Silver is undeniably one of the most favoured investment vehicles for the top minds in the industry. From its ability to rise with a growing economy, to a precious metals hedge against inflation, silver is a metal with many talents.

Over the past six months, we have tracked the performance of many of the silver miners and explorers – our favourite way to play the silver boom.

Many silver stocks have increased dramatically since the beginning of this year. As a matter of fact, one company featured in our past Special Report Edition increased almost 100% in just two short months. However, despite a strong run, many silver stocks have recently experienced a strong sell off.

With the exception of one:

Minco Silver Corp (TSX: MSV) (OTCPK: MISVF)

Looking for the right company is like finding a needle in a haystack or being a kid in a candy store. Whatever figure of speech you use, it’s just plain difficult – especially in this market.

But if you are looking for a pure silver play, no company makes more sense to us than Minco Silver Corp (TSX: MSV) (OTCPK: MISVF). We’re not the only ones who think so.

The Largest Pure Silver Play in China?

Experts at both Raymond James and BMO Capital Markets have buy ratings for Minco Silver and both believe that the next few months may “potentially be a company-changer.”

BMO just upgraded Minco Silver with a target price of $3.00, while Raymond James has a target price of $3.35, with a NAV (Net Asset Value) of $4.26/per share. Target prices from large institutions are often very conservative, factoring in every possible risk.

But as you will read later, these target prices could easily be raised if Minco Silver achieves a very important milestone – one both BMO and Raymond James expects to happen anytime now.

This milestone has the potential to make Minco Silver the largest pure silver play in China – an incredible feat when you consider China`s prowess in commodities.

The Fuwan Silver Project

Minco Silver (TSX: MSV) (OTCPK: MISVF) is a pure silver play with a 43-101 resource of 158 million ounces* in their Fuwan Silver Project in Guandong, China.

Fuwan is a world-class silver deposit located on the Fuwan silver belt – a belt with a strike length of 10km. It has significant potential for expansion as it encompasses over 200 km2, of which less than 2% has been drilled to date.

The silver zones of the Fuwan are shallow (250-450m deep), high grade, flat-lying, strata bound, with a total strike length of 2.8 km.

Contiguous with the Fuwan deposit, Minco Silver and its sister company Minco Gold have already delineated several deposits within the district totalling 180Moz of silver and 1Moz of gold.

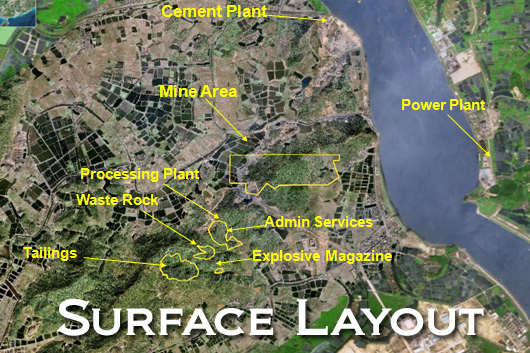

Infrastructure

The location of the Fuwan silver project makes it very attractive and translates into very low capital requirements when compared to other mines of this size.

It is accessible by paved highway and nearby waterway. Power, water, fuel and supplies are also easily obtainable. The property can also accommodate everything required for a mine including tailings dam, waste disposal, and processing plant sites.

The majority of reserves and resources (~60%) are contained within two zones which will reduce mine development requirements – saving money for Minco Silver and adding even more value to shareholders.

Take it to the Bank

Of the 158 million ounces that Minco Silver owns, 55 million ounces are reserves.

Unlike your standard indicated and inferred resource, reserves are resources that you can literally take to the bank and use as collateral for financing.

Minco Silver has already completed a “bankable feasibility” – this means their project is both profitable and makes sense (see Taking the Next Step for info on feasibility studies).

Based on the results of a Q4/09 feasibility study managed by Wardrop Engineering, the Fuwan deposit is expected to produce an average of 5.5Moz of silver at cash costs of US$5.65/oz over a 9.2-year mine life based on a 55.4Moz silver reserve. That means that Minco Silver is expected to produce close to $100 million in revenue and over $69 million net profit with current silver prices.

To give you an idea of what 5.5Moz could mean for Minco Silver, let’s use Silvercorp Metals (TSX, NYSE: SVM), a primary silver producer in China, as a comparable. In 2009, Silvercorp pulled close to 4.2Moz of silver out of the ground and is forecasted to pull just over 4.6Moz in 2010. They have a current market cap of ~$1.15 billion. That’s more than 10 times Minco Silver’s current market cap of just over $110 million!

If production commences, Minco Silver will have annual revenues nearing its own current market cap. Don’t forget that this forecast is based on only 55.5 million ounces, and not the total resource of 158 million Minco Silver has already found.

Bankable feasibilities take time and a lot of money. Not only has Minco Silver accomplished this, they have done this without major dilution and without incurring debt.

Moreover, they have $21 million dollars in the bank, and another $2.75 million in interest payments is expected to fill their treasury soon.

Minco Silver is already a great story when you consider it has a bankable feasibility study, no debt, $21 million dollars, and just over 50 million shares outstanding on a fully diluted basis.

But the real upside to this story lies in something that is expected to happen at anytime…

Timing is Crucial

Minco Silver (TSX: MSV) (OTCPK: MISVF) is on the brink of a very historical milestone – the same milestone that helped propel Silvercorp’s share price through the roof: the receipt of their EIA (environmental impact assessment) permit from the Chinese government.

To give you an idea of how big this is, take a look at the price performance chart for Silvercorp below:

As you can see in the above chart, Silvercorp’s share price slowly increased as they moved toward the EIA approval – very much like Minco Silver has to date. This is a very similar situation and is a sound reason why Minco Silver has gained in share value over the last few months, while other silver companies have dropped.

You can see how Silvercorp’s share price continued to increase substantially following the receipt of their EIA approval – more than tripling in share price in a few short months and continually climbing in the subsequent years.

Once Minco Silver receives this permit, the Mining permit is simply a formality and should follow shortly – as was the case with Silvercorp, who received their mining permit a few short months after their EIA approval.

Minco Silver already has the following approved:

- Chinese exploration report approved by MOLAR (Ministry of Land and Resources)

- Chinese Feasibility Study

- Project Approved by Gaoming county government

- Soil and Water Conservation Plan

- MAP (Mining Area Permit) approved by MOLAR

- Land use permit

In essence, the receipt of their EIA permit is more of an administrative formality than anything.

But we know permitting processes are often intertwined with political and social roadblocks – especially in a country like China.

But that’s where Minco Silver shines.

At the helm of Minco Silver is Dr. Ken Cai, a Chinese national who has been the driving force behind many property negotiations in China.

Not only that, he has a wide range of high-level contacts in the Chinese mining communities and this has allowed Minco to access data on a large number of projects throughout China.

Speaking from personal experience, Minco Silver’s Dr. Ken has some serious connections in China. He not only has the right contacts in the Chinese government, but has structured Minco Silver in a way that will allow them to operate as a Chinese company – a very important step if you want to operate a large scale mine in China.

It takes some due diligence to understanding the intricacies of what Dr. Ken Cai has done. But we can assure you, from our personal experience with other public companies, that no other company has been able to do what Minco Silver has.

But don’t just take our word for it, see what the large institutions have to say:

“We believe Minco Silver offers a compelling buying opportunity given that critical catalysts and milestones (final permitting, financing, etc) are merely months away…” – Raymond James, April 2010

“We continue to expect the Environmental Impact Assessment to be approved, which should be followed by receipt of a mining license, within the next several months. We recommend investors accumulate Minco Silver shares ahead of these key announcements.” – Raymond James, April 2010

“Development costs to construct a 3ktpd underground mine and flotation plant at Fuwan of ~US$73M are low by international standards and represent a low barrier to initial development.“ BMO Capital Markets, February 2010

“Given the larger footprint of mineralization at Fuwan, BMO Research views the prospects of both an increased mine life and future expansion through consolidation of the Fuwan camp as realistic.” BMO Capital Markets, February 2010

Both BMO and Raymond James are expecting Minco Silver to receive their EIA permit anytime now. That’s perhaps why Raymond James is calling 2010, Minco Silver’s “company-changing year.”

One quick glance at Minco Silver Corp (TSX: MSV) (OTCPK: MISVF) and you can clearly see what it has over other companies:

- one of the lowest shares outstanding compared to its peers with a tight capital structure

- $21 million in the bank with no debt

- 43-101 resources of over 150 million ounces, with 55 million ounce probable “reserves”

- Coverage and buy targets from large financial institutions such as Raymond James and BMO Capital Markets

- A potential takeover target, as mentioned by BMO

- On the verge of a historical milestone at any moment

With an estimated float of 11 million shares, Minco Silver (TSX: MSV) (OTCPK: MISVF) has done a great job of attracting institutions but have yet to realise its retail capabilities. With such a small float, retail investors will be playing catch up with the institutions if Minco Silver receives their EIA permit.

Minco Silver is expecting to receive their EIA permit anytime now. When this happens, it will spell big rewards for the Company and its shareholders.

Minco Silver could be on its way to becoming one of the largest pure silver plays in China…

Minco Silver Corporation

Cdn Symbol: (TSX: MSV)

US Symbol: (OTCPK: MISVF)

*Minco Silver owns 100% of the Fuwan Silver Deposit, subject to a 10% profit sharing agreement with the Guangdong Geological Exploration and Development Cooperation.

For the full interactive newsletter and report, please follow this link: http://archive.constantcontact.com/fs005/1102243211822/archive/1103478771778.html

If you have not already subscribed to Equedia Weekly, you may sign up here: http://equedia.com/newsletter/

Disclaimer and Disclosure

Disclaimer and Disclosure Equedia.com & Equedia Network Corporation bears no liability for losses and/or damages arising from the use of this newsletter or any third party content provided herein. Equedia.com is an online financial newsletter owned by Equedia Network Corporation. We are focused on researching small-cap and large-cap public companies. Our past performance does not guarantee future results. Information in this report has been obtained from sources considered to be reliable, but we do not guarantee that it is accurate or complete. This material is not an offer to sell or a solicitation of an offer to buy any securities or commodities.

Equedia.com has been compensated to perform research on specific companies and therefore information should not be construed as unbiased. Each contract varies in duration, services performed and compensation received. Equedia.com is not responsible for any claims made by any of the mentioned companies or third party content providers. You should independently investigate and fully understand all risks before investing. We are not a registered broker-dealer or financial advisor. Before investing in any securities, you should consult with your financial advisor and a registered broker-dealer. The information and data in this report were obtained from sources considered reliable. Their accuracy or completeness is not guaranteed and the giving of the same is not to be deemed as an offer or solicitation on our part with respect to the sale or purchase of any securities or commodities. Any decision to purchase or sell as a result of the opinions expressed in this report OR ON Equedia.com will be the full responsibility of the person authorizing such transaction.

Please view our privacy policy and disclaimer to view our full disclosure at http://equedia.com/cms.php/termsr. Our views and opinions regarding the companies within Equedia.com are our own views and are based on information that we have received, which we assumed to be reliable. We do not guarantee that any of the companies will perform as we expect, and any comparisons we have made to other companies may not be valid or come into effect. Equedia.com is paid editorial fees for its writing and the dissemination of material and the companies featured do not have to meet any specific financial criteria. The companies represented by Equedia.com are typically development-stage companies that pose a much higher risk to investors. When investing in speculative stocks of this nature, it is possible to lose your entire investment over time. Statements included in this newsletter may contain forward looking statements, including the Company’s intentions, forecasts, plans or other matters that haven’t yet occurred. Such statements involve a number of risks and uncertainties. Further information on potential factors that may affect, delay or prevent such forward looking statements from coming to fruition can be found in their specific Financnial reports. Equedia Network Corporation., owner of Equedia.com has been paid six thousand four hundred and thirty Canadian dollars plus gst/hst per month for 7 months which totals forty five thousand dollars plus gst/hst of advertisement coverage on Minco Silver Corporation. The company (Minco Silver Corporation) has paid for this service. Equedia.com currently owns shares of Minco Silver Corporation and may purchase shares without notice.We intend to sell every share we own for our own profit. We may sell shares in Minco Silver Corporation without notice to our subscribers. Equedia Network Corporation is a distributor (and not a publisher) of content supplied by third parties and Subscribers. Accordingly, Equedia Network Corporation has no more editorial control over such content than does a public library, bookstore, or newsstand. Any opinions, advice, statements, services, offers, or other information or content expressed or made available by third parties, including information providers, Subscribers or any other user of the Equedia Network Corporation Network of Sites, are those of the respective author(s) or distributor(s) and not of Equedia Network Corporation. Neither Equedia Network Corporation nor any third-party provider of information guarantees the accuracy, completeness, or usefulness of any content, nor its merchantability or fitness for any particular purpose.