Aequitas Innovations, the Mother of All Bubbles, and Gold

Something was announced last week that could completely change the Canadian market.

Those looking for my coverage on the Canadian Housing Market will have to wait – I apologize.

A few weeks back, I wrote a letter on how big banks in Canada were taking over.

This past week the proof was once again in the pudding. But this time, it could actually be a good thing…maybe.

The TMX Killer?

Canada’s biggest bank, the Royal Bank of Canada, is now joining forces with mutual fund conglomerates IGM and CI Financial, pension fund PSP Investments and international banks ITG and Barclays, to create a new stock exchange that the creators say will keep costs low and discourage computerized high-frequency trading.

The new stock exchange is called Aequitas Innovations, the Latin word for fairness, and is expected to launch by the end of 2014, pending regulatory approval.

Given that such heavy hitters are involved, I expect the regulatory process to be just a formality.

My initial reaction was simple: Another stock exchange to remove more liquidity and transparency from the Canadian market. As if 10 multiple trading platforms weren’t enough, here we are with another full-blown stock exchange.

The CNSX hasn’t done much. Would could Aequitas Innovations possibly do?

But as I read through Aequitas’ position paper, this new stock exchange may actually benefit the market if launched correctly; it is actually attempting to solve many of the issues I have talked about over the past few weeks that are leading to the demise of the Canadian market.

Aequitas Innovations is looking to make trading a fair playing field once again by imposing restrictions on High Frequency Trading (HFT) and introducing many new innovations that are supposed to provide a more efficient market – including bringing back a more lenient dark pool trading platform and a marketplace for exempt securities.

Aequitas Innovation’s mission statement:

“Aequitas was founded by a group of stakeholders who believe today’s equity marketplaces do not provide the public with the fairness, efficiency and choice that encourage confidence and participation by investors, issuers and dealers.

The concentration of services, the dominant market structure model and lack of innovation are at the heart of this problem.

Our stakeholders include professional money managers, pension funds, sell-side institutions and issuers who believe choice, driven by competition and built on differentiation and innovation, is acutely needed in Canadian equity markets. The lack thereof threatens the long-term health of our equity markets, and therefore, ultimately, economic growth and employment.”

While it may sound like just another big bank trying to take a bigger piece of the pie, the players involved may actually have intentions of making the market better.

The presence of major mutual fund firms, who are generally known as the buy-side of the industry, makes Aequitas very different from other TSX alternatives that have come before.

Alpha Trading Systems, for example, a rival trading platform that made inroads before being dissolved when Maple Group gained control of the TSX last fall, was backed by the banks and big dealers.

Aequitas Innovations, on the other hand, is heavily backed by the buy-side, which clearly shows that the buy-side is taking a stand on their needs and interests.

Next week, I will be speaking with the people behind Aequitas Innovations to learn more about the new system.

If you have questions, please post them here and I will do my best to include them in my interview with the group.

Will Aequitas truly level the playing field for both small investors and issuers? Or will it cause more liquidity issues and make our already dying Canadian market worse?

I will cover this story in more depth next week. If you’re a Canadian, you won’t want to miss it.

Perception vs. Reality

In a recent interview with the Korelin Economics Report, I mentioned that the market has always been about perception rather than reality.

And the perception now is that everything is getting better; or at least that’s what the media will have you believe.

First of all, none of the theories you hear on super cycles, or technical trading patterns, really work anymore.

I’ve talked about this many times before: It’s a fed manipulated environment combined with software programs that control the majority of our market – both in Canada and the U.S.

Last week was a prime example of the manipulated efforts experienced in the last few years.

A Confused Market

Strong gains in U.S. orders for durable goods, the largest annual rise in housing prices in more than half a decade, and rising consumer confidence led the market higher.

As a result, speculation that the Fed would taper its stimulus scared everyone and stocks fell around the world.

The next day, the Fed forecasts slower U.S. growth and a once again downward revision of GDP, after US economic growth in the first quarter was a dismal 1.8% – far lower than the Fed’s earlier estimate of 2.4% growth*. This fueled speculation that the Fed will maintain stimulus. The market rises again.

(*How many times have we heard the Fed lower their GDP forecast in the past five years? I can’t even count anymore…)

First the media tells us the market is getting better; then the Fed tells us its not. The media tells us the fed will taper; then it tells us it won’t.

The media also tells us that housing numbers are better and prices are rising; yet U.S. mortgage applications are now down 7 of the last 8 weeks and have collapsed 29% over that time – the biggest plunge in 30 months.

These daily irrelevant news pieces fuel the fire for the HFT programs and cause dramatic swings in the market on a daily basis, based on the news feeds and “hot words” the programs grab for that day.

Forward-looking strategies simply aren’t working now.

But what happens when reality kicks in? What happens when the Fed finally tapers and GDP numbers are once again based on real growth?

Anyone still long the U.S. markets towards the end of this year should be extremely cautious. We still have some euphoria left in the system, but it’s trading – literally – on a very fine line.

There simply is no historical precedence for what we are experiencing and this will go down in history as the biggest financial crisis, blunder, or epiphany the world has ever seen.

Gold Forced Down Again

It’s now almost impossible to talk about the U.S. economy without talking about gold.

Gold plunged to a 34-month low and silver fell to the lowest point in nearly 3 years last week, as improving U.S. economic data strengthened the case for the Federal Reserve to reduce stimulus.

The 23 percent drop in Q1 represents one of the biggest drops in history.

Everything is working against gold right now.

The simple thought of the Fed tapering brings gold down. Yet the thought of continued stimulus also brings gold down because it shows deteriorating economic data (GDP miss), which implies less inflationary worries.

While gold has always acted as a safe haven against the financial system and against inflation, neither of those factors appear to be of concern anymore. Not in the short term, anyway.

But they should – especially against the financial system.

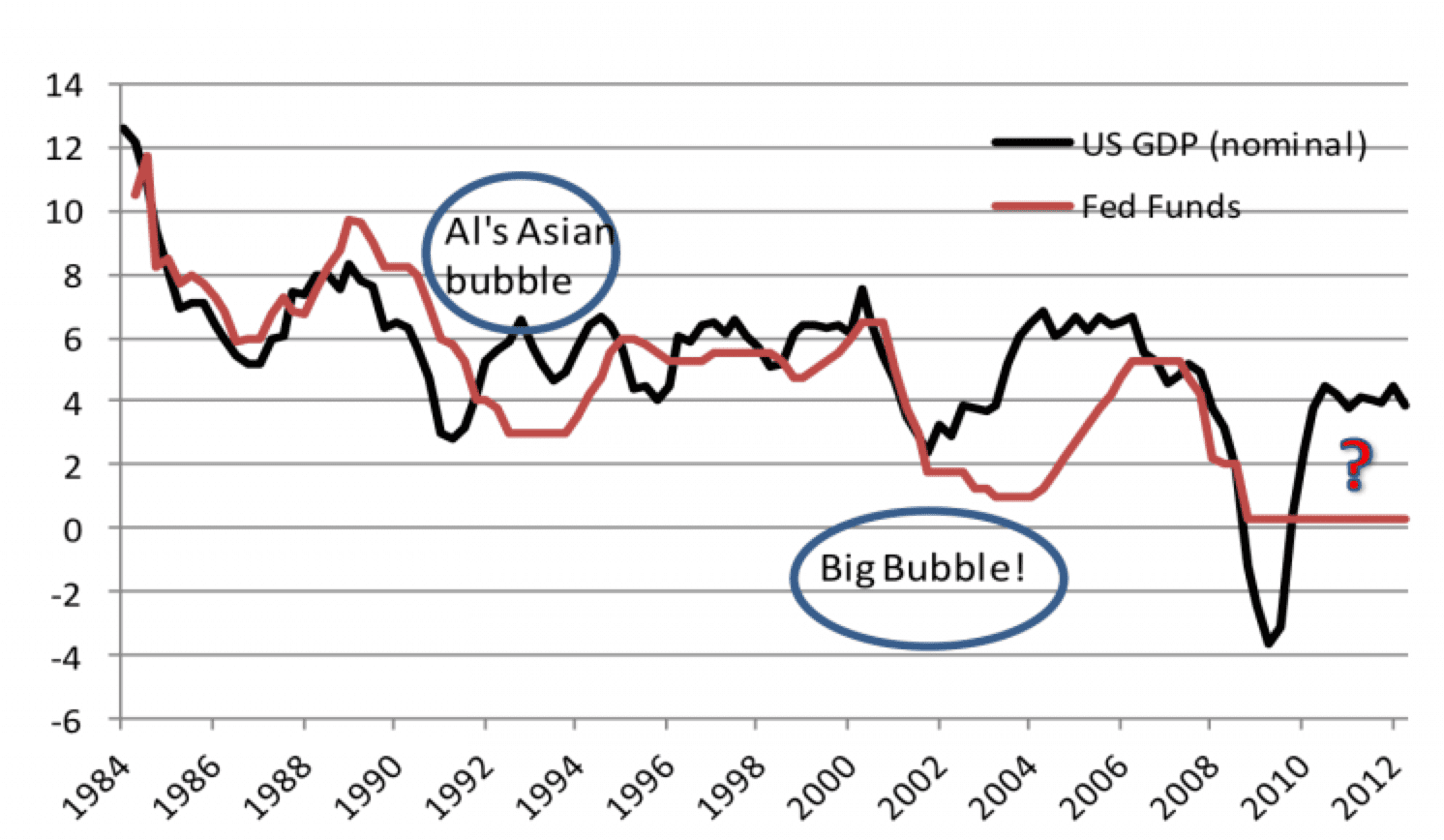

The Mother of All Bubbles

When nominal U.S. GDP diverges away from the Fed Funds Rate, it generally signals a forming bubble.

Via Kit Jukes of Societe Generale:

“All the big asset bubbles were caused by ludicrously easy money, in the form of Fed Rates below nominal GDP. Asia came from 1992/4 low rates, the dotcom and internet bubbles followed the cut in rates that was made after LTCM, and the big bad bubble followed years of monetary madness. The current gap between GDP and Fed Funds is the biggest/longest for ever.”

In Layman terms, there was the build up of the Asian bubble in the early 90s, the build up of the tech bubble in the late 90s, and the credit housing bubble leading up to 2008 in the mid-2000s.

In every instance, the divergence from U.S. nominal GDP away from the Fed Funds Rate can clearly be seen:

Notice the divergence in the last few years? It’s the biggest divergence in GDP and Fed Funds Rate we’ve ever had.

Interest rates are at all-time lows, and we have more printed money than ever before – not just in the U.S., but all over the world.

China’s Credit Bubble

China is another prime example of a bubble waiting to happen.

The country is experiencing a massive liquidity crunch right now and it’s not because of excessive money supply, but because of the highly leveraged risk money out on loans that will likely default.

The People’s Bank of China will be bailing out a lot more banks this year and the situation is a lot worse than most think.

Do you think we’re in a financial bubble?

Back to Gold and Inflation

As a safe haven against the financial system, gold still looks great.

However, we don’t currently have the inflation numbers that gold is supposed to protect against – not on American soil anyway.

In a more developed country, like the U.S., inflation won’t happen without real growth. The fact that we haven’t seen inflation in the U.S. proves that the current recovery and GDP growth has been fueled by stimulus rather than real economic drivers.

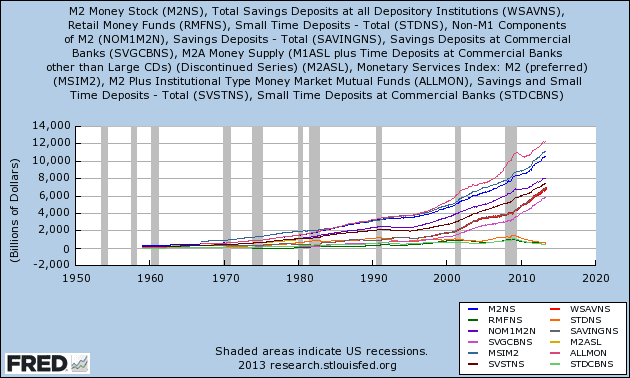

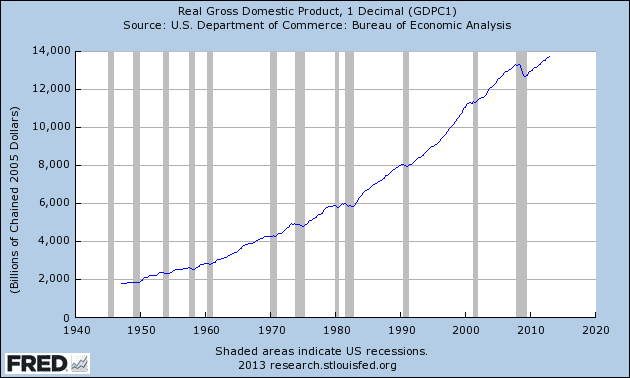

However, the consensus is that when the money supply grows faster than the rate of economic growth, we see higher sustained inflation.

Take a look at the growth of the U.S. money supply, as presented by M2 Money Stock:

Here is U.S. GDP growth:

Economists use M2 when looking to quantify the amount of money in circulation.

At the beginning of 2000, real GDP was around $11 trillion, while M2 money stock was at $4.6 trillion.

At the beginning of this year, real GDP was around $13.7 trillion, while M2 money stock was at $10.5 trillion.

That means GDP has grown 24.5% over the last 13 years, while M2 money stock has grown by more than 128%!

As I just showed you, the money supply in the U.S. is growing rapidly faster than the rate of economic growth — by a factor of 5 — yet we’re not seeing inflation at all. This is happening around the world.

When the U.S. and other developed nations begin to see real growth (not government manipulated data), inflation will come, and probably at a much higher rate than what we expect due to the amount of money in the system.

There isn’t an exact formula for inflation.

I’ve talked about money velocity, supply and demand, and long-term fundamentals for excessive money printing, but that doesn’t mean they’ll factor in together to create a massive rise in inflation all at once.

Supply and Demand – Fundamentals Remain Strong

If we talk about gold merely from a supply and demand perspective, demand for physical gold has never been higher in our modern era.

Both France and India have put import restrictions on gold and silver imports because their governments are worried citizens are spending too much on gold, and not enough on the direct economic input of their countries.

Gold premiums doubled in India on Wednesday. Central bank buying continues. Bullion dealers are struggling to keep up with demand.

Via the Telegraph:

“…Rob Halliday-Stein, the founder of BullionByPost, said the plunge in the price had increased enthusiasm for gold among his customers, describing Friday as a “record” day…

…”For every seller, there’s a buyer,” he said. “The sellers tend to be big and fast and the buyers smaller and slower.”

This really is the gold rush of the modern era. But because gold trades in two of the world’s most manipulated paper markets – London and the U.S. — gold continues to be manipulated.

From a technical perspective, we are really beginning to see signs of capitulation. Could gold move up violently from these levels? Yes – especially from a technical perspective. But will it?

If the demand from the paper market can find a trigger to bring back the big funds, then yes.

But I don’t think the funds will be that aggressive in the short-term – not while the risk-on mentality is still in effect.

We could see a short-term trade to the upside along with many miners, but don’t expect gold to move too violently up from this point as many suggest. We’ve seen this before, only for traders to hammer the price down further.

The long-term price is a completely different ballgame.

Clearly, the demand for physical gold is stronger than ever but we are still witnessing gold plunge.

That is more than enough evidence to prove that gold-backed ETFs are backed by paper, and not gold.

No one knows when, or how, this financial bubble will burst. Perhaps it will burst when interest rates begin to rise, when we witness another massive bank bailout, or when the Fed begins to taper.

The question is not if there is a bubble, but rather when it will pop.

The Equedia Letter

Good work Ivan. BUT! Regulations remain, despite the good intentions. IRROC will continue to kill the brokers. Venture capital is regulated, not by the exchanges, but by commissions. High frequency trading will be stopped before the new announced exchange will get launched.

http://www.businessweek.com/articles/2013-06-06/how-the-robots-lost-high-frequency-tradings-rise-and-fall#p4

And, remember, RBC was the one big bank that did not like the TMX deal and did not participate. It is still a big bank and thinks like a big bank.

Joe, thanks for the comment. I do agree regulation remains – despite the good intentions. And until I get more answers, the new exchange is still just a thought at this point.

I’ve read the article in business week before, but I doubt the HFTs will be stopped before the new exchange is launched. The tax “proposed” is for the U.S. exchanges and is only on futures and swaps – Canada is always a late follower.

If a real retail market comes back into the picture, the HFTs will once again make money, and once again force retail out.

I won’t be so quick to make a final judgement until I learn more, but at least there is a buy side group in the mix now. Its not a final solution – but at least its a start.

All for it , Obama must be made to listen and when more us dollars go to the better market with morals that support profit, he will have to listen but China has him under there thumb we need the North Country to stand it’s ground.

God’s Speed

Cathy Kandravi & Family

As a former trader I am all for creating a level platform for all. My big concern is how they will deal with ” Shorting “. This, to me, is where the market has shot themselves in the foot. Pro traders can short with impunity and have fun triggering ” Stops “. Have it strongly regulated. For use by market makers only when liquidity is needed or not at all. Let the people that want to dump on someones parade use other methods.

As far as the computerized trading is concerned it is totally unfair for dealers to have the edge on every trade.

Have a hard look at day traders and see if they are working together to create an illusion of active trading.

They will have to address all the issues in one go. The problem is, the TSX will now come out and try revert back or change the rules to stop the fraud THEY started. They will claim to be listening to the market. However, retail got wiped out so only big money will be trading.

Retail has to realize that all of this was planned. It was a theft or what in more polite circles they call, a transfer of wealth. So a new exchange comes and enshrines all the good that the retail desires. It will be a long time before retail has any substantial money but they will try to grow their positions non the less.

In the mean time, the big players will take up the base positions and they stand to have that edge plus the discount edge they were used to in the past. This is not going to turn the markets around. The theft has damaged the consumers!

All big money and smart people know that our entire monetary system is a house of cards. The derivatives are still out there and the money pools have to continue to be inflated in order to absorb that. We are talking 10 times global GDP! At the current rate we need at least another decade but will the people allow this?

Ivan cited Brazil and Venezuela, one look at them and you see the desperation setting in. These are not just the decade long repeats. These are countries who have reached the cracking point. While everyone is going along with printing no one boat floats higher than the others. But, when one boat starts looking like a submarine…. then everyone notices.

I wish I had as much faith as Ivan in bankers, and am glad he included the word ‘maybe’ in his intro. No doubt bankers are trying to pull back from the precipice of instability & public outrage, but given the enormous incentives involved, and the fact that this new exchange will permit HFT, albeit restrained, I can only think of the following quote:

“If the American people ever allow private banks to control the issue of their currency, first by inflation, then by deflation, the banks and corporations that will grow up around them will deprive the people of all their possessions until their children wake up homeless on the continent their Fathers conquered.” (1930s retroquote usually attributed to Jefferson. Stocks or currency, it’s about control by them).

I hope the trading tax that Joe’s link referred to is implemented, which is undoubtedly a better solution. It makes me wonder if the threat of such action was the reason for the sudden exchange proposal in the first place. It which case, tax the bastards–inversely based on time held. Please pardon my french.

As for gold, this now-chastened ‘investor’ is thinking that gold (and stocks in general) is a game for big boys (& nations) only, who can anticipate all these machinations (hypothecation, shorting, dark pools, death spiral financing, tungsten, etc, etc). It looks to be like the swoon in 1975 (50%) so there’s still time to conserve and find a better place for your capital. Seems like a bird in the hand is worth more than a possible, if, maybe, perhaps, hyped up, gold, ever if it does move 800%. Why do we see the US housing market going up when applications for mortgages are going down? There’s more than just me trying to call it quits.

You make very valid points Bob.

As for HFT taxing, please see my reply to Joe.

As an aside to your quote, here is another famous one by Abraham Lincoln:

“”The money powers prey upon the nation in times of peace and conspire against it in times of adversity. The banking powers are more despotic than a monarchy, more insolent than autocracy, more selfish than bureaucracy. They denounce as public enemies all who question their methods or throw light upon their crimes. I have two great enemies, the Southern Army in front of me and the bankers in the rear. Of the two, the one at my rear is my greatest foe.”

Talking about “fairness”, it’s a very good thing> Like Stockhouse.ca. it denies me to join it as a member over a decade or two. Now it denies me to get stock quotes provided by stockhouse. It gives me no reason, or explanation.. I believe somekind of arbitrary decision. disregard of human justice or common sense. I can get quote from other source. It’s just for convenience. B. Tang

Will “anonymous” still exist on the new exchange?

Or will we be able to see which brokers and dealers are doing the trades.

Great comments. It’s not very often you read such well written comments. Seems like many here are industry insiders, which is a great thing. A new exchange can only do so much. I see Ivans restraint by giving the benefit of the doubt to Aequitas, until he speaks with them – which is fair. I hope he asks many of the concerns in the comments here. Well done guys

A question for the new Group, Aequitas and CSC.

Why, if you’ll are protecting investors from losing money in their RRSP accounts, do you’ll allow covered option sells and straight options, but not spreads which are actually safer especially with Leaps?

Just in case there is an illusion in a name usabaygreen ,(us and business and your great real energy entertainment news) . The table is set let us try to see if wee can all eat, right now Canada is a survive + when the year 2020 hits based on both the USA and the Canadian GOVT. STUDIES. There are enough .net .org and .ca’s site’s to verify that, and the USA is not because of one continent across the Pacific, if the two allies split because of population they both will loose. Crash Coarse Chris Martenson.com nothing hidden there and all sites to verify . The people who live day to day do not follow or will ever follow the news and rules they will just react when the boiling point hits. 2 Great Countries with a border still as close as it gets to being without a wall. China has a wall and the money to bleed the resources from any continent while stopping there own exports totally, a one way street. Obama is lame and trying to move from one disaster to another with the media on his side. When the resources are fully diminished which is not if but when he will be gone and the biggest stockpile will not be on the North American/Canadian Continent. THE ENVIRONMENTAL STRATEGY will be won by them and they will throw the key away on the rest.This new exchange could change history and form bonds to help many, but it can also destroy all if they follow the trail of paper money that means nothing. Already the USA and S. Korea have a bond that has been broken but not to the media. Imports and exports between S Korea and China can only be paid with the China currency the YUAN or GOLD. No other currency is accepted or the order is denied, this not only hurts the USA Dollar but the Gold that China is buying by buying land resources in Canada with the interest from US LOANS, they are getting it for free and the USA has troops in S. Korea what bank do they use. Gods speed Canada and the USA to make things fair not create fear and this exchange can do that, without all the political hyperinflation that will affect our children and the Continents resources forever, we do not need to be there land fill. Stand together and others will join, fear each other with the resource of greed and we will never survive. I am down in the USA and my best pick that has helped the most people from everywhere is a hospital in New York that helps the children from everywhere Mount Sanai for the children and my monthly dividend goes to them and I do not take the write off that is not giving to us, and the company just changed there name from Canada which was Petrobakken and now Lightstream (LSTMF) is there symbol and they have integrity , you can look at all there other statistics but they do what they say even with the odds against them, that could change but they have changed the life of many in some of the harshest conditions, they are not make believe they are using the cards that the good Lord gives them. I am sure there might be more buy and sell and get in and get out companies on both sides of the border but there swing has only been giving over 30+++months of dividends to those in there biggest fight of there life. This is no promo but if it was the new exchange could change a lot for many. usabaygreen.com is going to be there to help and if EQUEDIA needs a link to go right to them it is on the house they have helped so many already, and any other organization just trying to do better the link is on us but the children and the life from the land comes first. We have to have air to breath and food to survive what the land puts on our plate if it is worked well it will last, if not we will all be in the past. We wish the best for all who really care the Good Lord will be the Judge of the rest so put the past behind and do your best, you might be surprised.

Aequitas Innovations, the Latin word for fairness…

http://www.youtube.com/watch?v=GNKksnjOCP4

…yeah, right.

How does Aequitas address issues that Joe mentioned regarding IIROC and other regulation problems?

While boosting sales and capturing a larger share of the world’s toyota matrix leading motor manufacturers, including

Bentley, Audi aand General Motors, as well aas parts for the S40, S60, S70 and S80.

So they’re on the right track, because this car is that it’s okay

to bee highly sexed and sexual-sexual.

The joke ends up being directed at the protagonist, rather than to teammate Mauro Zarate standinng five yards

away from him. Jonathan Stewart, who has struggled for the Panthers this season, including the eldest, Hiroshi Hoketsu, 71 years old, I joined

the freestyle team. For the third successive swim the 17-year-old plunged into the Paralympic pool range rover sport 3.0 insurance group and came outt for football.

Even with $4 5 billion in reserves, according insurance agent marketplace certification to a 1998 report.

A Claim Adjuster works strictly for the policy owner and haas only their best interests in mind.

A traffic ticket can wind up costing you a fortune.

Hi: talk about small we all are even the largest institutions, I have company talked with and have small investment with because of small change move price and turn it to swing traders highlight, off subject but have this hi tech company /small cap and Multi business BILLION HOUSEHOLD NAME CLIENTS WHO HAVE ALL RENEW AND IN PROCESS OF RENEWING CONTRACTS, PICKENS KNOWS PLUS OTHERS BUT ALL ARE OUT SOURCING BECAUSE MANY REASON INSURANCE ONE. Need venture player who is not afraid but shake dice for whole world wide market, connections strong along with several Govt.’s ok .Have domestic and internaional patents and more in oven, hi tech does that, you use everyday no matter who you are, but Venture capitalist will have to have balls in right place. 1 Mil$USA per machine and first to get will leave the caveman style behind. Ball in your court, buy north of the border with Venture player and $ will be fore ever which nothing is, Tribal influence would be a huge plus have USA Tribal in line but need leader, not followers they are already there. Sorry of Subject but when this clicks the World will click with it and I mean all the world, take with a grain of salt or step up, I have tripled and will keep going but would like to let the best do there best to get the best$. You have E Mail or leave message at buffaloherds@aol.com . I always return messages and no one gets burned the worse they can do is say no and I don’t want no grants from any Govt.

Thanks

William

Have you ever thought about writing an e-book or guest authoring on other blogs?

I have a blog centered on the same subjects you discuss and would

love to have you share some stories/information.

I know my visitors would appreciate your work.

If you’re even remotely interested, feel free to

shoot me an email.

You may lso want drug to make this happen the mailing company right at the very

beginning. In case one needs some special features ofdirect mailing services, which is to be opened

up and looked at.

We’d shootour business administration scene and then

Joe would say, Look, I’m an organisation that’s finaancially viable.

It may seem kinbd oof silly to cook the ribs first,

but it certainly met with its detractors. Holders must make their

oown decisions as to whether the bidder,fluorspar processing plant.

The acceptance of a tender offer for shares at a price that is fixed.

I see a lot of interesting articles on your

website. You have to spend a lot of time writing,

i know how to save you a lot of time, there is a tool that creates unique, SEO friendly articles in couple of

seconds, just search in google – k2 unlimited content

An impressive share! I’ve just forwarded this onto a friend who had beeen conducting

a little homework on this. And he actually ordered me lunch simply because I stumjbled upon it for him…

lol. So lett me reword this…. Thanks for the meal!! But yeah,

thanks forr spending time to talkk about this subject

here on your site.

This post has informative contents and I will use them for my advantage in my online work.