The Highest Growth Silver Producer: Aurcana Corporation

Over the past six months, I have held off on many investments due to the nature of the Canadian markets.

But given the recent sell-off and what appears to be a potentially strong rebound, I feel now is a great time to be investing in strong silver production plays with massive growth potential; both in production growth and exploration upside.

I want to introduce you to:

One of the Highest Growth Silver Production Companies in the World

But before I do that, let me explain a few important things.

Silver is undeniably a strong performing precious metal. While volatile, it offers an incredible risk/return reward when compared to gold. That’s why I have been stocking up on physical silver myself in the past months.

Here’s my latest batch that arrived just the other day…it only took 8 weeks to get it. That’s because smart individuals and investors hoarding the shiny metal are draining the physical supplies of silver.

No More Silver?

A few weeks back, I talked about how the demand for physical silver coins at the U.S. mint hit a new all-time high during the month of February.

In just 6 business days in April, the U.S. mint had already sold 1,712,000 ounces of Silver Eagle coins, bringing the 2013 total to a whopping 15,935,000 ounces of coins. This doesn’t include any sales of bars or wafers.

Despite rising demand, prices fell.

As a result, the paper supply of both gold and silver are now being brought into question as physical demand heats up and investors are asking for physical delivery.

The only problem?

What? You Don’t Have My Gold?

The banks and those who claim to back up their paper gold with true physical inventories are defaulting on their redemptions.

Rumours of the LBMA (world’s largest gold trading house) not willing to deliver gold, and news of JP Morgan’s inventories at the COMEX having gone from 2.4 million (ounces) down to 160,000 ounces (see staggering bank outflow,) are beginning to surface everywhere.

One of the largest European banks, ABN Amro, recently defaulted on their gold contracts and informed their clients that they would only settle their gold bullion contracts in cash and not in physical.

I’ve also talked about silver manipulation by the big banks many times before.

Never before has their been such a rush to buy and redeem physical bullion. Even countries around the world are doing it, including Germany and Venezuela.

It’s only a matter of time before the paper contracts catch up to physical demand.

The Best Time to Buy

The best time to buy stocks is when no one else wants them, but fundamentals remain astoundingly strong. That couldn’t be truer for the silver space.

While silver can be volatile, strong silver producers generally operate at far better margins than the majority of the gold producers. This allows them to remain operational and cash flow positive, even if silver prices fall.

But with so many silver producers already trading at near 52-week lows, which one makes the most sense?

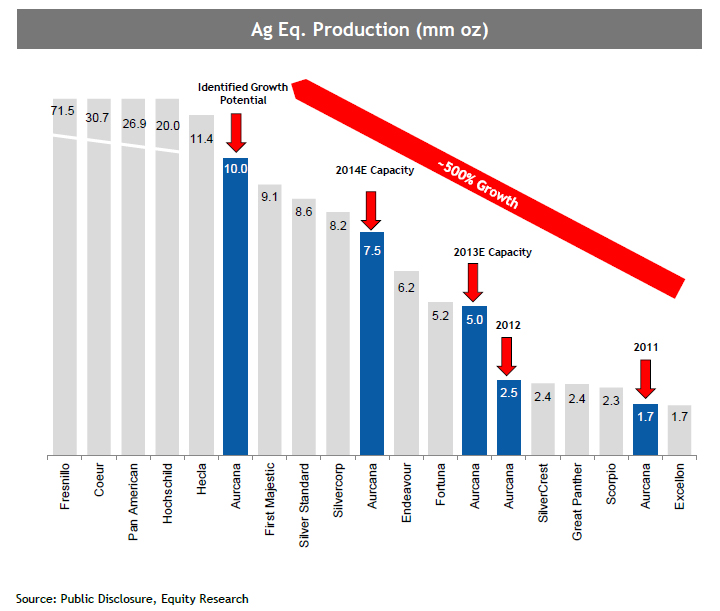

Highest Production Growth Potential

The company I am about to introduce owns and operates two mines, one of which will soon become one of the largest pure silver mines in the U.S. and one of the largest primary silver mines in North America.

It’s also sitting on at least *$4 billion worth of silver, with potential to uncover a lot more.

*Based on NI43-101 resources and current silver spot price

Its no wonder RBC Capital Markets says this Company:

…offers the highest projected production growth amongst the silver companies within our coverage universe.

A Dramatic Increase in Resource

Just last year, the Company announced a 50-fold increase in resource at just one of its mines.

Legendary silver geologist, Dr. Peter Megaw, believes that this company is not only sitting on two potentially really large deposits, but if they are tracked properly through exploration could have potential to be monsters.

And recent discoveries are starting to show that Dr. Megaw could be right.

More on this in a bit.

Not Just Another Junior

This Company isn’t just some junior explorer sitting on top of a deposit waiting for permits, or a junior explorer hoping to hit the big hole; this is an up-and-coming silver producer that is expected to undergo significant production and cash flow growth over the next few years, catapulting it from junior producer to senior status.

The Company is pulling silver out of the ground so fast that if its identified growth potential is met, it would join the ranks of companies like First Majestic, who currently has a market cap of $1.38 billion.

As of today, the Company only has a market cap of just over $200 million.

Current silver production is expected to more than triple and the Company is expected to undergo significant cash flow growth over the next few years.

Best of all, with the recent market dip, the Company is now trading near its 52-week low – yet, it continues to grow and churn our more cash than it ever has before.

With much of the hard work and capital intensive proceduressalready completed, the company is now in a position to grow organically with just their budgeted sustaining capital.

Analysts are already telling us that this Company is:

Building the next significant silver platform.

Silver Company Success

I can boldly say that EVERY silver company that the Equedia Letter has ever covered has shown great opportunities for major gains.

That is why I am excited about my next silver investment.

If you’re looking for the next silver play with incredible production growth potential and massive exploration upside, you’ve found it with:

Aurcana Corporation

(TSX.V: AUN)

(OTCQX: AUNFF)

Aurcana Corporation (Aurcana) is an up-and-coming silver producer that is expected to undergo significant production and cash flow growth over the next few years.

It owns two operating silver mines: the 100%-owned Shafter silver mine in Texas and the 99.9%-owned La Negra silver-copper-lead-zinc mine in Mexico.

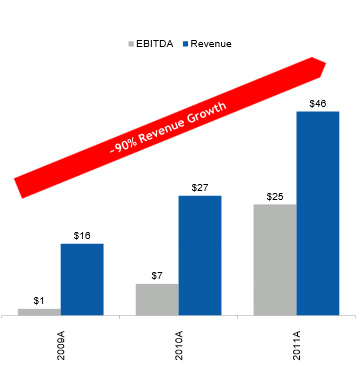

Last year, Aurcana produced over 2.5 million silver equivalent ounces, with revenues of nearly US$56.9MM, with a total cash cost per silver ounce net of by-products of US$6.43.

As the Company ramps up production, those numbers are expected to increase dramatically.

Production Expansion and Anticipated Growth

Aurcana recently reached new capacity at La Negra, churning 3,000 tons per day (tpd). It wasn’t doing that last year, which means it will produce more silver than it ever has before, at a lower cash cost.

At the Shafter mine, Aurcana is ramping up in hopes to reach steady-state levels by the end of this year, or early 2014.

Production at Shafter is expected to quadruple by 2015, with annual silver production forecast to increase from 1.5mmoz in 2013 to 6MMoz in 2015.

That means Aurcana is on the verge of becoming a senior silver producer, producing in excess of 5 million ounces per year.

But that’s just the tipping point.

If Aurcana can reach their production potential at Shafter of 2,500 tpd, they could be producing in excess of 10MM ounces of silver annually; thus, surpassing many strong senior producers.

The growth path for Aurcana is remarkable. Their goal is to become a 10MM oz. per year producer within the next few years. If their track record is any indication of their future, I believe they can achieve their goal.

Take a look:

CEO Lenic Rodriguez has taken Aurcana from a small suffering silver producer when times were tough, to a producer that is on the verge of becoming a senior producer.

But their growth is just beginning.

Let me explain.

La Negra – A Record Breaking Year

La Negra is a 99.9%-owned polymetallic carbonate replacement deposit (CRD), consisting mainly of a manto (horizontal) and chimney (vertical) skarn deposits.

It was originally brought into production in the early 1970’s and has over 60 km of underground workings spread over five levels.

The project consists of 28 individual deposits, only three of which contain formally defined NI43-101 resources.

Aurcana has done a phenomenal job of improving the operational performance and economics of the project. Through a number of low-cost expansions, the La Negra Mill is now operating at 3,000 tpd.

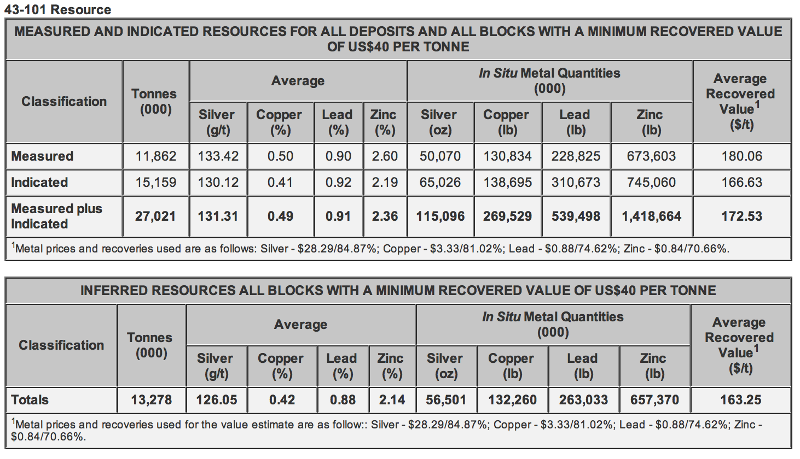

Resource: How Much Potential Does it Have?

Last year, Aurcana reported a 50-fold increase in NI43-101 compliant measured and indicated resource estimate La Negra.

It identified 115 million ounces of measured and indicated silver underground, which should change the mine life to at least 20 years, assuming a daily capacity of 3,000 tonnes.

Notes:

-

Ounces and pounds of in situ metal are calculated using only resource blocks with a recovered value of US$40 or greater.

-

Metal prices and recoveries used for the average recovered value estimate are calculated using a trailing 12-quarter average spot price and actual recoveries as documented in the company’s NSR reports from January through May 2012.as follows: Silver – $28.29/84.87%; Copper – $3.33/81.02%; Lead – $0.88/74.62%; Zinc – $0.84/70.66%.

-

Mineral Resources are not Mineral Reserves and do not have demonstrated economic viability. There is no certainty that all or any part of the estimated Mineral Resources will be converted into Mineral Reserves. The estimate of Mineral Resources may be materially affected by environmental, permitting, legal, title, taxation, sociopolitical, marketing, or other relevant issues

-

The Mineral Resource was estimated in accordance with the Canadian Institute of Mining, Metallurgy and Petroleum (“CIM”), CIM Standards on Mineral Resources and Reserves, Definitions and Guidelines prepared by the Standards Committee on Reserve Definitions and adopted by the CIM Council on November 27, 2010

In addition to silver, La Negra could produce on average 5 million pounds of copper, 10 million pounds of lead and 21 million pounds of zinc. From a silver equivalent standpoint, it could be producing an average of 3.7 million ounces every year.

Apart from the implied substantial increase in the project’s life of mine, the new mineral resource estimate could point to better project economics going forward as the M&I tonnage grades have increased from to 123.6 g/t Ag from the previous resource estimate to 131.6 g/t Ag.

If the Company continues to increase their resource, production could increase beyond its expected range with lower cash costs.

Given recent discoveries, there are strong signs the Company could increase their resource dramatically…

A Significant Discovery the Market Doesn’t Know

On Feb 11, 2013, Aurcana announced new discoveries at La Negra that indicate the presence of gold.

Take a look:

Zona Aurifera I, returned strong assay values including:

- 15.3 gm/t Au and 261 gm/t Ag;

- 12 gm/t Au and 105 gm/t Ag;

- 10.0 gm/t Au and 381 gm/t Ag;

Zona Aurifera II also returned strong assay values including:

- 2.8 gm/t Au and 229 gm/t Ag;

- 2.4 gm/t Au and 307 gm/t Ag;

- 2.8 gm/t Au and 95 gm/t Ag;

These numbers are good, but I don’t think the market understands just how significant these numbers may be.

Let me explain.

The Head of the Octopus

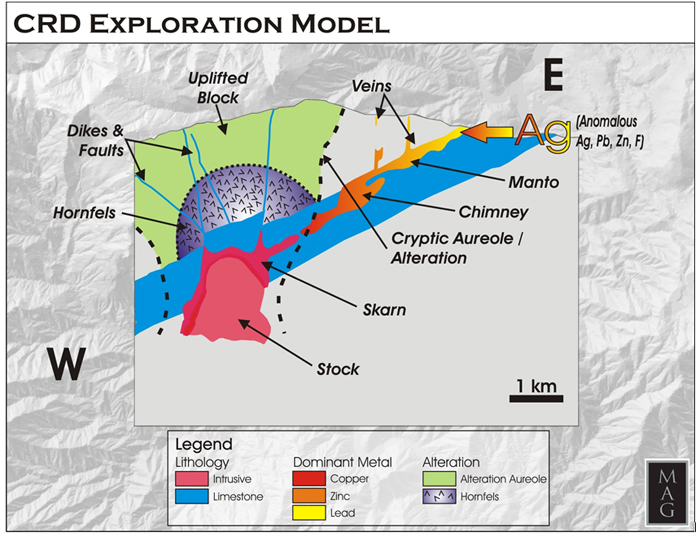

La Negra is a Carbonate Replacement Deposit.

Those of you who have been a long time reader of the Equedia Letter will know exactly what this type of deposit is and why Aurcana’s recent gold grades could mean something special.

For those who are new, the following is a refresher.

Carbonate Replacement Deposit (CRD) Explained

CRD’s represent approximately 40% of Mexico’s 10-billion ounce historic silver production and have been mined for more than 400 years. They are characterized by massive to semi-massive silver-lead-zinc sulphide intrusions.

The attractive characteristics of CRDs are simple: They have potential for large tonnage and high grades; potential for substantial base metal credits to the precious metal resource; and, sulphide replacement in carbonates (limestone) mitigates oxidation, and is therefore more metallurgically amenable and environmentally benign. In other words they’re cheap to mine and have a minimal environmental footprint.

|

|

Courtesy: MAG Silver

|

As you can see from the above, CRD’s have many different parts. As Dr. Peter Megaw explained, think of a CRD like an octopus. The Stock and Skarn are the body of the octopus and the manto are the tentacles.

The biggest CRD, Santo Eulalia, has produced over 50 million tonnes, has six parallel mantos of comparable size and each manto had about 8 million tonnes – and that’s before you get into the big chimneys that are 700 metres high and 100 metres in diameter. La Negra already has a resource of more than 40 million tonnes*.

*as represented by their NI43-101 M&I and inferred resource

Here’s where it gets interesting.

La Negra – Gold Intercepts Explained

The market doesn’t understand the significance of the February drill results because it doesn’t understand CRD systems. If it did, it would see the massive potential that I do.

Let me explain it in simple terms.

While the manto and skarn of a CRD deposit can be massive in size, the big volume of mineralization occurs in the stock, the head of the octopus, if you will.

As you get deeper into the system, the silver and lead grades drop off but everything else rises, and that’s a typical geological sign that you’re getting closer to the source of a CRD system.

Now the grades of silver and lead may drop off as you get closer to the source, and even in some respect the grade for zinc is dropped off, but the volume of mineralization goes up by an order of magnitude.

How Does that Relate to La Negra?

Gold tends to show up in two places; it shows up way in the fringe of the district and then again in the guts. So as you get down to where La Negra is finding gold, its in a nearer source environment; a more proximal environment.

In other words, as you get closer to the source your silver grades go down, your leads grades go down, your zinc, copper, and gold all come up. And the reverse is true as you go farther away from the source with gold disappearing fairly quickly, and copper goes away after a while. Zinc persists all the way to the end, with lead and silver generally the strongest in the most distal parts of the system.

So all the metals are present at some level from one end all the way to the other.

It’s just the relative proportion that’s changed.

A Legendary Expert

I wanted to make sure I was putting the right pieces of the puzzle together. To prove my theory, I needed to speak with someone who knows these CRD systems well.

And there is no one in the world that knows more about Mexican CRDs, than the pioneer of CRD research, Dr. Peter Kenneth McNeill Megaw.

He was awarded the Robert M. Dreyer Award last year in recognition of his applications of the science of geology to the

discovery of Carbonate Replacement Deposits (CRD) and Epithermal Silver-Gold Vein Deposits (EVD) in Mexico, for his study and understanding of how CRD and EVD deposits fit into the geologic evolution of Mexico, and mostly for his discoveries: the Juanicipio-Valdecañas epithermal veins in the western Fresnillo District, Zacatecas and the Platosa, Durango and Pozo-Seco/Cinco de Mayo, and Chihuahua CRD deposits.Dr. Megaw is the world’s foremost expert on CRDs and has played a pivotal role in Mexican mining over the last 30 years.

(Of course, Aurcana knows Dr. Megaw is the man when it comes to CRDs and as such, has hired him to lead the exploration work at both Shafter and La Negra. This gives me comfort in knowing the exploration program will be done right.)

Dr. Megaw’s interpretation of what we’re seeing at La Negra — the higher gold and copper values, lower silver and high zinc — is that they’re in a more near source or more proximal environment.

In plain English, the recent gold intercepts could mean Aurcana may be onto a source. As you just learned, finding the source should mean the volume of mineralization could go up by an order of magnitude.

If that is the case, and all known signs say it is, then their resource could skyrocket based on what we know of these systems.

With Dr. Megaw’s help, Aurcana is now aggressively following up the recent discoveries of significant gold associated with strong silver, zinc and lead mineralization in the new areas tested at La Negra, with a 5,000 meters drill program already underway.

But again, that’s not all.

Not Even Close

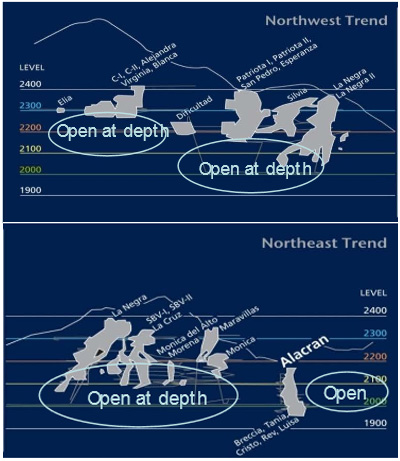

La Negra is a much more substantial system than anybody knew until about the last five years.

First of all, La Negra still remains open in multiple directions, and at depth. According to Dr. Megaw, It could go way below the current operating levels and still not be anything that you could consider a deep mine below the surface.

Using the Octopus analogy, La Negra is more like an octopus that’s swimming vertically; so the head is down and Aurcana’s grabbed a couple of tentacles. So what you do is follow these tentacles down into the guts of the system to where it all comes together.

Aurcana hasn’t even come close to doing enough exploration work at La Negra.

Dr. Megaw also believes that there may be multiple mineralization centres in La Negra’s district.

Multiple Mineralization Centres?

These systems are all related to bodies of highly evolved intrusive rock, magma, called cupulas. Basically, you start with a large body of magma and then it differentiates and makes a smaller body of more concentrated composition.

And sometimes you have several of those that come up to the same area. Each one may have mineralization associated with it. So the zoning that you expect to see on an ore body in a district scale will be repeated with respect to each of those intrusive centres.

In Dr. Megaw’s analogy, La Negra has multiple octopi. He expects to see the same style of mineralization repeated with respect to a bunch of different sources.

Thus far, the company knows of 28 individual deposits, only three of which contain formally defined NI43-101 resources. Large system of underground levels and workings provides access to carry out additional exploration on surface identified targets.

La Negra is a massive CRD system. And the bigger the deposit, the more they behave like the typical CRD model. That means all signs point to massive exploration upside potential.

But La Negra isn’t the only massive discovery…

Shafter is one too.

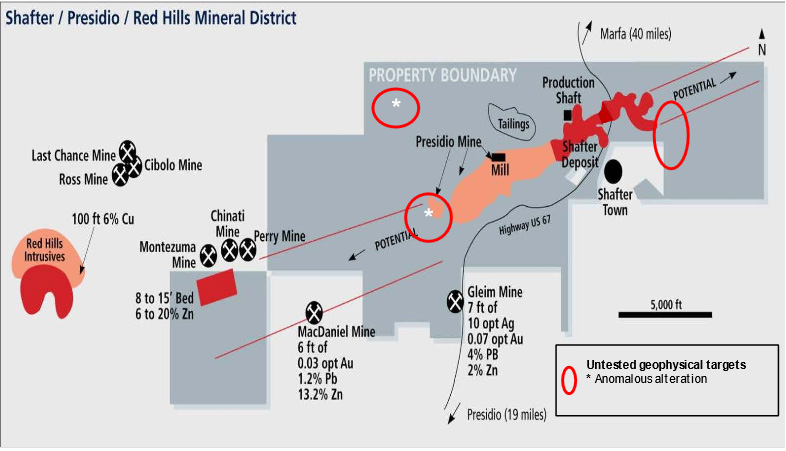

Shafter, Texas: The Next Major Silver Mine in U.S.

…We believe that at current share prices investors are buying La Negra at a good price and getting the potential upside from Shafter for free.

– Stonecap Securities, April 15, 2013

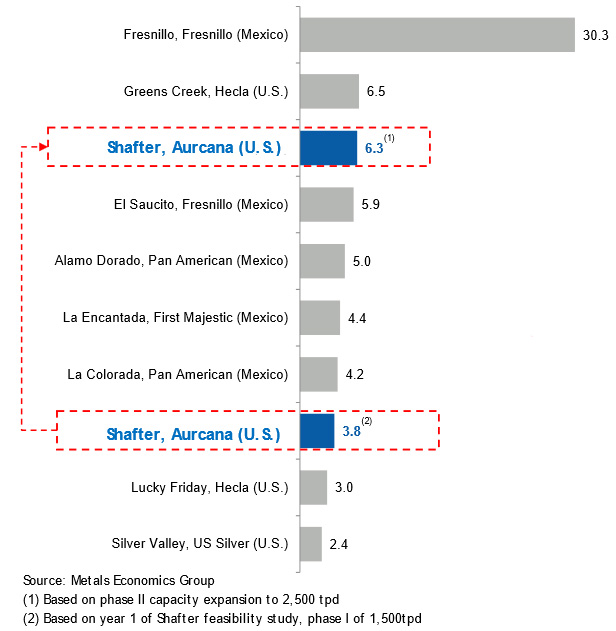

Located near the United States/Mexico border, Shafter is an oxidized CRD and predominantly an underground silver mine that at its peak will become one of the largest primary silver producers in the U.S.

It will not only be the 2nd largest producing pure silver mine in the U.S., second only to Hecla’s Greens Creek project in Alaska, but will supply 10% of all U.S. silver.

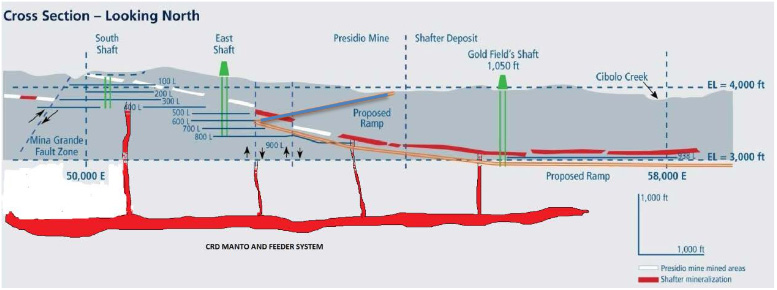

It lies within the northern limits of the Sierra Madre Occidental belt, one of the more prolific mineralized belts within Central America. It is the down-dip extension of the Presidio mine that was mined until 1942 when operations were suspended due to the War Act. During that time, it produced 2.3 million tonnes of ore containing 35.2 million ounces of silver with an average grade of 15.42oz/tonne.

Although located in Texas, Shafter seems to be a perfectly well behaved CRD. As Dr. Megaw had put it, Shafter doesn’t know its not in Mexico.

Shafter Resources

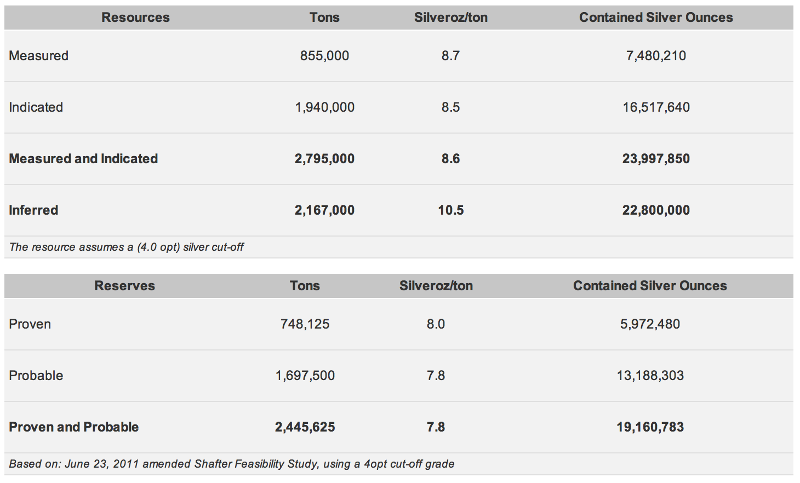

Shafter currently has a NI 43-101 silver resource of 24.6 million ounces Measured and Indicated (2,900,000 tons @ 8.48 opt), 22.8 million ounces Inferred (2,167,000 @ 10.52 opt) and a pre-feasibility completed.

There is also significant potential to expand mine life through conversion and expansion of mineral resource. The resource remains open along strike, and potentially, at depth.

Shafter Mining Operations

Management is currently in the process of ramping up Phase I production from its current 5,00 tpd to 1,500 tpd, with an estimated cash cost of around $10/oz.

The ramp up process, however, does have certain risks and delays and Shafter is no exception.

While the mine development has been progressing, the Shafter mill has experienced a few unanticipated technical issues with some pieces of equipment in the mill and processing plant that have slowed down the ramp up efforts.

As a result, the Shafter mill has not yet reached its initial target of 600 tpd on a continuous basis.

While the mill is operating and producing silver, the progress is dependent on the delivery times for additional pieces of equipment that are required to streamline the operations.

In order to achieve full production capacity during 2013, a number of improvements to the original plant design are necessary.

These improvements and delays, however, have been identified. That means management knows what the problems are and how to solve them.

An action plan developed by using outside consultants as well as in-house expertise has been finalized and set in motion to gradually move to full production.

For example:

- Additional filter presses have been ordered and are scheduled for delivery during Q2 2013 and to become operational during Q3 2013.

- The installation of a CCD circuit that will result in an increase of the overall recovery rate is underway and will be completed gradually during 2013.

- In order to meet the planned level of production, the addition of a second drying oven and a new furnace in the refinery is currently being designed and will be completed during Q3 2013.

- Construction has been completed on the foundations and steel work of one additional thickener with a second one in progress. These tanks are being built as part of the project to achieve planned capacity.

- Staff hiring and training is continuing to strengthen the production team at Shafter. Additional people are being trained and will be added with the gradual increase in production to 1,500 tpd.

After speaking with management regarding Shafter’s ramp-up phase, I think they will take just a little longer than anticipated to reach a throughput of 1,500 tons/day; my estimate is probably by the end of the year or Q1 of 2014.

However, I expect some of the required equipment to arrive by Q3, which is less than a couple of months away. At which point, Aurcana could be producing 900 tpd by the end of Q3 and on its way to the 1,200 – 1,500 tpd by the end of Q4 or early 2014. This should increase cash flow and add to a better bottom line in the upcoming quarterly statements.

While the market may penalize Aurcana slightly for the delays, it may not necessarily be justified to the extent the market has shown. Many of the problems were not only identified immediately but action plans are well underway to solve the issues.

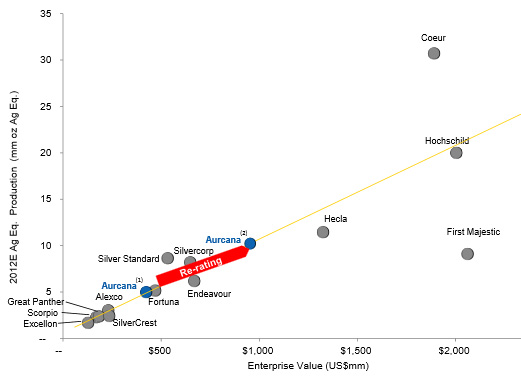

If Aurcana can ramp Shafter up to the 1,500 tpd capacity, we should see a strong rerating to the upside of the Company’s share price.

Operation Upside

According to management, the current designed capacity of the mill is 2,500 tpd which means production could be much higher than currently expected numbers.

Permitting is already in place to run at a higher throughput.

Once managements completes Phase I, they will begin Phase II to support 2,500 tpd, with expected annual production in excess of over 6 million ounces. That’s excluding the lower grade open-pit material.

Should resource growth and underground operations support the higher run rate, it would lead to yet another opportunity to rerate Aurcana shares.

The anticipated Peak production of 3.8 million ounces in 2014/15 will transform Shafter into one of the largest primary silver mines in US.

Exploration Upside at Shafter

Dr. Megaw is also leading the exploration efforts at Shafter in attempts to track the deposit to more mantos, and ultimately, the source of the CRD.

The Shafter deposit itself, as well as the surrounding areas, are vastly under-explored and represent a large opportunity for growth by expanding into a full mining district.

Aurcana controls a significant land package surrounding Shafter, which has been home to a handful of other historical mining operations. There is certainly opportunity to add resources to Shafter as the company explores along trend.

Recent discoveries at Shafter have identified new evidence to support the massive potential:

Dr. Peter Megaw, consulting geologist for Aurcana Corporation states:

Having evidence of complex, multiple stages at Shafter confirms we are exploring in a system with high potential, while demonstrating that although we still have not zeroed in on where to focus, continuing to do so is more than warranted. Seeing high complexity is a positive indicator for a long-lived, multi-staged, large system.

The Characteristics of Shafter

Aurcana is currently mining the manto at Shafter. As part of the CRD model, it appears that they are currently mining at the distal part of the system.

The known historic combination of the Presidio and Shafter ore bodies is just under two miles long, or just over two and a half kilometres. These systems can commonly be as much as seven or eight kilometres from one end to the other – especially horizontally or laterally developed systems like Shafter (whereas La Negra is vertically-oriented.) Shafter has all the signs of being fed from one end and working outward from the other.

As current Shafter resource appears to be in the distal part of the system and already in the four million plus tonne range, in terms of historic production and current resources, there’s no doubt that Shafter is proving itself to be a very big system.

And they’ve only found a piece of it.

Using Dr. Megaw’s analogy, “management has the elephant by the trunk and has the rest of the body to look for.”

That means Shafter has potential to be much, much bigger.

Exploration Highlights at Shafter

- Potential to encounter additional mineralized mantos in favourable limestone beds at depth

- Similar Mexican CRD deposits support the existence of stacked mineralized mantos

- Current exploration focused on locating potential “feeder” system that formed the Shafter deposits

- Existing resource open along strike to the east

- Historic drilling stopped before end of mineralization

- Historic geophysical anomalies remain untested in east and west sectors

- Numerous past-producing mines and prospects in the area

- Anomalous silica/oxide concentrations NW of Shafter deposit

- Possible evidence of buried mineralization

Shareholder Dilution

Most of the capital intensive work bringing both La Negra and Shafter into production has already been done and paid for.

Both of Aurcana’s projects are operating and generating cash flow; thus, the Company’s strategic development can be largely self-funded, thereby reducing dilution risk that other developing resource companies typically face when building expanding production.

However, if Shafter runs into more capital intensive problems during its ramp up, it has arranged a US$15 million non-dilutive credit facility with its concentrate buyer from the La Negra Mine, to be reimbursed by Q4 2013.

Aurcana should have more than enough money to bring Shafter to steady-state and transform the Company into a senior producer.

Risks

There are always risks and it wouldn’t make sense not to point them out:

- Silver Prices: Aurcana’s bottom line, beyond variations in operating and capital expenditure, is sensitive to changes in the prices of silver, copper and zinc. Of these, silver is the greatest contributor to the company’s revenues. While commodity price performances represent risk, the company’s low operating costs should help leverage its ability to maintain cash flow at lower silver prices.

- Execution: Any delays in the project execution/ramp up at the large-scale Shafter mine could have an impact on valuation. However, I would say that the market has already penalized Aurcana for the slower start-up at Shafter. Furthermore, management already has in place an action plan that’s underway to solve their ramp-up issues. Once Aurcana can demonstrate that it can sustain a daily throughput of 1,500 tons, it will alleviate many near-term concerns.

- Project Economics: Aurcana is currently using historic data at Shafter and more recent sampling to establish the life of mine grades. That means the data could materially differ from the actual operational parameters. However, given what we know of these CRD systems, the potential for further exploration upside with Dr. Megaw’s help warrants an increase in resource. Also, La Negra grades should improve thanks to access to the higher-quality material.

Tracking the Monsters: Shafter and La Negra

The massive upside exploration success at Aurcana will be determined by management’s ability to track the CRDs from the tip of the system right into the guts.

With the help of Dr. Megaw, Aurcana stands a great chance of dramatically increasing their resources at both Shafter and La Negra.

Major deposits, such as Penasquito, the Naica Mine, San Martín-Sabinas, and even the monster at Cinco de Mayo, have been all found using the same techniques currently being deployed by Aurcana and led by Dr. Megaw.

These massive CRD systems are all being found primarily in Mexico. While these CRD systems exist elsewhere, they’re not as well developed outside of Mexico. These deposits get as big as they ever get worldwide, which is well over a hundred million tonnes, in Mexico.

Both Shafter and La Negra are big systems that I believe will continue to get bigger.

There will be others that say Aurcana should look at targeting other juniors with its cash flow once Shafter runs at steady state, but I say the potential is right there in their own backyard.

The point is that many of the major CRDs that have produced, and will continue to produce millions of ounces of silver, were tracked from something like Shafter through something like La Negra and into the source. Many of these already massive CRDs currently being mined will continue to get even bigger.

While Aurcana already has a great resources at both Shafter and La Negra, and its production growth potential is larger than anybody in the space, they still have yet to hit the jackpot.

Is there a possibility that both Shafter and La Negra can become extremely large systems capable of becoming some of the largest known CRDs in the world? Yes.

What will it mean for shareholders if they do?

It’s a Small World

Silver is an asset whose consumption will exceed new production for many years. With just $50 billion of silver bullion above ground, the silver market is a very small market that gets crowded very easily.

The amount of silver stocks with strong assets is extremely limited and very few discoveries are being made worldwide.

It pays to be the highest growth potential silver producer with massive upside exploration potential.

And who doesn’t want to get paid?

Until next time,

Ivan Lo

The Equedia Letter

We’re biased towards Aurcana Corporation because they are an advertiser, we will be buying shares, and we own options. You can do the math. Our reputation is built upon the companies we feature. That is why we invest in every company we feature in our Equedia Reports, including Aurcana Corporation. It’s your money to invest and we don’t share in your profits or your losses, so please take responsibility for doing your own due diligence. Remember, past performance is not indicative of future performance. Just because many of the companies in our previous Equedia Reports have done well, doesn’t mean they all will. Furthermore, Aurcana Corporation and its management have no control over our editorial content and any opinions expressed are those of our own. We’re not obligated to write a report on any of our advertisers and we’re not obligated to talk about them just because they advertise with us.

Aurcana Corporation Highlights

- High-Quality Assets in Favourable Mining Jurisdictions

- Emerging Senior Silver Producer with Leading Growth Profile

- Significant Production Upside Potential

- Attractive Relative Valuation and Re-Rating Potential

- Experienced Management Team with Track Record of Value Creation

Salvador Huerta, Chief Financial Office

With training at Harvard Business School, Mr. Huerta has over 30 years work experience as a CFO for large multinational Companies, such as: H.J. Heinz; Timex Corp; Rheem Manufacturing and other global Mexico based Groups. Mr. Huerta has extensive knowledge and experience in business, finances, manufacturing, planning, treasury and accounting, as well as international joint ventures, mergers and acquisitions. Prior to joining Aurcana, he acted as an investment opportunities advisor for Nichimen Japanese Co, now Sojits Corporation a large multinational corporation with 483 subsidiaries all over the world.

Dr. Sadek El Alfy, Vice President Operations

Dr. Sadek El-Alfy is a professional mining Engineer with 35 years of experience in underground as well as open pit mining on various continents. Recently he was responsible for mining operations in Venezuela and Uruguay for Crystallex International Corporation over a period of 12 years. In the past few years, he was also responsible for the completion of Feasibility Studies and Environmental Impact Studies for major mining projects in several South American countries as well as Mexico. Prior to his involvement in South American operations, Dr. El-Alfy was in charge of mining and concentrating operations at several locations in Canada including General Manager of the Iron Ore Company of Canada.

Nils von Fersen PGeo, Vice President, Exploration

Nils von Fersen is a Professional Geologist with over 30 years of expertise in conducting and managing mineral exploration for base and precious metals in Canada, Chile, Mexico and Guatemala for major and junior mining companies. Mr. von Fersen spent 18 years with Kidd Creek Mines and Falconbridge in exploration and project evaluation in western Canada and internationally, including the exploration and feasibility phases of the world class Collahuasi porphyry copper deposit in Chile. Since 1999 Mr. von Fersen has been a consulting geologist with a focus on projects in B.C., Mexico and Central America.

Alfonso Canseco Hernández, Director of Operations and General Manager, La Negra Mine

Mr. Canseco has more than 38 years of experience in mine management.He is a Graduate Engineer in Mining and Metallurgy of the “Universidad Nacional Autonoma de México”.

Prior to joining La Negra Mine, Mr. Canseco worked with Grupo Mexico (IMMSA) as Mine Supervisor and Mine Assistant Superintendent. He also held the position of Manager with Peñoles Group, Director of Mining Constructions for the Ministry of Economy, Manager of Minera Guadalupe, Minera Victoria, Minera Nukay as well as Project Assistant with Baja Mining in Santa Rosalía, B.C.S.

Mr. Ted Apodaca, General Manager, Shafter Mine

Mr. Ted Apodaca has over 30 years of experience in Mining and General Construction that include mine development from start-ups to turn key operation, mine operation, mills construction as well as underground mining techniques and shafts sinking. He operated various mining operations in Brasil, Venezuela, Panama, Indonesia, Bolivia and Honduras.

Board Of Directors

Bob Tweedy, Director-Chairman

- Chairman of Useppa Holdings

- Trustee of Dundee REIT

Adrian Aguirre, Director

- Vice Chairman of Maxcom Telecomunicaciones

Ken Collison, Director

- SVPP Project Development of Avanti Mining

- Former COO at Thompson Creek Mines

Paul Matysek, Director

- Former President & CEO of Potash One

- Director of Lithium One, Nevada Copper, and Forsys Metals

Arthur H. Ditto, Director

- Former COO of Kinross Gold Corp

- Over 40 years of mining experience

Technical Advisors

Jerry Blackwell

In mining exploration since 1970. Worked with Cominco Ltd., and has also been a consulting geologist. Director of Gitennes Exploration Inc. since 1993 Served as an Officer and Director of numerous listed-companies where his geological expertise, management style and integrity have been greatly valued. Over 39 years of mineral exploration and development experience.

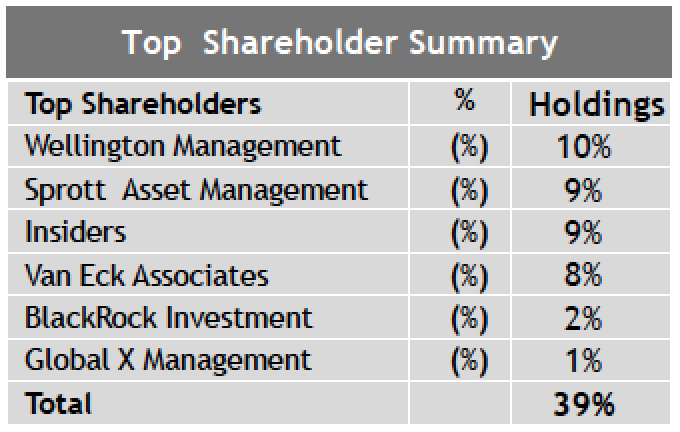

Capital Structure and Ownership*

Issued & Outstanding: 58.4 Million

Warrants: 9.1 Million

Options Outstanding: 4 Million

Cash: ~$10 Million

Investments: $1 Million

Leased Equipment: $9 Million

52 Week Low: $2.80 52 Week High: $10.08

* as at May 1, 2013

High-Quality Assets in Favourable Mining Jurisdictions

Shafter – Pure Ag Mine

- 100% ownership

- Commercial production started Dec 14, 2012, followed by production ramp up in 2013

- Anticipating 3.8mm Ag oz at US$10/oz cash cost in a 12 months period while running continuously at 1,500tpd

- 99.9% ownership

- 2012 annual production of 2.5 mm oz silver equivalent

- 2012 YTD as of Q3 2012, silver equivalent cash cost was negative $0.21

Emerging Senior Silver Producer with Leading Growth Profile

Significant Production Upside Potential

Identified growth opportunities support potential for combined annual production of up to ~10mm oz. Ag equivalent per year.

Identified Growth Opportunities: 12 Month Production Potential

La Negra: ~ 2.9 million ounces Ag. Eq. to ~ 4.3 million* ounces Ag. Eq.

- Capacity Expansion

- Mill Head Grade Improvements

- Resource Expansion

Current Capacity: 3,000 tpd

*Assumes average mill head grade of 100g/t

Shafter: ~3.8 million ounces Ag. Eq. to ~6.3 million ounces Ag. Eq*

- Phase I – Ramp Up to Capacity

- Phase II – Capacity Expansion

- Resource Conversion Expansion

Phase I – 1,500 tpd

*Assumes linear increase in production from Shafter feasibility study with capacity expansion from 1,500 to 2,500 tpd

Strong Balance Sheet and Cash Flow Generation

Attractive Relative Valuation and Re-Rating Potential

La Negra – 99.9% owned Primary Silver Min

- Permits and agreements are in place with a high level of local community support.

- Awarded the 2013 Environmental and Socially Responsible Company (ESR) Award by the Mexican Center for Philanthropy (CEMEFI) for the La Negra Mine.

- Successful restart by Aurcana in 2007 at throughput of 1,000 tpd and now increased to 3,000tpd. Tailings facility expanded to accommodate up to 10 additional years of mine life

- 2012 annual Ag production of 2.5 million ozs silver equivalent at low cash costs net of by-products

- Significant production and exploration upside potential Ag production increase and mine life extension confirmed by new M&I resource estimate

La Negra, 43-101 Resource Report, Oct. 2012

October 10, 2012 – Aurcana published Technical 43-101 Resource Report at La Negra with 115mm M&I Ag oz,

- Includes significant base metal credits (Pb, Zn and Cu)

Increase in resource base supports extended mine life of operations and identified plans to increase throughput and Ag production.

- Supports extended mine life

Resource upside remains

- Deposit remain open in multiple directions

- Large system of underground levels and workings provides access to carry out additional exploration on surface identified targets

Surface Exploration Indicates Potential for Gold

- On Feb 12, 2013, Aurcana announced significant exploration results and new discoveries at La Negra

- Assay values range from 0.2gm/t to 15.3gm/t Au and are associated with strong silver, lead and zinc values

- Additional exploration program will follow in 2013.

Highlights

Zona Aurifera I

- 15.3gm/t Au and 261 gm/t Ag

- 12 gm/t Au and 105 gm/t Ag

- 10.0 gm/t Au and 381 gm/t Ag

Zona Aurifera II

- 2.8 gm/t Au and 229 gm/t Ag

- 2.4 gm/t Au and 307 gm/t Ag

- 2.8 gm/t Au and 95 gm/t Ag

Operations

La Negra Mine

- Multiple mining faces enables targeting higher grade ore

- Low cost long hole open stope mining and room and pillar mining methods

- $32.4/tonne milled (1)

- YTD Silver cash costs negative:- $0.21/oz.

(1)(2) - Grades improving on new zones

*(1) Year to date numbers based on Q3 2012 financials, costs are before general and administrative costs

- Average mill head grades of Silver ~80 g/t, Copper ~0.5% and Zinc ~1.2%

- 150 tonne per hour crushing capacity (avoids peak power rates)

Significant Upside Exploration Potential

- Drifting and drilling have been employed to expand tonnage to the current volume

- Recent significant surface exploration results and new discoveries of gold associated with strong silver, lead and zinc values will be followed with an exploration program

- Surface exploration has added potential targets that can be explored cheaply from underground

- Additional concessions were staked by Aurcana along the regional trend which will be explored for similar targets

- Regional structural controls (NW and NE) and intrusive/dike contacts are the main controls for ore bodies

- Intersections of these structures are good targets for underground exploration

- Large system of underground levels and workings provides access to carry out additional

exploration to test these targets

- Complexity (i.e., multiple pulses of intrusion/mineralization) have been observed

Shafter Mine – 100% Owned Pure Silver Mine

- Located 375km southeast of El Paso, Texas in a

historic mining region - Extension of the ore body from the historic Presidio Mine

- Commenced test mining in April 2012

- Commercial production started Dec 14, 2012 and ramp up to phase I, 1500tpd capacity in 2013

- Expected 12 months production of 3.8mm oz. Ag. at approx. US$10/oz. cash cost, as soon as mill is running continuously at 1,500tpd for 12 months

- Significant production and exploration upside

potential

*Based on year 1 of Shafter feasibility study

Source: June 23, 2011 amended Shafter Feasibility Study

Note: Measured and indicated resource includes reserves

Significant Production Scale

)

Shafter will be the largest pure silver mine in the U.S and one of the largest primary silver mines in North America.

- Underground mining commenced from 3 stopes in Dec 2012

-

Decline has been completed and is beingused for the underground mining

-

Plant improvements underway including installation of additional filter presses and thickeners to support phase I full commercial production of 1,500tpd.

-

The addition of a Counter Current Decantation (CCD) will support future increase in production.

-

All permits in place for future expansion to 2,500 tpd

Growth Objectives

- Phase I – Ramp up the mine to its capacity of 1,500tpd during 2013

- Phase II – Expand mill and mine capacity to 2,500tpd from 1,500tpd in Phase I, as soon as mill and mine is continuously running at 1,500tpd

- Significant potential to expand mine life through conversion and expansion of mineral resource

- Resource remains open along strike, and potentially, at depth

- Move from Phase I production of 3.8 million ounces of silver to Phase 2 production of ~6.3 million of ounces of silver*

*Assumes linear increase in production from Shafter feasibility study with throughput expansion from 1,500tpd in Phase I to 2,500tpd in Phase II

Exploration Opportunities

- Deposit classified as an oxidized Carbonate Replacement Deposit (“CRD”)

- Potential to encounter additional mineralized mantos in favourable limestone beds at depth

- Similar Mexican CRD deposits support the existence of stacked mineralized mantos

- Current exploration focused on locating potential “feeder” system that formed the Shafter deposits

- Existing resource open along strike to the east

- Historic drilling stopped before end of mineralization

- Historic geophysical anomalies remain untested in east and west sectors

- Numerous past-producing mines and prospects in the area

- Anomalous silica/oxide concentrations NW of Shafter deposit

- Possible evidence of buried mineralization

Shafter Ore Body Cross Section

RBC Capital Markets, December 2012

Above average free cash flow potential: Given production growth, declining capital expenditures and robust forecast silver prices, we expect Aurcana has the potential to generate strong free cash flow over the next 3 years, with a projected free cash flow yield of 11.8%, above its peer average yield of 6.3%.

Production expected to more than triple: With the ramp-up of Shafter (Texas) and ongoing throughput improvements at La Negra (Mexico), silver production is expected to quadruple by 2015E with annual silver production forecast to increase to 6 MMoz from 1.5 MMoz in 2012E.

Aurcana is an up-and-coming silver producer that is expected to undergo significant production and cash flow growth over the next few years as its Shafter mine in Texas ramps up towards full capacity and throughput increases at its La Negra mine are completed.

With operations at Shafter expected to reach steady-state levels in Q4/2013, Aurcana is on the verge of becoming a Tier II silver producer (production in excess of 5 million ounces) joining the ranks of First Majestic Silver, Silvercorp and Silver Standard. As a Tier II silver producer, Aurcana is likely to garner additional investor and capital markets attention.

Given a renewed focus on exploration at Shafter and ongoing focus at La Negra, we expect exploration success to lead to reserve and resource growth. This should be viewed positively by the market given the ability to provide clarity on the mine lives of both assets, assuming overall grades remain relatively constant. At La Negra, drilling continues to demonstrate the potential for additional resources and reserves with exploration highlighting the underlying potential of previously known zones within the northeast and northwest trends.

Given the ability to provide an acquirer with meaningful production from two relatively low cost operations located within mining friendly and geo-politically stable jurisdictions, we believe that Aurcana could become a potential takeover target. We believe that should the company be able to successfully bring Shafter up to steady state run rates, a larger silver producer could take a run at the company.

With the expected ramp-up of Shafter and higher forecast silver prices, we expect Aurcana’s operating cash flow will increase significantly over the next three years with the company expected to generate $275 million ($0.51/sh) in operating cash flow through 2015 (Exhibit 3). After taking into account capital expenditures, we forecast Aurcana could generate $190 million ($0.35/sh) in operating free cash flow through 2015E (Exhibit 4). Based on the company’s current share price, the implied 3-year free cash flow yield is approximately 11.8% which compares to the average free cash flow yield of 5.8% for the silver producers within our coverage universe.

…Aurcana offers the highest projected production growth amongst the silver companies within our coverage universe…

Both La Negra and Shafter are under-explored assets and the current 43-101 compliant resources understate the size of each project.

Building the next big silver platform in Mexico: Given management’s strong track record of acquiring and developing valuable assets, we expect Aurcana to continue to expand its presence throughout the region via additional plant expansions or new acquisitionsMarket ignoring true scope of La Negra and Shafter: The market only values the company based on short mine life implied by current resources and reserves, in our view. Our key valuation assumption lies within the extension of mine life beyond that of 43-101 compliant reserves/resources. Our valuation is based on a sum-of-the-parts analysis of both the Shafter and La Negra projects.

Because the project is already operating and generating cash flow, we believe Aurcana’s strategic development can be largely-self funded, thereby reducing the dilution risk that other developing resources companies typically face when building expanding production.

Ramp at Shafter and La Negra. Mining operations started at Shafter in April 2012 and the incremental silver production is key to achieving mid-tier status. We expect the company to quickly ramp to the project’s 1,500 tpd designed capacity and track towards annual silver production of roughly 3.8 million ounces, making it the second largest primary silver mine in the United States.At Shafter, we believe management’s focus has been on mine development leaving the deposit and surrounding areas underexplored for additional resources. Exploration efforts at both projects are being overseen by a world-renowned expert credited with discovery of some of Mexico’s largest silver projects. We expect this focus on exploration to expand compliant reserves/resources and formally extend mine life by five years or more at both projects.

Building the next significant silver platform.

Downside scenario limited. Aurcana’s growth story is predicated on both the successful ramp of its assets and its ability to extend mine life from exploration, in our view. Delays in reaching full capacity and/or failure to delineate out years’ production would result in a valuation near current levels, based on our NAV models; however, we do not see this worst case scenario as likely and believe downside is limited.

If Shafter is able to reach its production targets, the project will be on pace to be the 14th largest producing silver mine in the world, second in the U.S behind Hecla Mining’s Greens Creek project in Alaska.

The Shafter deposit itself, as well as surrounding areas, are under-explored and represent a large opportunity for growth by expanding into a full mining district, in our view. Aurcana controls a significant land package surrounding Shafter, which has been home to a handful of other historic mining operation…An exploration program to discover and delineate new resource led by regional silver expert geologist Dr. Peter Megaw is underway. We expect periodic news flow form these activities to serve as catalysts for share price appreciation.

Stonecap Securities, August 2012, April 2013

While Shafter is the asset that will propel Aurcana into the ranks of mid-tier silver producers, La Negra is now shaping up to be just as or more valuable from an NPV perspective.

…We believe that at current share prices investors are buying La Negra at a good price and getting the potential upside from Shafter for free.

Edison Securities, December 2012

While the rapid transition to a major producer is never smooth and has its setbacks, we believe that the company is well positioned to deliver above the average industry earnings growth in the short to medium term. This should continue to provide support to Aurcana’s shares. We value the company at US$1.38

Valuation: Cheap on both multiples and DCF

…the stock is cheap relative to its peers, as we believe the market is missing the company’s robust growth proposition.

On the whole, having almost completed its major investment programme, the company is well positioned to benefit from high commodity prices,which, coupled with a rapid increase in production, should improve cash flow generation and FCF yield, potentially leading to higher shareholder returns.

As the company’s major investment programme, which was focused on upgrading processing capacity at La Negra and bringing Shafter into production,is out of the way, we expect Aurcana’s cash flow generation to improve dramatically in the coming years.

Forward-Looking Statements and Corporate Disclosure from Aurcana Corporation

No stock exchange, securities commission or other regulatory authority has approved or disapproved the information contained in this presentation. This Presentation includes certain “forward-looking statements”. All statements other than statements of historical fact, included in this release, including without limitation statements regarding potential mineralization and resources, reserves, exploration results, realization of production estimates, fluctuation in resource prices, actual capital costs, operating costs and expenditures and future plans and objectives of Aurcana, are forward looking statements that involve various risks and uncertainties. The mineral resource estimates contained here in are only estimates and no assurance can be given that any particular level of recovery of minerals will be realized or that an identified resource will ever qualify as a commercially mineable or viable deposit which can be legally and economically exploited. In addition, the grade of mineralization ultimately mined may differ from the one indicated by the drilling results and the difference may be material. The estimated resources described herein should not be interpreted as assurances of mine life or of the profitability of future operations. There can be no assurance that forward looking statements will prove to be accurate and actual results and future events could differ materially from those anticipated in such statements. Important factors that could cause actual results to differ materially from Aurcana’s expectations include, among others, risks related to international operations, the actual results of current exploration activities, unexpected delays in project development, conclusions of economic evaluations and changes in project parameters as plans continue to be refined as well as future commodity prices. Although Aurcana has attempted to identify important factors that could cause actual results to differ materially, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking statements.

This presentation includes disclosure of scientific and technical information, as well as information in relation to the calculation of reserves and resources, with respect to the Shafter and La Negra Projects. Aurcana’s disclosure of mineral reserve and resource information is governed by National Instrument 43-101 – Standards of Disclosure for Mineral Projects (“NI 43-101”) under the guidelines set out in the Canadian Institute of Mining, Metallurgy and Petroleum (the “CIM”) Standards on Mineral Resources and Mineral Reserves, adopted by the CIM Council, as may be amended from time to time by the CIM.

Certain information in this presentation is derived from the following technical reports, “Technical Report on Shafter Feasibility Study”, dated June 23, 2011, “Mineral Resource Estimate Maravillas Deposit La Negra Mine”, dated February 16, 2010, “Mineral Resource Estimate Monica Deposit La Negra Mine” dated July 22, 2008 and “Technical Report on the Mineral Resources and Mineral Reserves of the el Alacran Deposit of the La Negra Silver, Lead, Zinc, Copper Mine Queretaro, Mexico”, dated February 2008. Copies of the reports are available on the SEDAR website under Aurcana’s profile at www.sedar.com. The technical contents of this presentation were reviewed and approved by Nils von Fersen, P.Geo, the Vice President of Exploration of Aurcana and a Qualified Persons (“QP”) as defined by National Instrument 43-101 (Standards of Disclosure for Mineral Projects).

Cautionary Note to United States Investors Concerning Estimates of Measured, Indicated and Inferred Resources:

These tables use the terms “Measured”, “Indicated” and “Inferred” Resources. United States investors are advised that while such terms are recognized and required by Canadian regulations, the United States Securities and Exchange Commission does not recognize them. “Inferred Mineral Resources” have a great amount of uncertainty as to their existence, and as to their economic and legal feasibility. It cannot be assumed that all or any part of an Inferred Mineral Resource will ever be upgraded to a higher category. Under Canadian rules, estimates of Inferred Mineral Resources may not form the basis of feasibility or other economic studies. United States investors are cautioned not to assume that all or any part of Measured or Indicated Mineral Resources will ever be converted into Mineral Reserves. United States investors are also cautioned not to assume that all or any part of a Mineral Resource is economically or legally mineable.

Disclaimer and Disclosure

Equedia.com & Equedia Network Corporation bears no liability for losses and/or damages arising from the use of this newsletter or any third party content provided herein. Equedia.com is an online financial newsletter owned by Equedia Network Corporation. We are focused on researching small-cap and large-cap public companies. Our past performance does not guarantee future results. Information in this report has been obtained from sources considered to be reliable, but we do not guarantee that it is accurate or complete. This material is not an offer to sell or a solicitation of an offer to buy any securities or commodities.

Furthermore, to keep our reports and newsletters FREE, from time to time we may publish paid advertisements from third parties and sponsored companies. We are also compensated to perform research on specific companies and often act as consultants to many of the companies mentioned in this letter and on our website at equedia.com. We also make direct investments into many of these companies and own shares and/or options in them. Companies do pay us to advertise on our website and we often distribute our reports on featured companies. While we are never paid to write a rosy and positive report on any company, we do market our reports using the advertising fees paid for by our featured companies.

This process allows us to continue publishing high-quality investment ideas at no cost to you whatsoever. Our revenue is generated by sponsor companies and we grow our readership by using the advertising fees we charge to distribute our reports. This helps both Equedia and our client companies gain exposure and allows us to provide you with our research at no cost.

Therefore, information should not be construed as unbiased. Each contract varies in duration, services performed and compensation received.

If you ever have any questions or concerns about our business or publications, we encourage you to contact us at the email or phone number below.

Equedia.com is not responsible for any claims made by any of the mentioned companies or third party content providers. You should independently investigate and fully understand all risks before investing. We are not a registered broker-dealer or financial advisor. Before investing in any securities, you should consult with your financial advisor and a registered broker-dealer. The information and data in this report were obtained from sources considered reliable. Their accuracy or completeness is not guaranteed and the giving of the same is not to be deemed as an offer or solicitation on our part with respect to the sale or purchase of any securities or commodities. Any decision to purchase or sell as a result of the opinions expressed in this report OR ON Equedia.com will be the full responsibility of the person authorizing such transaction.

Please view our privacy policy and disclaimer to view our full disclosure at http://equedia.com/cms.php/terms. Our views and opinions regarding the companies within Equedia.com are our own views and are based on information that we have received, which we assumed to be reliable. We do not guarantee that any of the companies will perform as we expect, and any comparisons we have made to other companies may not be valid or come into effect. Equedia.com is sometimes paid editorial fees for its writing and the dissemination of material and the companies featured do not have to meet any specific financial criteria. The companies represented by Equedia.com are typically development-stage companies that pose a much higher risk to investors. When investing in speculative stocks of this nature, it is possible to lose your entire investment over time. Statements included in this newsletter may contain forward looking statements, including the Company’s intentions, forecasts, plans or other matters that haven’t yet occurred. Such statements involve a number of risks and uncertainties. Further information on potential factors that may affect, delay or prevent such forward looking statements from coming to fruition can be found in their specific Financial reports. Equedia Network Corporation., owner of Equedia.com has been paid $9166 plus HST per month for 12 months which totals $110,000 plus hst of advertising coverage for Aurcana Corporation on equedia.com plus any additional expenses we may incur as a result of additional distribution. Aurcana Corporation has paid for this service. We have also been granted 25,000 options at $6.32 which expires on February 28, 2015 with a full vesting period of one year, by Aurcana Corporation. Equedia.com may purchase shares of Aurcana Corporation without notice and intend to sell every share we purchase for our own profit. We may sell shares in Aurcana Corporation without notice to our subscribers. We currently do not own shares of Aurcana Corporation, but will likely buy shares in Aurcana Corporation following this initial report.

Equedia Network Corporation is also a distributor (and not a publisher) of content supplied by third parties and Subscribers. Accordingly, Equedia Network Corporation has no more editorial control over such content than does a public library, bookstore, or newsstand. Any opinions, advice, statements, services, offers, or other information or content expressed or made available by third parties, including information providers, Subscribers or any other user of the Equedia Network Corporation Network of Sites, are those of the respective author(s) or distributor(s) and not of Equedia Network Corporation. Neither Equedia Network Corporation nor any third-party provider of information guarantees the accuracy, completeness, or usefulness of any content, nor its merchantability or fitness for any particular purpose.

Great report. I have been following Aurcana for some time and I too agree this company is ripe.

By luck got in at near lows in July and this article being sometime before gives me great joy that my guessing makes me feel smart. Though there’s always risk your writings here are proving to follow the great potential you explained some months ago. Very easy to understand for the not so bright, like myself. Great job explaining this investment

chanel 財布 がま口