Those results could be very important.

They are already hitting right now and they’re hitting the high grades all at open-pit depth. This is a huge plus because that could add a very good grade component to the front end of the North Area mining plan.

When you’re kick-starting production, it’s always good to get grade and ounces up front in the mine plan because it makes everything so much easier.

A Potential Buyout Target

Corvus may not only be on top of a new high grade discovery in Nevada, but the high grade component could be the catalyst for a takeover bid. At the very least, it’s going to significantly make the early stages of Phase II production even better.

If Corvus can continue to hit on the high grades at North Bullfrog, I’d bet the majors in the area would all take a stab at them.

(Corvus has already told me they have signed numerous confidentially agreements with majors in the area) Companies that are keen on the type of mineralization Corvus is finding include all of your classic Nevada operators: Newmont, Barrick, Kinross, and even Agnico Eagle, who wants to get a Nevada mine group going. Mid-tiers that are keen to have a Nevada prong to their production scenario could be also be interested in Corvus. They include the likes of Osisko (who just bought a massive land package in Mexico) and Allied Nevada ($4 billion market cap). There is a very broad scope of those interested in Nevada because everyone knows it is the place to be.

If you’re a company onto a new high grade gold discovery in Nevada, you’re going to have a lot of people watching – especially if you have a low market cap like Corvus.

Nevada is well-known for takeovers. Two years ago, AuEx Ventures was bought out by Fronteer Gold, who subsequently got bought out by Newmont last year. The majors want to consolidate this space because they know Nevada will be a leading gold producer for many decades to come.

Even without any more high grade finds (an unlikely scenario), North Bullfrog still makes complete fiscal sense. The project itself is as close to a no-brainer as you’re going to get. The widespread, low-grade gold mineralization found at the site already has the potential to make a very profitable operation. This is clearly shown in their most recent PEA.

Preliminary Economic Assessment (PEA)

North Bullfrog currently has a 43-101 recognized gold resource of over 1.6 million ounces. On February 28, 2012, Corvus released a PEA based on this resource which outlined a resource of 1.1M ounces – the other 0.5M ounces were not incorporated into the initial mine plan. The Company anticipates publishing an updated PEA outlining numbers behind a staged production plan later this month.

It shows a conventional open-pit, heap-leach operation; one of the cheapest and most cost effective ways of extracting gold from ore, allowing for lower grade deposits to be economically viable.

(One of our most recently featured companies – already up significantly since our initial report – uses this exact operation and they have shown their investors a significant return on investment since production began just a few short years ago.) The PEA conceptualises a 31,000 tpd operation, using 0.1 g/t Au cut-off, for a total of 142.7M tonnes of ore mined over a 12.8-year mine life. It projects an average annual gold production of 57,700 ounces, for a total of 746,855 recoverable ounces of gold at cash costs of $815/oz.

While it wouldn’t be considered a low cost producer, those numbers are a lot stronger than they appear, showing a payback period of only 1.2 years at current gold prices; 2.6 years should prices fall to $1300.

In short, the PEA shows:

- Indicated Resources 19.5Mt @ 0.32 g/t for 199k oz. Au

- Inferred Resources 123.3Mt @ 0.23 g/t for 890k oz. Au

- 747,000 ounces gold recoverable

- Average life of mine annual production of 57,700 ounces gold plus by product silver

- $815/oz. gold cash operating cost

- Low strip ratio of 0.41

- Avg. gold recovery of 69% (increasing with new test results)

- 13 year mine life

(Keep in mind that the initial PEA does not include any of the 2012 resource expansion drilling with high-grade gold potential)

I emphasize that the numbers used in the PEA are extremely conservative.

Opex and admin costs used in the PEA are higher than 75% of operating mines. The process costs used is higher than any other existing Nevada operations. The Capex costs used in the PEA are 15% higher than mines constructed in the past 24 months.

Also, the geometry and geology of North Bullfrog should allow this project to produce gold at some of the lowest mining costs. That means management could have used much more aggressive numbers in their PEA, but they’re using conservative costs to make sure this will work from a fiscal standpoint.

That means when management puts this into production, the numbers could be much better – not to mention that I expect gold prices to be significantly higher two years from now.

While the current PEA shows promising numbers with a short payback period, there is a much smarter, and shareholder friendly, way of making the project even better.

A Two Phase Approach

The Mayflower deposit at North Bullfrog currently sits on patented land. That means its private land and the permitting timeline for patented land in Nevada is around 6 months vs. the 18-24 months for non-patented land. As a result, management can easily fast track North Bullfrog into production by first commencing production at Mayflower to generate the cash required to pay for the development of the rest of the project. This not only means less dilution for shareholders, but a much faster timeline to production.

It also means significantly reduced cost requirements to bring this project to production status. Instead of the $68.8M required, as outlined in the initial PEA, Phase I development Capex will only be ~$28M and will produce ~40,000 ounces of gold per year over 3 year mine life (+ trickle down in yr. 4). Furthermore, Phase I includes their highest grade deposit, with high heap leach recovery rates (and improving), and no pre-stripping.

After Phase I is complete and producing, it will help pay for some of the expansion costs in the Phase II development.

Improving Recovery Rates

No amount of gold would make sense if it wasn`t recoverable. The initial PEA projects average Life of Mine recoveries of 68.6%. That number is more than sufficient to make the project viable, and is an above average recovery rate required to make a heap leach project sustainable.

However, recent metallurgical testing from the Mayflower and Savage zone using column leach tests, conducted on material with comparable head grades drilled in June, and announced this month, showed gold recoveries of 73%-84%; significantly higher than the 68.6% average reported in their February 28, 2012 PEA.

Easy Road to Permitting

North Bullfrog is in Nevada; one of the most mine-friendly jurisdictions on the planet. It’s also near local communities who once heavily relied on mining and have since been bleeding without it. I don’t see permitting being much of an issue. Also, Phase I production at North Bullfrog begins at their Mayflower zone, which is located on patented land.

In Nevada, patented land generally involves a less onerous and potentially faster permitting process than unpatented, federally owned land (permitting on patented land has an average six-month timeline, versus up to 24 months on unpatented land). That means Mayflower could begin production as early as Q4/14, positioning Corvus as a near-term operator.

Comparable Companies

If you want some immediate comparables, you could compare Corvus to Atna Resources ($180M market cap) who is constructing the Pinson project in Nevada.

Or a better comparison would be Midway Gold ($215M market cap), who is permitting the Pan heap leach gold project in White Pine County, Nevada. Midway Gold has completed a feasibility and is looking to produce in 2014.

Midway’s current feasibility study shows a mine life of 9 years, 648,800 recoverable gold ounces, capex of $99M, at a fully loaded cash cost of $824/oz.*

*Midway Gold, September 2012 presentation

In the initial PEA, Corvus’ is expected to have a 13 year mine life, produce 747,000 recoverable gold ounces with a capex of $68.8M ($30M Phase I), and a cash cost of $815/oz.

If Corvus’ feasibility study, scheduled for Q1 2013, show roughly the same numbers, why shouldn’t they have a market cap closer to Midway’s?

Corvus currently has a market cap of $70M, while Midway has a market cap of $215M. Corvus’ feasibility is coming out in just a few short months and they also expect to be producing in 2014.

If you want some comparables to what Corvus could become, I’d take a look at both Allied Nevada ($3.5 billion market cap) with their Hycroft project in Nevada, and Argonaut Gold ($913M market cap) with their production story in Mexico.

Allied Nevada and Argonaut have similar grades and both projects are producing about 100,000 ounces per year.

Both Companies started out small and used their early production story as important catalysts for corporate growth; using production to find more ounces.

While projects currently produce about 100,000 ounces per year, they have given shareholders a terrific return.

Corvus expects to be producing 100,000 ounces by the time they are fully operational in 2016.

Just Getting Started: Significant Upside Potential

Drilling continues to show and prove that North Bullfrog has significant potential for expansion.

This year, the drill program outlined resources in several areas of significant and apparently continuous mineralization that, with further drilling, should continue to improve. In the Mayflower zone, large-diameter core drilling intersected a massive quartz-adularia vein grading:

- 6.85 g/t Au and 1.91 g/t Ag over 1.1 m, within a broader zone grading 0.81 g/t Au and 0.67 g/t Ag over 54.4 m.

- 9.94 g/t Au and 6.26 g/t Ag over 6.1 m from a depth of 6 m.

Management has told me that these intersections, and the general higher-grade nature of the core drilling vs. previous RC drilling results, suggests the potential for higher overall grades in the updated resource estimate and PEA for Mayflower, which I expect to be released within the next few weeks. If this proves to be the case, the updated PEA should show much stronger numbers, which should lead to a higher valuation of its share price. Even more exciting are the results that came out of the Yellow Jacket target. Yellow Jacket is over 2km long and is a high-grade gold-silver vein system located less than 400m away from the Phase II, proposed Sierra Blanca pit.

As I mentioned earlier, Corvus announced that Hole NB-12-138 intersected:

- 72.4 m grading 1.74 g/t Au and 98.7 g/t Ag, including 4.3 m grading 20.0 g/t Au and 1,519 g/t Ag beginning at 40 m vertical depth

This result defines a thick, near-surface mineralized zone around the previously discovered high-grade vein, potentially expanding the Sierra Blanca open pit.

Meanwhile, Hole NB-12-139 encountered extensive explosive hydrothermal zones, indicating the target boiling zone lies below the high-grade quartz vein intersected in hole NB-12-138. This suggests more elevation-controlled high-grade mineralization at depth of the Yellow Jacket zone. Very promising stuff.

Without going into too much geo-talk, it means that Corvus has not only found one high grade feeder structure, but they have apparently figured out how to find more. This style of high-grade mineralization has produced exceptional deposits throughout Nevada and if Corvus can further define the potential of their deposit, it could be massive game changer.

North Bullfrog could contain millions of ounces, including some high grade zones, and there is serious blue sky potential as mineralization at all targets remain open in all directions.

Furthermore, there could be a high grade silver component to this story. Hole 12-138 showed that with such high grades, it would not be out of the question to ship silver concentrate to a nearby tolling mill. The current mine plan does not include the silver because the heap leach process would result in low silver recoveries. However, if the high silver grades continue, there may be a silver story to tell.

Of course, none of the upside potential and production numbers matter if management can’t execute.

Credentials and Experience to Deliver

Corvus has a world class team. They have delivered results in exploration and development that very few in the industry have.

I’ve already mentioned that Corvus’ CEO, Jeffrey Pontius, has led the discovery of nearly 40M ounces of gold, which is an incredible accomplishment on its own.

However, the rest of the Corvus team are also extremely capable men who have done it all before; some alongside Jeff. It includes:

- Dr. Russell Myers who led the discovery of several of Corvus’ projects and has nearly 30 years of experience;

- Carl Brechtel who has designed and developed various operations all over the world, was the prefeasibility manager for AngloGold Ashanti, and has nearly 40 years of experience;

- Mark Reischman who has over 25 years of experience on Nevada projects and has worked with many majors including Kinross, AngloGold Ashanti, Barrick, BHP, and Rubicon.

|

| Management Receiving the Colin Spence Award 2011 for excellence in global mineral exploration |

Not only does management have the credentials and experience, they just recently delivered a big win for investors with their last company, turning a $1 stock to over $10 in a few short years. They have shown they can raise money; raising over $250 million in the last few years alone.

In this market environment, being able to raise money is absolutely crucial.

Each member of the management team has 25 to 35 years of experience; all with successful track records.

I wouldn’t bet against these guys.

Don’t Blink: Upcoming Catalysts

There are lots of catalysts for Corvus to receive a higher valuation. In the next few weeks or so, Corvus should be updating their PEA to include more recent drilling, updated resource, mine plans, and updated metallurgical work.

The Company infill drilled 37 holes at Mayflower aimed at upgrading Inferred resources to the Indicated category.

The results so far from the core drilling showed higher-grade gold mineralization compared to RC drilling. That means the higher grade mineralization could have been underestimated in the current resource estimate. A resource update is expected within the next few weeks as part of the updated PEA. Also, recent bottle-roll leach tests on bulk samples taken from Mayflower showed similar or better recoveries than those from other deposits on the property; column leach tests showed significantly higher recoveries than before.

With higher grades and better recoveries, the economics of Phase I production could potentially, and significantly, be enhanced in the upcoming PEA.

The PEA should show:

- Mayflower can be a standalone project.

- Actual Phase I and II plan for the North Bullfrog in more detail

- Updated resource for Mayflower with higher grade and higher recovery based on on-going test work.

One of the more significant events that could boost share price is the feasibility study that is expected for Q1 2013 – which is just a few short months away.

With COO Carl Brechtel working on this, who was the Prefeasibility Manager for AngloGold Ashanti, you can expect him to deliver on the timeline.

Once the feasibility study has been completed, Corvus will submit the Plan of Operations to Nevada. Being on patented land, it shouldn’t take more than 6-9 months for Corvus to receive their permit for Mayflower. Once they receive their permit, its construction time.

Near Term Excitement

I mentioned earlier that Corvus may be on to a high grade feeder structure at depth. This is a very significant event that could be a massive game changer.

Corvus has not only found one high grade feeder zone, but management believes they have figured out how to find more.

If they do, it could blow this up into something more than a strong production story. Majors are watching; many have signed confidentially agreements and have been on the property since the high grade announcements. They know something much bigger is there; it’s up to management to find it. Given management’s track record of finding gold, I am betting they will.

Management has told me there should be 3-4 holes coming from the high grade targets. The drill will then be moved back to Mayflower for more drilling for the feasibility study in Q1 2013 and to follow up on the new vein system there. Then, in late November, the drill will move back up to Yellow Jacket to keep attacking the high grade.

There’s going to be a lot of news in the coming months and I think they’re going to be awesome.

With highly encouraging metallurgical results, continued drill success, and the presence of new high grade feeder zones, I see significant potential for the North Bullfrog project to evolve into a major new Nevada gold producing district.

But Wait, There’s More

Nevada isn’t the only place where Corvus has projects. It also controls 5 major projects in Alaska and Quebec, which I call the backstops for the Company.

Not only do their non-core projects have potential, Corvus doesn’t have to dilute shareholders to maximize their potential – most of them are partner funded. One of these include Terra; an Alaskan project that could give off some cash to Corvus from bulk processing test and initial gold production before the year is over.

They also have the Gerfaut project in Quebec which has potential for a major new copper-gold discovery. News from this project should be coming out soon.

October Buying Opportunity

October represents one of the best buying opportunities for gold and gold stocks. As I mentioned a few weeks ago in my Letter, “Watch the Throne“:

September is over and we’re now heading into a month where gold has traditionally not performed as well. We’ve seen gold and silver prices rise over the last few weeks, so it wouldn’t shock me that we see a pullback. October is also generally a more volatile month for both gold and stocks.

We’re seeing it right now; gold and gold stocks have not performed well this month, as predicted.

However, November marks a month where the bulls come back to play and those who get involved in gold and gold stocks have historically been well rewarded.

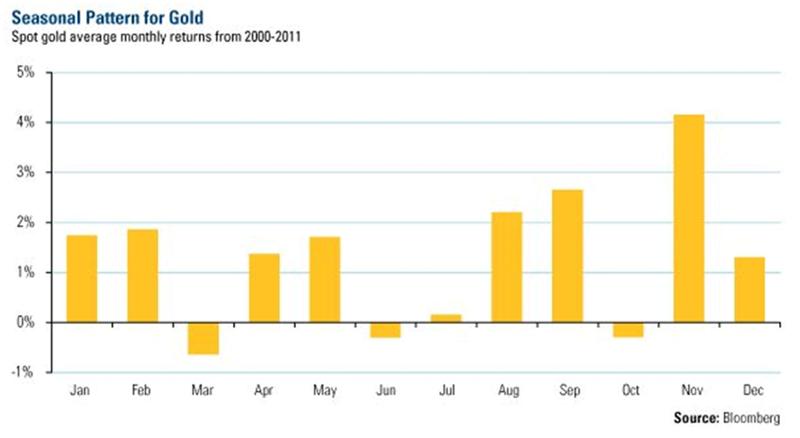

Should gold prices follow historical trends for October along with stocks, it would represent a great buying opportunity. Over the past 40 years, November has generally been one of the best months for gold, second only to September.

However, in the last decade, November has been the best performing month for gold by a long shot.

Take a look:

If the trend follows the same pattern as it has in the past 10 years, we’re going to see a nice surge in gold; with it, an even nicer surge in gold stocks.

The Bottom Line

Investing in the right people with the right project is the key to success. It significantly reduces risk, as a strong and capable management team is able to deliver results.

More importantly, these people attract money.

In an environment where financing has been extremely difficult, despite historically high gold prices, the ability to finance and attract big money is crucial. Many of the juniors are going bankrupt – even with great projects.

Why?

Because no one wants to take the risk in an unproven management team. Not in this market. The key to making money on a discovery is by investing in a company capable of executing, and raising money without excessive shareholder dilution. This is not an easy task. But for those who are capable, as Corvus’ management has shown many times in the past, the rewards can be extremely profitable.

No project has value unless it gives its investors a good return. That’s why Corvus Gold makes sense.

They have strong shareholders; with Tocqueville Asset Management, AngloGold Ashanti, and Management all each owning more than 10% of the Company. The float is small and management continues to buy shares – a big plus in my book. They’re also very capable of managing capital structure, with only 325k warrants ever issued; a true testament to management’s ability to not only raise money, but minimize dilution.

There are so many reasons why I liked Corvus; after visiting their property and speaking with management, I like them even more.

Corvus may be on to a new high grade gold discovery at North Bullfrog. And high grade gold discoveries in Nevada are a complete game changer and puts a bullseye on Corvus for a takeover. Combine that with a near-term production story and significant exploration potential, with all targets open in all directions, the Corvus story couldn’t get any more exciting.

That, along with many other reasons, is why Corvus is my next big investment.

More highlights of Corvus’ project and management credentials can be found below.

Corvus Gold Inc.

We’re biased towards Corvus Gold Inc. because they are an advertiser, we expect to participate in their most recently announced financing dated October 15, 2012, and we own options. You can do the math. Our reputation is built upon the companies we feature. That is why we invest in every company we feature in our Equedia Reports, including Corvus Gold Inc. It’s your money to invest and we don’t share in your profits or your losses, so please take responsibility for doing your own due diligence. Remember, past performance is not indicative of future performance. Just because many of the companies in our previous Equedia Reports have done well, doesn’t mean they all will. Furthermore, Corvus Gold Inc. and its management have no control over our editorial content and any opinions expressed are those of our own. We’re not obligated to write a report on any of our advertisers and we’re not obligated to talk about them just because they advertise with us.

Until next time,

Ivan Lo

Equedia Weekly

Questions?

Call Us Toll Free: 1-888-EQUEDIA (378-3342)

Disclaimer and Disclosure

Equedia.com & Equedia Network Corporation bears no liability for losses and/or damages arising from the use of this newsletter or any third party content provided herein. Equedia.com is an online financial newsletter owned by Equedia Network Corporation. We are focused on researching small-cap and large-cap public companies. Our past performance does not guarantee future results. Information in this report has been obtained from sources considered to be reliable, but we do not guarantee that it is accurate or complete. This material is not an offer to sell or a solicitation of an offer to buy any securities or commodities.

Furthermore, to keep our reports and newsletters FREE, from time to time we may publish paid advertisements from third parties and sponsored companies. We are also compensated to perform research on specific companies and often act as consultants to many of the companies mentioned in this letter and on our website at equedia.com. We also make direct investments into many of these companies and own shares and/or options in them. Companies do pay us to advertise on our website and we often distribute our reports on featured companies. While we are never paid to write a rosy and positive report on any company, we do market our reports using the advertising fees paid for by our featured companies.

This process allows us to continue publishing high-quality investment ideas at no cost to you whatsoever. Our revenue is generated by sponsor companies and we grow our readership by using the advertising fees we charge to distribute our reports. This helps both Equedia and our client companies gain exposure and allows us to provide you with our research at no cost.

Therefore, information should not be construed as unbiased. Each contract varies in duration, services performed and compensation received.

If you ever have any questions or concerns about our business or publications, we encourage you to contact us at the email or phone number below.

Equedia.com is not responsible for any claims made by any of the mentioned companies or third party content providers. You should independently investigate and fully understand all risks before investing. We are not a registered broker-dealer or financial advisor. Before investing in any securities, you should consult with your financial advisor and a registered broker-dealer. The information and data in this report were obtained from sources considered reliable. Their accuracy or completeness is not guaranteed and the giving of the same is not to be deemed as an offer or solicitation on our part with respect to the sale or purchase of any securities or commodities. Any decision to purchase or sell as a result of the opinions expressed in this report OR ON Equedia.com will be the full responsibility of the person authorizing such transaction.

Please view our privacy policy and disclaimer to view our full disclosure at http://equedia.com/cms.php/terms. Our views and opinions regarding the companies within Equedia.com are our own views and are based on information that we have received, which we assumed to be reliable. We do not guarantee that any of the companies will perform as we expect, and any comparisons we have made to other companies may not be valid or come into effect. Equedia.com is sometimes paid editorial fees for its writing and the dissemination of material and the companies featured do not have to meet any specific financial criteria. The companies represented by Equedia.com are typically development-stage companies that pose a much higher risk to investors. When investing in speculative stocks of this nature, it is possible to lose your entire investment over time. Statements included in this newsletter may contain forward looking statements, including the Company’s intentions, forecasts, plans or other matters that haven’t yet occurred. Such statements involve a number of risks and uncertainties. Further information on potential factors that may affect, delay or prevent such forward looking statements from coming to fruition can be found in their specific Financial reports. Equedia Network Corporation., owner of Equedia.com has been paid $9166 plus HST per month for 12 months which totals $110,000 plus hst of media coverage on Corvus Gold Inc. plus any additional expenses we may incur as a result of additional distribution. Corvus Gold Inc. has paid for this service. We have also been granted 150,000 options at $1.08 which expires on September 27, 2014 with a full vesting period of one year, by Corvus Gold Inc. Equedia.com may purchase shares of Corvus Gold Inc. without notice and intend to sell every share we purchase for our own profit. We may sell shares in Corvus Gold Inc. without notice to our subscribers. We currently do not own shares of Corvus Gold Inc., but we expect to buy shares by participating in Corvus Gold Inc.’s most recently announced non-brokered private placement financing dated October 16, 2012, because we believe in the Company’s ability to deliver results. The shares will have a hold period of 4 months from the date of closing.

Equedia Network Corporation is also a distributor (and not a publisher) of content supplied by third parties and Subscribers. Accordingly, Equedia Network Corporation has no more editorial control over such content than does a public library, bookstore, or newsstand. Any opinions, advice, statements, services, offers, or other information or content expressed or made available by third parties, including information providers, Subscribers or any other user of the Equedia Network Corporation Network of Sites, are those of the respective author(s) or distributor(s) and not of Equedia Network Corporation. Neither Equedia Network Corporation nor any third-party provider of information guarantees the accuracy, completeness, or usefulness of any content, nor its merchantability or fitness for any particular purpose.

check your payback periods