Dear Readers,

A few weeks ago, I introduced you to a tiny gold company sitting on what I believe could become one of the most important high-grade gold discoveries in the lower 48.

Since then, they kept drilling.

And just today, they announced something BIG.

Something that EVERY gold company wishes for.

I’ll tell you about it in just a moment.

But first, you need to understand why this matters — and why the timing could not be better.

Because while this little company was busy pulling high-grade gold out of the Arizona desert, the most powerful buyers on the planet were sending a message that almost nobody in the mainstream press bothered to report.

Let me explain.

The Buyers Who Never Sell Are All-In

Last week, the World Gold Council released its 2026 Central Bank Gold Reserves Survey.

Buried in it was a number that should have been on every front page.

A record 45% of the world’s central banks now plan to add to their own gold reserves over the next twelve months.

89% expect global central bank gold holdings to keep climbing.

And not a single central bank surveyed said it plans to sell.

Think about who we’re talking about here.

These are the most conservative, smartest, and powerful institutions on Earth. They don’t chase trends, they don’t chase hot trades — they exist to protect nations.

And right now, as a group, they are all leaning the same way at once — toward gold, and away from the dollar.

In fact, gold has now quietly overtaken U.S. Treasuries to become the single largest reserve asset in the entire world.

This is an extremely significant dataset.

For eighty years, the “risk-free” asset in the world was U.S. government debt.

Now, sovereign after sovereign is waking up to the fact that “risk-free” comes with an asterisk — especially when the issuer of that asset can freeze it with a single phone call.

This is the same story I laid out in a previous letter: BRICS nations building a parallel settlement system, Washington formally adding gold to its list of critical minerals, and the dollar’s slow, surgical dethroning as the world’s reserve currency.

Don’t think of gold as a trade, but rather a generational re-pricing of the world’s oldest money.

And don’t think Wall Street doesn’t know.

JPMorgan has called for $6,300 gold, while many analysts are even calling for $7,000.

Sure, gold pulled back last week — down to around $4,150 on a more hawkish Fed and an easing of Middle East tensions.

But step back and look at the bigger picture.

In my lifetime, gold crossed $1,000… then $2,000… then $3,000 — each milestone taking years.

Then, in a matter of months, it ripped past $5,000 to a record near $5,600 this past January.

Every single pullback along the way has been a buying opportunity.

And here’s the thing about a rising gold price: When gold moves like this, a tiny handful of companies — sitting on the right rock, in the right jurisdiction, at exactly the right time — suddenly become takeover targets.

We’ve watched it happen over and over again with the companies we’ve featured in the Equedia Letter.

The small boats rise the fastest.

And today, I want to show you one I believe is sitting in the perfect spot.

West Point Gold Corp.

(TSX-V: WPG | OTCQX: WPGCF | FSE: LRA0)

Disseminated on behalf of West Point Gold.

(Original report here: “By the Time You Read This, They’ve Already Bought More“)

For those of you just joining, here’s the quick version.

West Point Gold’s flagship asset is the Gold Chain Project, a large-scale, low-sulphidation epithermal gold system on roughly 11,760 acres of patented and BLM ground in northwestern Arizona’s historic Oatman District.

It sits on the southern extension of the legendary Walker Lane Trend. This is the same geological corridor that produced Round Mountain (20+ million ounces) and the Bullfrog district that AngloGold Ashanti has spent years and well over half a billion dollars consolidating.

It has water rights on its own patented land, a rare and absolute necessity for any mine.

It has VanEck, the world’s largest gold ETF manager, on its share register.

It has Kinross Gold, one of the world’s senior producers, with a strategic option deal on one of its Nevada assets.

And it has a management team that has built and sold mining companies to the majors before.

But none of that is why I’m writing you today.

I’m writing you because of what West Point Gold just announced.

This Changes Everything

First, let me give you a quick geology lesson, because it’s key to this story.

Most low-sulphidation epithermal gold systems — the kind West Point Gold is drilling — cap out at about 300 metres of vertical depth.

Maybe 400m on a really good day.

After that, they tend to pinch out, thin down, and die.

So the single most important question for a deposit like this is simple:

Does the high-grade keep going down?

Because when an epithermal system keeps getting better with depth instead of dying, geologists have a word for it.

They call it telescoping.

It’s the signature of a fundamentally larger, rarer, and more valuable system sitting underneath.

This is the question that separates a nice little discovery from a genuine company-maker.

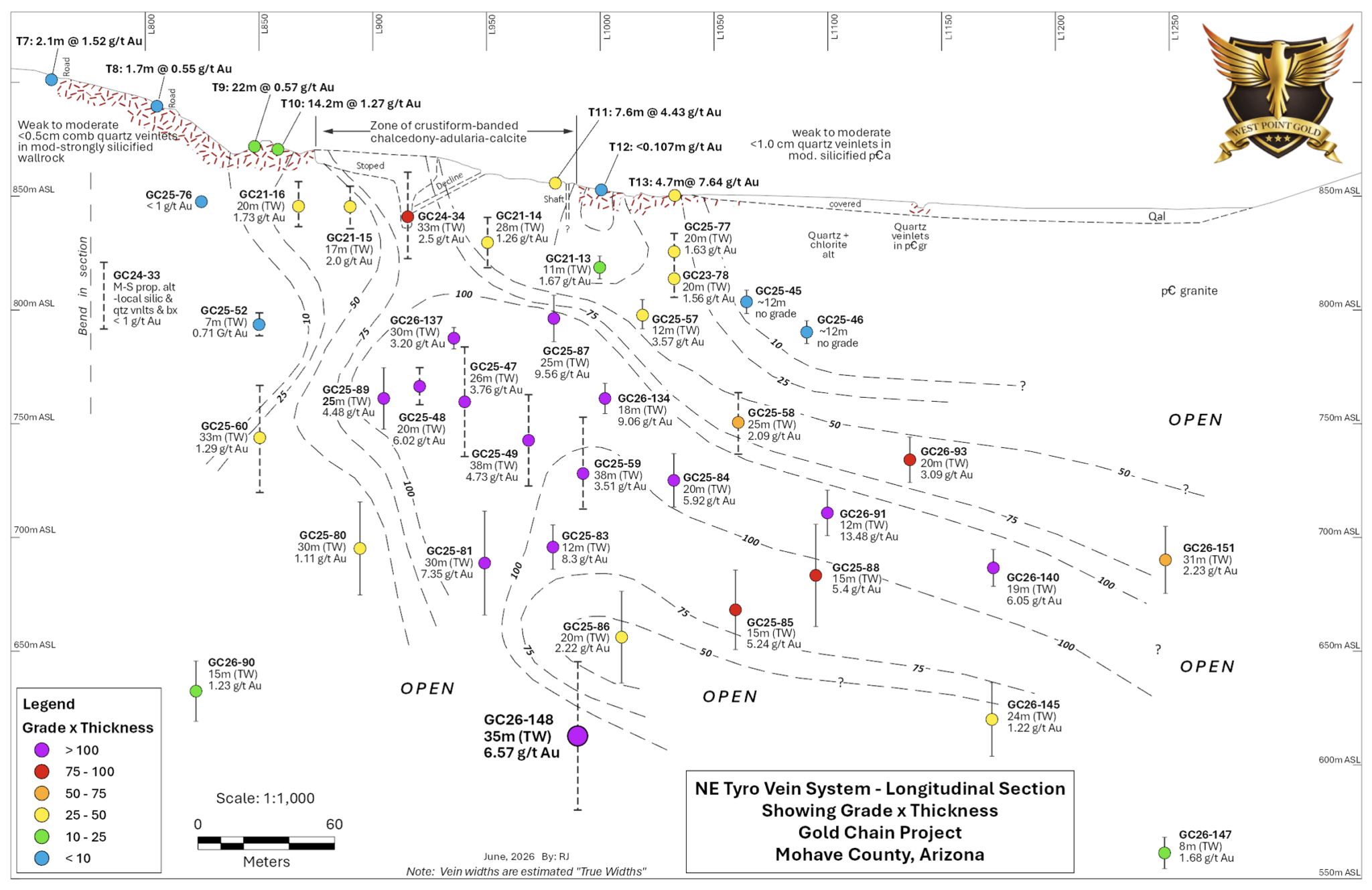

Now, West Point Gold’s Tyro Main zone is already a great discovery on its own, and Tyro NE was already a high-grade system.

In fact, drilling at Tyro NE has consistently returned with significant high-grade gold.

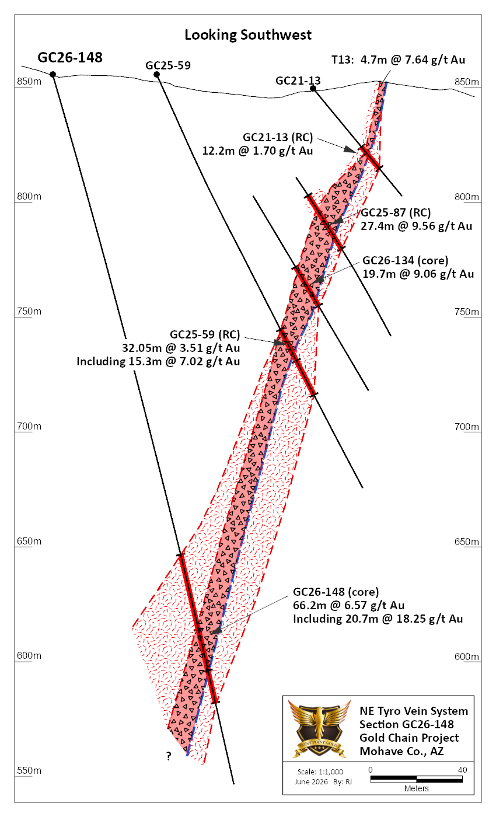

Just last month, the Company reported on two holes, GC26-134 and GC26-137:

- Hole GC26-134 returned 19.7m of 9.06 g/t Au from 95.8 to 115.5m, about 20m above GC25-059 (15.3m of 7.02 g/t Au).

- Hole GC26-137 returned 35.7m of 3.2 g/t Au from 53.2 to 88.9m, including 10.2m of 10.23 g/t Au, about 20m above GC25-047 (38.1m of 4.86 g/t Au including 10.7m at 8.64 g/t Au).

These not only further confirm and validate the high-grade discoveries made at the NE Tyro Zone in drill core, but are in line with or exceed many prior results and continue to showcase the robust widths and high-grade tenor of the system at NE Tyro.

But despite already being a high-grade zone with consistent drill results, West Point Gold has never drilled past 250m at Tyro NE.

Management believes there is much more there, so they deliberately targeted below their previous drilling at Tyro NE, around 250 metres beneath surface.

And they didn’t just nick the edge of the zone.

They drilled straight into the heart of it.

Today, the Company released the results of the GC26-148 drill hole. And it’s absolutely amazing.

Take a look:

- 66.2 metres of 6.57 g/t gold from 219 metres

- Including 20.7 metres at 18.25 g/t — a fat, high-grade core

Management calls it among the broadest (true width) and highest-grade intercepts ever drilled at the Northeast Tyro zone.

Those internal grades are roughly 35 times the average grade of an open-pit gold mine in the southwestern United States.

And here’s the part the market may not have fully processed yet.

This hole successfully extended the high-grade zone to more than 250 metres below surface — and the Company now says the zone is likely to remain open at depth even after its upcoming maiden resource estimate.

In plain English, it means that when they release the maiden resource — the first hard count of ounces — it almost certainly won’t capture the full size of this thing.

There will be a known, drilled, high-grade extension sitting below the resource boundary.

What the Geology Is Actually Telling Us

Now, if you pull up the company’s news release, the technical summary reads like a foreign language for those unfamiliar with geology.

Most readers would glaze over words like “crustiform-banded adularia,” “phreatic breccia,” and “bladed calcite lattice texture.”

But buried in that jargon is the real story. Because those boring-sounding details are exactly what a seasoned exploration geologist gets excited about.

So let me translate it for you, paragraph by paragraph, in plain English. Stick with me — this is where you learn to read the signs the pros are reading.

What they said: The intercept is a broad zone of quartz veinlets, stockwork and vein breccia over 66.2m, with an estimated true width of about 35m, and it appears to be an extension of a steeply plunging shoot.

What it means: Think of gold mineralization like plumbing. Hot, gold-rich fluids rose up through cracks in the rock millions of years ago and dumped their gold as they cooled. A “shoot” is a particularly rich, concentrated pipe of that gold — the fat part of the plumbing. The fact that this hole hit a “steeply plunging shoot” means they didn’t just clip a thin vein — they drilled into a thick, near-vertical column of gold that plunges down into the earth. And “true width of about 35m” matters enormously: a lot of drill results sound impressive until you realize the drill hit the vein at an angle, inflating the number. Here, even after correcting for angle, this is a genuinely wide body of gold. Wide plus high-grade is the combination you want.

What they said: The NE Tyro vein is a robust, uniform vein system that dips consistently and ranges from 10m to 35m wide, hosted in Precambrian granite.

What it means: “Robust and uniform” is geologist-speak for predictable. And predictable is worth its weight in — well, gold. Many gold veins are erratic; they pinch, swell, twist, and vanish, which makes them a nightmare (and hugely expensive) to drill out and mine. A vein that holds a consistent width and direction over a long distance is far cheaper to define, far easier to model into a resource, and far more likely to become an actual mine. The market pays a premium for predictability.

What they said: The mineralized zone is a multi-stage breccia cemented by several crustiform-banded stages of quartz-calcite-adularia, and one sample returned 1.73m at 62.7 g/t.

What it means: “Crustiform banding” means the gold-bearing minerals were deposited in layers — like rings on a tree — one event stacked on top of another. “Multi-stage” means the system didn’t fill with gold just once; it got recharged and refilled over and over again. Each pulse of fluid added more gold. This is a hallmark of a big, long-lived, healthy mineralizing system — not a one-and-done flash in the pan. And “adularia”? That specific mineral is a textbook fingerprint that tells geologists the fluids were boiling, which is precisely the moment gold drops out of solution and concentrates. Seeing adularia is like a chef seeing the water hit a rolling boil: it means the conditions were exactly right.

What they said: The footwall contains hydrothermal and possibly phreatic breccia with fluidal “streaming” textures, suggesting recurrent movement and explosive events related to deeper fluid boiling and potential gold deposition.

What it means: “Breccia” is rock that’s been shattered into fragments and re-cemented. “Phreatic breccia” with “fluidal, streaming textures” means there were underground steam explosions — violent, energetic events where pressurized, gold-rich fluids blasted through the rock. Why does that matter? Because those explosions happen above the boiling zone — and the boiling zone is the gold factory. In other words, the rock is telling the geologists: the engine that made this gold is sitting somewhere below where you’ve drilled. They’re seeing the smoke, and the fire is deeper.

What they said: Bladed calcite “lattice texture” has developed, and native gold has been observed in dendritic growths.

What it means: Two more confirmations. “Bladed calcite lattice texture” is one of the most reliable visual signals in the book that a system was boiling — geologists literally use it as a field flag for “drill here.” And “native gold observed” means they can see actual gold in the rock, not just gold detected by a lab assay. When you can see boiling textures in the hole, you’re standing in the sweet spot of an epithermal system.

So put it all together.

A wide, predictable, high-grade shoot that plunges down, in a system that filled with gold again and again…showing every textbook signal that the gold-forming engine is still sitting below where they’ve drilled so far.

The rocks themselves are pointing down and saying, “Keep going.”

That’s Mother Nature telling you there’s more – even after West Point Gold’s maiden resource comes out.

As we mentioned in the previous letter:

“…The corp-dev teams at the big gold producers such as Newmont, Kinross, Barrick and AngloGold are all hunting for the same checklist: 100,000 to 300,000 ounces a year of potential, first-quartile cash costs, a Tier-1 jurisdiction, and exploration upside. WPG already checks every one of those boxes.”

In short, if West Point Gold delivers on what management has been telegraphing – a resource of 2 million ounces at around 2 g/t, combined with a high-grade extension zone NOT in this resource – the major gold producers will have no choice but to take notice.

West Point Gold’s gold project is quickly becoming exactly what major gold producers look for: open at depth, high grades, and a low-sulphidation epithermal system in a tier-1 jurisdiction.

And there’s a strong chance hole GC26-148 isn’t a one-off.

There are seven more holes with assays still pending at this same depth at Northeast Tyro, part of roughly 6,550 metres of assays still to come.

As President & CEO Derek Macpherson put it: the high grades at NE Tyro continue to depth, the zone will remain open following the maiden resource, and deeper drilling is set to resume under a funded Fall 2026 to Spring 2027 program.

The Last Time Something Like This Happened

Now, you might be thinking: “That’s a nice hole, but how do I know this leads somewhere?”

Fair question.

So let me show you the blueprint because we’ve watched this exact movie before.

In the previous report on West Point Gold, I drew a line between West Point Gold and a company called Corvus Gold.

If you’ve followed this Letter for a while, you’ll remember it well.

Corvus’s North Bullfrog project sat on the same Walker Lane Trend. It hosted the same style of low-sulphidation epithermal gold — high-grade vein and stockwork zones, surrounded by lower-grade halos.

Sound familiar?

It should. It’s the exact deposit architecture West Point Gold is drilling at Tyro right now.

And here’s how the Corvus story ended.

In 2022, AngloGold Ashanti swooped in and bought Corvus for a total equity value of US$450 million.

That deal became the seed of what AngloGold now calls a Tier-1 gold district — a mine expected to pour an average of 105,000 ounces of gold a year over an 11-year life.

But here’s the kicker.

After buying Corvus, AngloGold’s geologists kept drilling that district and went on to define a deposit called Merlin, whose mineralization extends to extraordinary depth for an epithermal system.

And guess who the Exploration Manager at Corvus was through that AngloGold takeover?

A 40-year Walker Lane veteran named Mark Reischman.

And where is Mark Reischman today?

He came out of retirement as an advisor to work on West Point Gold’s deep-target thesis at Gold Chain.

He didn’t come back for an easy paycheck.

He came back because he’s seen this setup before, and he knows what’s at the bottom of it.

So when I tell you a hole that proves West Point’s high-grade keeps going at depth is a big deal, understand the context.

This is the same trend, the same deposit type, and the same lineage of people who turned Corvus into a US$450 million takeout — except this time, with gold trading at more than double the price it was when Corvus was bought.

Analysts Are Waking Up

Here’s how I know the market hasn’t caught up yet.

On June 14, 2026, Paradigm Capital initiated research coverage on West Point Gold.

Their rating? Speculative Buy.

Their 12-month target? C$3.30 per share.

The stock was trading around C$1.10 at the time.

That’s a potential return north of 200% to their target.

And this wasn’t just some back-of-the-napkin guess.

Paradigm spent six months working alongside an independent resource estimator and touring the project in person. And here’s what they concluded in that report:

There is already a real, economic deposit here, before the company has even published its first official resource.

Let me give you their numbers:

- Paradigm independently estimates that the two Tyro zones already host roughly 1.1 million ounces at 2.1 g/t — including the high-grade NE Tyro zone at about 0.6 million ounces at 3.5 g/t.

- They ran a conceptual mine model, and it throws off a 54% after-tax IRR and a net present value of roughly US$1.09 billion at $4,500 gold…

- …against a company that was carrying a market cap of only about US$107 million when they wrote it.

- Their net asset value works out to C$9.65 per share at $4,500 gold, meaning at C$1.10, the stock was trading at barely 0.11 times its own NAV.

Now connect that back to hole GC26-148.

Paradigm’s model specifically flags extension of NE Tyro at depth as a key catalyst. They estimate every additional 100 metres of NE Tyro extension is worth roughly 70,000 ounces — and that adding just 0.2 Moz to the high-grade zone alone would lift their NAV by about 20%.

GC26-148 is part of that extension – and it came back with even higher grades!

And they note that both Tyro zones are “open at depth,” which is exactly what the new hole just confirmed for NE Tyro.

So, Why Has the Stock Pulled Back?

Now, some of you are looking at the chart and asking the obvious question.

If this story is so good, why is the stock down from its highs?

It’s a fair question. And I’m going to give you a straight answer.

As most of our readers know, we share ideas based on a company’s long-term merits, not on short-term trading fluctuations.

Take our last antimony deal. We first featured it at C$0.50. We featured it again when it fell below C$0.36.

Last month, it hit a high of over C$3.

In other words, the climb wasn’t a straight line up. But we stuck to our guns based on the merits of the project — not on day-to-day trading.

We believe West Point Gold is in a similar situation.

Part of the recent weakness is simply tied to gold’s price. The whole sector pulled back in recent months as gold came off its highs, and the juniors always move more violently than the metal itself. That’s the nature of the beast.

But there’s a second factor you should understand, because it’s mechanical and has nothing to do with the quality of the rocks.

It’s the warrant and financing overhang.

According to WPG’s disclosure, the company has just over 20 million warrants outstanding, with an aggregate exercise value of roughly C$9.9 million — and a recent private placement that has now come free-trading, adding more stock to the float.

When a stock carries a meaningful pile of in-the-money warrants, it can act like a ceiling.

As the share price rises, warrant holders have an incentive to exercise and sell into strength. That selling pressure can suppress the share price, particularly as it runs into resistance. New shares hit the float as existing holders get diluted.

Anyone who has watched junior miners long enough has seen it play out.

And there’s timing involved, too: roughly 60% of those warrants expire in 2026. Holders facing an expiry have a forcing function: exercise or lose the option entirely. That can compress a wave of selling into a tighter window.

So yes, we believe that’s part of why the stock has been soft.

But here’s where it gets interesting.

Because that very same overhang that looks like a headwind on a quiet day can look completely different on a catalyst day.

Feature, Not a Bug

When WPG shares hit C$2.17 back in February 2026 on the back of strong drill results, that very same warrant structure was already in place.

The market cut straight through the overhang.

Why? Because the news was good enough.

When you’ve got a company on the cusp of a maiden resource, with a stack of pending assays and continued high-grade hits, catalyst flow can overwhelm supply pressure.

And WPG has a stack of catalysts coming.

Now consider what those warrants actually represent if they get exercised.

That C$9.9 million in exercise value? It’s essentially a pre-funded treasury.

If those warrants come in, that’s roughly C$10 million in cash flowing straight into West Point’s bank account — without a brokered financing, without a marketed deal, without dumping new shares at a discount to market.

For a junior explorer about to ramp drilling and march toward a maiden resource, ~C$10 million of capital is a big deal.

And here’s the final piece.

The strike prices themselves anchor a floor under the stock.

Warrant holders sitting on paper struck at C$0.30 to C$0.45 are likely not about to dump everything the moment the stock ticks higher. They’re already up three or four times their money — and were up even more when shares traded around C$2.

Many of these holders are insiders, family, friends, and supportive institutions who got in early.

In other words, they have skin in the longer-term story.

So while the overhang explains some of the recent softness, I’d argue it’s set up to flip into a tailwind the moment the catalysts hit.

A cheaper entry point, a built-in treasury, and a floor under the stock, all while heading into a maiden resource.

That, in my opinion, is an opportunity.

The District Bigger Picture

And Tyro is only part of the story.

Beyond the two Tyro zones, West Point Gold is already chasing gold at three more targets across the property:

- Black Dyke — a wide-open structural setting with historic mining and gold at surface.

- Sheep Trail — which returned 32.0 metres of 1.0 g/t gold in April, opening up a third potential resource area on the same property.

- Bull 8 — which returned 21.4 metres of 1.0 g/t gold in early June, on the first drilling ever along a 12-kilometre untested structural corridor.

And looming over all of it is the Frisco Graben — a large, covered target that West Point’s 2025 drilling already showed is sitting above a productive epithermal system.

The Frisco Graben is the target Mark Reischman identified on this property from day one.

It’s the reason he came out of retirement to advise West Point Gold.

Paradigm believes the planned 2026–2027 drill program could reveal property-wide potential of 2 million ounces or more.

In other words, the market right now is still pricing in the first zone.

It hasn’t even begun to think about the district.

Conclusion

So let’s put the whole picture together.

- Gold above $4,100, central banks buying at a record pace, and Washington calling domestic gold a matter of national security.

- A high-grade gold system on patented ground, with water rights, in a tier-1 mining jurisdiction.

- 66.2m of 6.57 g/t, including 20.7m at 18.25 g/t — that just proved the high-grade keeps going at depth, more than 250 metres down, still open.

- Seven more holes pending at that same depth.

- A maiden resource estimate coming later this year — the single event that flips a junior from “exploration story” to a number a major can put a price on.

- An independent analyst target of C$3.30 against a ~C$1.10 stock, with a modelled NAV of C$9.65.

- A blueprint — Corvus Gold — that played out 180 miles up the same trend and sold for US$450 million.

We’ve been doing this long enough to know that mathematical mispricing like this doesn’t last forever.

Especially not when the drill keeps hitting.

Show me another junior gold explorer with these consistent high-grade drill results in a low-sulphidation epithermal gold system in a tier 1 jurisdiction with water rights.

Anytime we’ve seen anything similar to 66.2m of 6.57 g/t drilled by a gold junior, their shares have exploded.

And more results are coming.

The maiden resource is coming.

The assays are still landing.

And the deeper they drill, the better this gets.

West Point Gold Corp.

Canadian Trading Symbol: WPG

US Trading Symbol: WPGCF

German Trading Symbol: LRA0

Seek the truth and be prepared,

Carlisle Kane

Important Disclosures & Disclaimer

This is a follow-up commentary and is provided for informational purposes only. It is not investment advice and is not a recommendation to buy or sell any security.

Equedia.com and Equedia Network Corporation are not registered as investment advisers, broker-dealers or other securities professionals with any financial or securities regulatory authority. Remember, past performance is not indicative of future performance. This article contains forward-looking statements that are subject to risks and uncertainties that could cause actual results to differ materially from the forward-looking statements made in this article. Just because many of the companies in our previous Equedia Reports have done well, doesn’t mean they all will. We are biased towards West Point Gold (WPG) because the Company is an advertiser on www.equedia.com. We currently own shares of WPG. You can do the math. Our reputation is built upon the companies we feature. That is why we invest in every company we feature in our Equedia Special Report Editions. It’s your money to invest and we don’t share in your profits or your losses, so please take responsibility for doing your own due diligence and consult your own professional advisers before investing in WPG or trading in WPG securities. Any opinions expressed in this article are our own. We’re not obligated to write a report on any of our advertisers, and we’re not obligated to talk about them just because they advertise with us. For a complete disclosure of the compensation received by us from WPG, please review our Terms of Service and full disclaimer at www.equedia.com/terms-of-use/.

As of the date of publication of this Newsletter, Equedia (on behalf of itself and any partner, director, officer or insider of Equedia) may have a financial or other interest in the parties featured in this Newsletter, within the meaning of National Instrument 31-103. Equedia and its directors own shares of West Point Gold (WPG) at the time of this writing. West Point Gold has engaged Equedia as part of a paid advertising engagement; all expenses for third-party site advertisements arranged for WPG have been paid for by WPG. All drill results, resource targets, and forward-looking statements referenced in this Newsletter are sourced from West Point Gold Corp. public disclosures, including press releases dated February 25, 2026, April 9, 2026, and April 22, 2026, and the Cormark Securities initiation report dated January 13, 2026. Gold price referenced as of April 26, 2026.

Additional Forward-Looking Statements

Certain statements contained in this presentation constitute forward-looking information. These statements relate to future events or future performance. Forward-looking statements include estimates and statements that describe WPG’s (the Company) future plans, objectives or goals, including words to the effect that the Company or management expects a stated condition or result to occur. The use of any of the words “could”, “intend”, “expect”, “believe”, “will”, “projected”, “estimated” and similar expressions and statements relating to matters that are not historical facts are intended to identify forward-looking information and are based on the Company’s current belief or assumptions as to the outcome and timing of such future events including, among others, assumptions about future prices of gold, silver, and other metal prices, currency exchange rates and interest rates, favourable operating conditions, political stability, obtaining government approvals and financing on time, obtaining renewals for existing licenses and permits and obtaining required licenses and permits, labour stability, stability in market conditions, availability of equipment, availability of drill rigs, and anticipated costs and expenditures.

The Company and Equedia cautions that all forward-looking statements are inherently uncertain, and that actual performance may be affected by a number of material factors, many of which are beyond the Company’s control. Such factors include, among other things: risks and uncertainties relating to West Point Gold’s ability to complete all payments and expenditures required under the Company’s Option Agreement with Kinross; and other risks and uncertainties relating to the actual results of current exploration activities, the uncertainty of reserve and resources estimates; the uncertainty of estimates and projections in relation to production, costs and expenses; risks relating to grade and continuity of mineral deposits; the uncertainties involved in interpreting drill results and other exploration data, the uncertainties respecting resource estimates, the potential for delays in exploration or development activities, the geology, grade and continuity of mineral deposits, the possibility that future exploration, development or mining results, statements about expected results and future dividends may not be consistent with the Company’s expectations due to accidents, equipment breakdowns, title and permitting matters, labour disputes or other unanticipated difficulties with or interruptions in operations, fluctuating metal prices, unanticipated costs and expenses, uncertainties relating to the availability and costs of financing needed in the future and regulatory restrictions, including environmental regulatory restrictions.

The possibility that future exploration, development or mining results will not be consistent with adjacent properties and the Company’s expectations; operational risks and hazards inherent with the business of mining (including environmental accidents and hazards, industrial accidents, equipment breakdown, unusual or unexpected geological or structural formations, cave-ins, flooding and severe weather); metal price fluctuations; environmental and regulatory requirements; availability of permits, failure to convert estimated mineral resources to reserves, the inability to complete a feasibility study which recommends a production decision, the preliminary nature of metallurgical test results, fluctuating gold prices, possibility of equipment breakdowns and delays, exploration cost overruns, availability of capital and financing, general economic, political risks, market or business conditions, regulatory changes, timeliness of government or regulatory approvals and other risks involved in the mineral exploration and development industry, and those risks set out in the filings on SEDAR made by the Company with securities regulators.

Although the Company believes that the assumptions and factors used in preparing the forward-looking information in this corporate presentation are reasonable, undue reliance should not be placed on such information, which only applies as of the date of this Press release, and no assurance can be given that such events will occur in the disclosed time frames or at all. The Company expressly disclaims any intention or obligation to update or revise any forward-looking statements whether as a result of new information, future events or otherwise, other than as required by applicable securities legislation.

All drill results, technical details, resource timing, and company-specific figures referenced above are sourced directly from West Point Gold Corp.’s public disclosures — principally the press release announcing hole GC26-148 at the NE Tyro Zone, and the June 9, 2026 release confirming completion of the 21,079-metre drill program. Central bank figures (record 45% planning to add gold, 89% expecting global official holdings to rise, no respondents planning to sell, and gold surpassing U.S. Treasuries as the largest reserve asset) are from the World Gold Council’s 2026 Central Bank Gold Reserves Survey, published June 16, 2026. Gold price levels are as of mid-June 2026 (~$4,150/oz) per public market data and had pulled back from the late-January 2026 record of approximately $5,600/oz. The JPMorgan ~$6,300 and ~$7,000 analyst gold-price calls are as referenced in the original April 2026 Equedia letter and prevailing market commentary.

Analyst figures — the C$3.30 target, Speculative Buy rating, ~1.1 Moz @ 2.1 g/t in-situ estimate, ~0.6 Moz @ 3.5 g/t NE Tyro estimate, 54% after-tax IRR, ~US$1.09 billion NPV at $4,500 gold, C$9.65/share NAV, ~0.11x P/NAV, cash and warrant figures, and the per-100m NE Tyro extension sensitivity — are drawn from Paradigm Capital Inc.’s initiation report on West Point Gold dated June 14, 2026. Paradigm rates the stock Speculative Buy and discloses that it has provided financial advice to and/or expects to seek investment-banking compensation from West Point Gold; its estimates are conceptual and its target reflects assumptions including resource growth toward ~2 Moz, a higher gold price, and multiple expansion. Warrant figures (just under 20 million warrants outstanding, ~C$9.9 million aggregate exercise value, roughly 60% expiring in 2026, strike prices ~C$0.30–C$0.45) are sourced from West Point Gold’s public disclosure; a recent private placement has become free-trading. The historical C$2.17 February 2026 share-price high and the ~C$1.10 recent level are per public market data; the antimony comparison references a prior Equedia-featured idea. Corvus Gold / North Bullfrog acquisition figures (~US$450 million equity value) and North Bullfrog production estimates (avg. 105,000 oz/yr, ~11-year life) are sourced from AngloGold Ashanti and third-party disclosures.

Mineral resources that are not mineral reserves do not have demonstrated economic viability. A maiden resource estimate has not yet been published; exploration targets and grades are conceptual. There is no certainty that any portion of the mineralization discussed will be defined as a resource, upgraded to a reserve, or ever economically mined. Forward-looking statements are inherently uncertain and actual results may differ materially. Past performance and prior takeovers (Corvus Gold and others) are not indicative of future results for West Point Gold. Consult a licensed financial professional before investing.