Dear Readers,

Earlier this year, everyone thought I was nuts when I told them the S&P would reach 1500:

“I expect the S&P 500 to be trading above 1,500. While this would still be below its all-time high of 1,565 set in October 2007 (a key psychological number), it would be just enough to take the Dow to around 14,300, beating its high in October 2007 high by a couple of hundred points.” – April 1, 2012

The S&P is now at 1460. The Dow is 13,593.37.

I’ve said for years the only way to solve Europe’s debt problem was to federalize the countries of the eurozone:

“The only real way out of the European mess is to cut the Gordian knot through federalization, as the United States did many years ago” – June 19, 2011

What better way to federalize the countries than to implement a federalized banking system with one banking supervisor to oversee everything:

“Soon there will be one European-wide banking supervisor that can directly give banks cash as it pleases. He/she will force the issue of euro bonds – debt that would be jointly guaranteed by all European Union nations; German citizens will have to suffer (but at least they will have jobs). He will also engage in another large round of long-term lending to banks. He will force the issue of more printed money” – July 1, 2012

Everything I just mentioned has happened as predicted.

The European Central Bank’s (ECB) recently announced unlimited bond buying program just received approval by Germany’s highest court. That means there is no limit to the money they can print.

The United States just did the same.

In my first letter this year, I said that QE3 for 2012 was inevitable:

“Hopeful numbers will come out of the US but the economic decay in 2012 will eventually accelerate enough to overshadow any signs of hope. In order to avoid an outright economic collapse, the governments of the world, in particular the US, will once again be forced to initiate massive amounts of Quantitative Easing (QE)” – January 8, 2012

The massive initiation has begun.

The Fed, like the ECB, just announced its own unlimited bond buying program; buying $40 billion a month of mortgage-backed securities bonds that would be open ended until labor conditions improve.

That means they’ll keep printing until things get better, and beyond.

Some are saying the amount could reach anywhere between $800 billion, and as high as $2 trillion. Instead of directly announcing a massive trillion dollar program, the Fed has instead announced increments of $40 billion per month.

Psychologically, $40 billion sounds a lot better than $2 trillion (perhaps that’s why gold didn’t punch through $1800.) Along with low interest rates until 2015 and a continued operation twist, that’s a balance sheet expansion of more than $85 billion per month ($45 billion/month operation twist + $40 billion/month QE).

Think that’s bad?

Take a look at what the Fed had to say:

“A highly accommodative stance on monetary policy will remain appropriate for a considerable time after the economic recovery strengthens.” September 13, 2012

In other words, Bernanke is not only going print until his policy works, but he will leave his loose monetary policy in play even if the economy strengthens.

Other experts around the world are already predicting his QE programs won’t work. QE2 hasn’t created more jobs – yet. So does that mean we’re going to keep printing, and printing, and printing? Didn’t believe me about QE to infinity?

Believe me now?

Currency Wars

For the last few weeks, I have been providing insight on our current financial war. The main point you should take away is that the winner is the nation that devalues its currency the fastest.

While this may sound counterintuitive, the less your currency is worth, the more exports you attract. And when a country cannot sustain itself through its own growth, it must rely on its exports. The only way you’re going to increase exports is to decrease the value of your currency so it becomes attractive for foreign countries to invest in, and purchase, from your nation.

The topic of currency war may not only shock you, but it may also offend you.

I have a lot of readers in Germany, so please take what I say next with a grain of salt, as I am merely making a point.

Germany’s Angela Merkel is an absolute genius.

She knows that printing money is going to devalue and inflate. She supports the Euro knowing it brings in more money for Germany. The devalued euro has turned Germany into an export powerhouse. The weaker euro has boosted Germany’s net exports, raised German wages and prices, and reduced the trade imbalance within the eurozone.

In other words, Germany has seen the strongest productivity growth in the Eurozone area.

While a lower euro and an unlimited bond buying program means Germany gains an upper hand in exports, inflation could eventually disrupt the natural balance of trade.

When the deflationary tendencies of the euro are overshadowed by inflation caused by an unlimited bond buying program, that’s when things can get out of hand. However, we’re not there yet. And believe me, when we are, Germans are not going to be the only one suffering.

So while German citizens argue against the policies presented by Merkel, those policies have given Germany an upper hand whereby they can combat their own inflationary worries with the deflationary tendencies of the euro.

When all of this comes to a halt, Germany will come out on top. Merkel wants a federalized Europe. And she wants Germany to be in control.

For now, the world is buying more from Germany, while its citizens pay more for everything else. More jobs, less purchasing power. That means people will have to work harder, for less. But hey, at least they have work.

Unlike the United States. Or anywhere around the world where currencies have been strong.

Such as Canada.

US Dollar vs the World

The more the U.S. prints, the stronger other world currencies become in relation to the dollar. As a result, this causes decreased exports for other countries around the world.

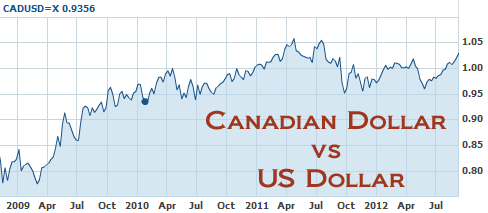

Here’s a look at the CAD dollar vs. U.S. dollar chart:

|

| Source: Yahoo Finance |

It’s clear the Canadian dollar has been rising against the U.S. dollar over the past few years. But while the average Canadian is happy they get to go across the border and buy cheap clothes, the country is suffering.

Canada’s trade deficit is the worst it’s ever been. Canada’s trade performance hit a new low in July, establishing a record deficit of $2.3 billion as both exports and imports tumbled in the face of a weak global economy.

Making matters worse, Statistics Canada revised June’s deficit to $1.93 billion, even deeper than the $1.81 billion deficit originally reported just months ago.

Canada’s not the only one feeling the effects of America’s printing press.

Look at the Japanese Yen vs. the U.S Dollar:

|

| Source: Yahoo Finance |

Last year, Japan has reported its first annual trade deficit in 30 years.

Japan’s trade deficit will grow sharply to Y840.0 billion in August from Y518.9 billion in July, marking a deficit for the second straight month on slower global demand.

Look at the Aussie dollar:

|

| Source: Yahoo Finance |

Data from the Australian Bureau of Statistics showed that Australia’s trade deficit widened in July. The country has recorded its seventh straight trade deficit in July.

Now here’s the best chart of all. It explains much of what I have been talking about for the past few weeks.

The Chinese Yuan vs. United States Dollar:

|

| Source: Yahoo Finance |

Take notice that for years the yuan never moved in relation to the dollar…until the last couple of years. It’s the US Dollar vs the World currencies.

In my last letters, I explained that QE was the United States’ secret weapon against China’s reluctance to appreciate their yuan against the dollar:

“Prior to 2011, no one was winning the currency war. China was experiencing a surplus and the US was negative. So the U.S. did everything it could, including persuasions through the G20, to convince China to appreciate their currency to balance out the major trade deficit. But China wouldn’t allow their yuan to appreciate because it would hamper their own growth. Why would they hamper their growth for the benefit of a competing country?

As a result, the United States, empowered by its world reserve status, pulled out its secret weapon: Quantitative Easing (QE). The United States effectively devalued its own currency by increasing its own money supply, forcing inflation onto China.”

Remember, last week I told you that currency is the target for any financial war and the United States is doing everything it can to fix the trade deficit between itself and China? The only way to do this is for the yuan to rise against the dollar.

We’re in a full-fledged currency war. QE is the bullet, the dollar is the gun, and the United States is the trigger man.

And we’re all the innocent bystanders.

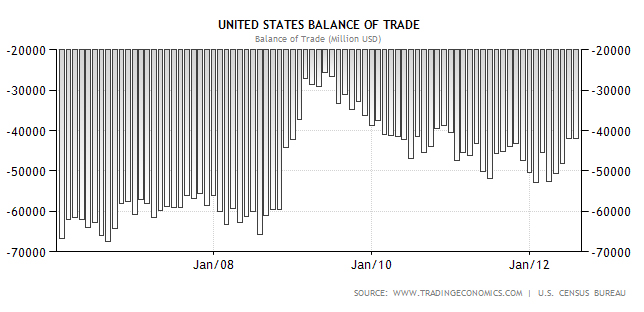

Think QE hasn’t been working? Take one good look at the chart above. Now take a look at the chart below:

The United States is slowly, very slowly, improving its trade deficit. However, their QE weapon is working at the expense of other countries. It’s no wonder why there are anti-American protests all over the world.

As I mentioned weeks ago:

“Countries around the world are feeling the effects of this currency war. It’s created higher food prices in Egypt and stock bubbles in Brazil.

Printing money means that U.S. debt is devalued so foreign creditors get paid back in cheaper dollars. The devaluation leads to higher unemployment in developing economies as their exports become more expensive to Americans.

While inflation isn’t so bad on the home turf, developing countries experiencing even a slight rise in prices are feeling the tremors. Rising food prices for us are an inconvenience, but for those of smaller developing nations, it’s a matter of life and death.”

Two of the world’s superpowers just announced unlimited bond buying programs. What will be the market’s next move? What will be the next big spark to infuse the market now that QE3 has been announced?

What to Do Now

I am a big believer in investing based on what we know, rather than guessing on what we don’t. Long-time readers know I rely on this theory more than anything.

Given the world’s current currency battle, all I know is that we need to protect ourselves by investing in hard assets. Obviously, that means all precious metals such as gold and silver, as well as real estate, fine arts, and other hard assets.

Gold should not be overlooked – especially now that the two superpowers have announced they will be printing endlessly.

However, even with the ECB’s unlimited bond buying program and an open-ended QE by the Fed, Gold did not break through $1800. I am scratching my head on this one. Could it be manipulation? Or did QE simply give a big enough cushion for the big money to take more risks and enter back into stocks?

Gold and silver’s RSI indicate that both metals are overbought. But in this market, it’s hard to rely on technicals for the short term.

This new round of QE is giving the under invested funds something to work with. QE gives the banks a cushion, allowing them to take more risks. That means their capital will be going into stocks, instead of hard assets.

One thing I know for sure is that gold stocks have been seriously outperforming gold over the past few weeks – finally!

Bankers are becoming more aggressive in purchasing gold stocks and those with a growing production profile and high grade projects near already producing mines are gaining serious traction. That includes the companies featured in my reports this year (see below).

The money being injected into gold and silver stocks will soon be so explosive that the right plays will make us all a ton of money.

QE is the assasination of wealth. But only if you sit still.

Timmins Gold Corp (TSX: TMM) (NYSE MKT: TGD)

Now up 25%* since my initial report.

Balmoral Resources (TSX.V: BAR) (OTC: BALMF)

Now up 74%* since my initial report.

MAG Silver Corp (TSX: MAG)(NYSE.A: MVG)

Now up 45%* since my initial report.

*based on Canadian share price

I still haven’t sold a single share in any of the three companies I just mentioned.

Until next week,

Ivan Lo

Equedia Weekly

Questions?

Call Us Toll Free: 1-888-EQUEDIA (378-3342)

Disclosure: I am long gold and silver through ETF’s and bullion, as well as long both major and junior gold and silver companies. We’re biased towards Timmins Gold Corp. because they are an advertiser, we own options, and we own shares. We’re biased towards MAG Silver because they are an advertiser and we own shares. We’re biased towards Balmoral because they are an advertiser and we own shares. You can do the math. Our reputation is built upon the companies we feature. That is why we invest in every company we feature in our Equedia Reports, including Timmins Gold Corp., MAG Silver, and Balmoral Resources. It’s your money to invest and we don’t share in your profits or your losses, so please take responsibility for doing your own due diligence. Remember, past performance is not indicative of future performance. Just because many of the companies in our previous Equedia Reports have done well, doesn’t mean they all will.

Furthermore, Timmins Gold, MAG Silver, Balmoral Resources, and their management, have no control over our editorial content and any opinions expressed are those of our own. Disclaimer and Disclosure Equedia.com & Equedia Network Corporation bears no liability for losses and/or damages arising from the use of this newsletter or any third party content provided herein. Equedia.com is an online financial newsletter owned by Equedia Network Corporation. We are focused on researching small-cap and large-cap public companies. Our past performance does not guarantee future results. Information in this report has been obtained from sources considered to be reliable, but we do not guarantee that it is accurate or complete. This material is not an offer to sell or a solicitation of an offer to buy any securities or commodities.

Furthermore, to keep our reports and newsletters FREE, from time to time we may publish paid advertisements from third parties and sponsored companies. We are also compensated to perform research on specific companies and often act as consultants to many of the companies mentioned in this letter and on our website at equedia.com. We also make direct investments into many of these companies and own shares and/or options in them. Companies do pay us to advertise on our website and we often distribute our reports on featured companies. While we are never paid to write a rosy and positive report on any company, we do market our reports using the advertising fees paid for by our featured companies.

This process allows us to continue publishing high-quality investment ideas at no cost to you whatsoever. Our revenue is generated by sponsor companies and we grow our readership by using the advertising fees we charge to distribute our reports. This helps both Equedia and our client companies gain exposure and allows us to provide you with our research at no cost.

Therefore, information should not be construed as unbiased. Each contract varies in duration, services performed and compensation received.

If you ever have any questions or concerns about our business or publications, we encourage you to contact us at the email or phone number below. Equedia.com is not responsible for any claims made by any of the mentioned companies or third party content providers. You should independently investigate and fully understand all risks before investing. We are not a registered broker-dealer or financial advisor. Before investing in any securities, you should consult with your financial advisor and a registered broker-dealer. The information and data in this report were obtained from sources considered reliable. Their accuracy or completeness is not guaranteed and the giving of the same is not to be deemed as an offer or solicitation on our part with respect to the sale or purchase of any securities or commodities. Any decision to purchase or sell as a result of the opinions expressed in this report OR ON Equedia.com will be the full responsibility of the person authorizing such transaction.

Please view our privacy policy and disclaimer to view our full disclosure at http://equedia.com/cms.php/terms. Our views and opinions regarding the companies within Equedia.com are our own views and are based on information that we have received, which we assumed to be reliable. We do not guarantee that any of the companies will perform as we expect, and any comparisons we have made to other companies may not be valid or come into effect. Equedia.com is paid editorial fees for its writing and the dissemination of material and the companies featured do not have to meet any specific financial criteria. The companies represented by Equedia.com are typically development-stage companies that pose a much higher risk to investors. When investing in speculative stocks of this nature, it is possible to lose your entire investment over time. Statements included in this newsletter may contain forward looking statements, including the Company’s intentions, forecasts, plans or other matters that haven’t yet occurred. Such statements involve a number of risks and uncertainties. Further information on potential factors that may affect, delay or prevent such forward looking statements from coming to fruition can be found in their specific Financial reports. Equedia Network Corporation., owner of Equedia.com has been paid $5833.33 plus HST per month for 6 months which totals $35,000 plus hst of media coverage on MAG Silver Corp. plus any additional expenses we may incur as a result of additional distribution. MAG Silver Corp. has paid for this service and has since extended this service for an additional 6 months for $40,000 plus HST. Equedia.com may purchase shares of MAG Silver without notice and intend to sell every share we purchase for our own profit. We may sell shares in MAG Silver Corp without notice to our subscribers. We currently own shares in MAG. Equedia Network Corporation., owner of Equedia.com has been paid $6666 per month for 6 months which totals $40,000 plus hst of media coverage on Abzu Gold Ltd. plus any additional expenses we may incur as a result of additional distribution. We have also been granted 150,000 options at $0.20 vesting over a one year period. Abzu Gold Ltd. has paid for this service. Equedia.com and its owner currently owns shares of Abzu Gold Ltd. and we may purchase more shares without notice. We intend to sell every share we own for our own profit. We may sell shares in Abzu Gold Ltd. without notice to our subscribers. Equedia Network Corporation., owner of Equedia.com has been paid $9167 plus HST per month for 12 months of advertising on Timmins Gold plus any additional expenses we may incur as a result of additional advertisements. We have also been granted 150,000 options at $2.15 by Timmins. Equedia.com and its owner may purchase shares of Timmins Gold Corp without notice and intend to sell every share we purchase for our own profit. We may sell shares in Timmins Gold Corp. without notice to our subscribers. We now own shares in Timmins purchased after the commencement of our advertisement. Equedia Network Corporation., owner of Equedia.com has been paid $7143 plus HST per month for 7 months which totals $50,000 plus hst of media coverage on Balmoral Resources Ltd. plus any additional expenses we may incur as a result of additional distribution. Balmoral Resources Ltd. has paid for this service in one lump sum. Equedia.com owns shares and may purchase shares of Balmoral Resources Ltd. without notice and intend to sell every share we purchase for our own profit. We may sell shares in Balmoral Resources Ltd. without notice to our subscribers.

Equedia Network Corporation is also a distributor (and not a publisher) of content supplied by third parties and Subscribers. Accordingly, Equedia Network Corporation has no more editorial control over such content than does a public library, bookstore, or newsstand. Any opinions, advice, statements, services, offers, or other information or con

tent expressed or made available by third parties, including information providers, Subscribers or any other user of the Equedia Network Corporation Network of Sites, are those of the respective author(s) or distributor(s) and not of Equedia Network Corporation. Neither Equedia Network Corporation nor any third-party provider of information guarantees the accuracy, completeness, or usefulness of any content, nor its merchantability or fitness for any particular purpose.