There’s a strange thing that happens at the top of every great boom.

The crowd watches the fireworks, but the smart money is watching the fuse.

Right now, the entire investing world is mesmerized by the fireworks: artificial intelligence, data centers, the race to build the most powerful models ever conceived.

The headlines scream about SpaceX, Nvidia, about OpenAI, about a coming age of machine intelligence that will rewrite the global economy.

Trillions of dollars in market value have been created on the promise of it all.

And we don’t doubt the promise. AI is real and so is the buildout. And the hundreds of billions being poured into data centers is very, very real.

But here’s the question almost no one is asking: What’s required for all of this to work?

Strip away the software, the hype, and the stock charts, and you’re left with something far more primitive: something that comes out of the ground and that you can hold in your hand.

Yes, I am talking about the raw resources.

You can’t build a data center without copper, nor build a missile guidance system without rare earths. You can’t make a semiconductor without gallium and germanium, nor manufacture the ammunition to defend any of it without antimony.

There is no AI revolution, no energy transition, no modern military, no space exploration, without a steady, secure supply of critical minerals.

And that supply is anything but secure.

This is the part of the story the mainstream media keeps burying beneath the AI noise.

It’s the part institutions — the BlackRocks, the BHPs, the sovereign wealth funds, and now even the U.S. government itself — are positioning around with a quiet urgency we haven’t seen in decades.

This isn’t a story about technology. It’s a story about who controls the inputs to technology.

Because these inputs are what create power, leverage, and national survival.

And critical minerals are the foundation of it all.

Above All Else

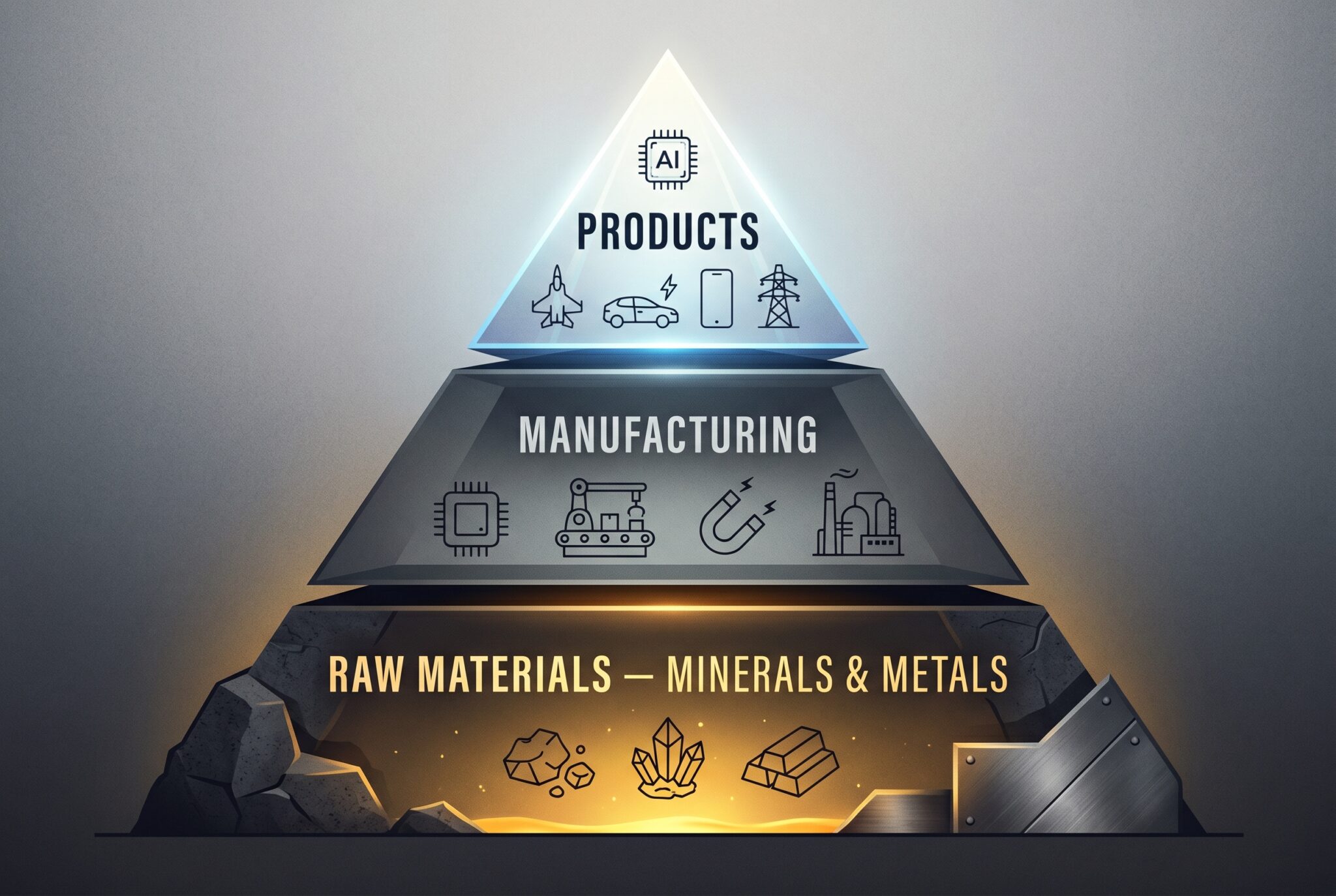

Think of the modern economy as a pyramid.

At the very top, where all the attention goes, sits the glamorous stuff: the AI models, the fighter jets, the electric vehicles, the smartphones, the power grids.

Beneath that sits the manufacturing: the fabs, the assembly lines, the magnet plants, the refineries.

And beneath that, holding the entire structure up, sits a layer most investors never think about: the raw materials. The minerals and metals that everything else is built from.

Remove the top of the pyramid, and you lose a product. But remove the bottom, and the entire thing collapses.

No one has articulated this more sharply than the man currently building rockets, satellites, and one of the largest AI compute clusters on earth. When Elon Musk was first trying to understand why rockets cost so much, he reasoned it down to first principles and arrived at an observation that should be ingrained in your brain.

Via Smithsonian magazine, recounting Musk’s reasoning:

“Obviously, the lowest cost you can make anything for is the spot value of the material constituents.”

Musk was saying that even with a magic wand — even if you could rearrange the atoms perfectly, with zero waste and flawless engineering — the floor on what anything can cost is the value of the raw materials inside it. Everything above that floor is just the question of how efficiently you turn raw material into a finished shape.

Flip that logic around, and you arrive at the entire thesis of this letter.

No matter how brilliant the engineering, no matter which company wins, no matter how good the software, design, or execution, none of it is possible without access to the material constituents in the first place.

Could you replace Musk, Zuckerberg, and Altman to run these companies? Probably. But you definitely cannot replace the atoms.

That is why critical minerals, such as tungsten, sit at the very bottom of the pyramid, holding everything else up.

And it leads to a conclusion that almost no one in the market is willing to say out loud: if you are going to invest in any of today’s booming sectors, such as AI, data centers, space exploration, defense, the most foundational, durable, can’t-be-engineered-around thesis isn’t the sector itself.

It’s the materials that the sector cannot exist without.

Here’s what makes critical minerals different from almost any other asset class on earth: they are non-substitutable, geologically concentrated, and increasingly controlled by governments rather than markets.

You can’t print them, nor can you can’t code your way around them.

You can’t simply “innovate” a replacement for a material whose properties are dictated by physics.

And, this is the crucial part: you can’t pull them out of the ground overnight. A new mine can take 10 to 20 years to move from discovery to production, once permitting, financing, and construction are factored in.

That combination of irreplaceable, scarce, slow to produce, and politically weaponizable is the most foundational setup an investor should consider.

It’s the kind of setup that the U.S. Geological Survey has been warning about for years.

The USGS now maintains a formal list of 50 critical minerals — everything from antimony and gallium to the rare earth elements, cobalt, graphite, lithium, and tungsten — defined as materials essential to the economy and national security whose supply chains are vulnerable to disruption.

Vulnerable is putting it gently.

Because one nation figured out the importance of this bottom layer of the pyramid long before anyone else. And it has spent the last two decades quietly building a stranglehold on it.

Domination

Let’s talk about the elephant in the room. Or rather, the dragon.

China does not merely participate in the critical minerals market. China is the critical minerals market.

According to the International Energy Agency’s most recent analysis, China dominates global output across nearly every strategic material that matters. It supplies roughly 70% of the world’s rare earth production and controls around 90% of global rare earth ore processing. It also produces the overwhelming majority of the world’s semiconductor metals: gallium and germanium. It also dominates graphite, magnesium, tungsten, and bismuth.

Add in refining, and the chokehold truly tightens.

China controls processing capacity that makes the rest of the world look like a rounding error.

By various estimates, roughly 57% of the world’s lithium, 77% of its cobalt, more than 90% of its rare earths, and over 90% of its natural graphite are refined within China’s borders.

In other words, it doesn’t matter where the rock comes out of the ground. If it has to be refined in China to become usable, then China holds the cards.

Why does this matter so much? Because of what these minerals actually do.

If you want advanced AI and the data centers to run it, you need them.

Want semiconductors? You need gallium and germanium.

Want electric vehicles and grid-scale batteries? You need lithium, cobalt, graphite, and nickel.

Want a modern military with fighter jets, submarines, precision-guided munitions, night-vision, and radar? You need rare earth magnets, tungsten, and antimony.

There is no version of the 21st-century economy that doesn’t run directly through this handful of elements.

And right now, China controls the supply.

For years, this was treated as a supply-chain efficiency story. Cheap Chinese processing kept costs down, so the West happily offshored the dirty, low-margin work of digging and refining while keeping the glamorous, high-margin work of design and assembly.

In other words, the West was busy building the top of the pyramid. It was clever at the time, but it has turned out to be one of the most dangerous strategic blunders in modern economic history.

Because a chokehold is only an inconvenience until the day someone decides to squeeze.

Squeeze Time

That day has arrived.

In August 2024, China added antimony to its export control list — a metal most people have never heard of, but one that is irreplaceable in ammunition, flame retardants, night-vision equipment, and military-grade alloys.

In December 2024, China restricted exports of gallium, germanium, and antimony specifically to the United States — three minerals central to semiconductor production and defense applications.

In April 2025, China escalated dramatically, imposing export controls on seven heavy rare earth elements and related magnets — not just against the U.S., but against the entire world. The effect was immediate and brutal. According to the IEA, export volumes collapsed in April and May, and carmakers in the United States, Europe, and elsewhere struggled to obtain permanent magnets. Some were forced to cut production. Some temporarily shut factories down. Even after volumes recovered, rare earth prices outside China stayed elevated — at one point, European prices reached up to six times those inside China.

In October 2025, Beijing went further still, announcing sweeping new controls that for the first time reached across borders. The new rules required foreign companies to obtain a license from China to export products made outside China if those products contained Chinese-origin rare earth materials or were produced using Chinese technology. Economists at the European Central Bank estimated that over 80% of large European firms sit no more than three intermediaries away from a Chinese rare earth producer. With one regulatory stroke, Beijing had asserted authority over a vast swath of the global manufacturing base.

Now, here’s where it gets interesting.

Via the International Energy Agency’s Global Critical Minerals Outlook 2025:

“…more than half of a broader group of energy-related minerals are subject to some form of export controls.”

And those restrictions are, “expanding in scope to cover not just raw and refined materials but also processing technologies.”

If that dynamic sounds familiar, it should. It’s the mineral world’s version of the chokehold that already exists in semiconductors.

Today, virtually every advanced chip on earth depends on two irreplaceable bottlenecks: Taiwan’s TSMC, which manufactures over 90% of the world’s most advanced chips (5nm and below), and the Netherlands’ ASML, the only company on the planet that makes the EUV lithography machines required to print them — machines involved in the production of roughly 99% of all semiconductors. Whoever controls those two nodes controls the entire chip economy downstream of them.

Critical minerals are the same story, but one layer deeper: China is the TSMC and the ASML of the materials world, the indispensable chokepoint that everything above it relies on — including the real TSMC and ASML.

Now, in November 2025, as part of a de-escalation package following a meeting between the two nations’ leaders, China announced it would suspend the October measures for one year, until November 2026, and pause the dual-use restrictions on gallium, germanium, and antimony to the United States.

While the market took a sigh of relief and the headlines declared the crisis over, it is anything but that.

One look closely at what was actually suspended and what wasn’t, and you’ll see the truth.

The April 2025 controls and the entire licensing architecture remained fully intact. And critically, the restrictions on military end-users stayed firmly in place. As analysts at the Center for Strategic and International Studies documented, under rules taking effect December 1, 2025, companies with any affiliation to foreign militaries — explicitly including those of the United States — would be largely denied export licenses.

So a civilian carmaker could once again buy gallium, but the Pentagon is still locked out.

By early 2026, Beijing had even begun redirecting elements of this framework toward Japan, prohibiting exports to Japanese military users.

So, China didn’t dismantle the weapon; it simply put the safety back on…for one year.

As one analysis aptly put it, China’s export controls are like a “one-shot bazooka”: devastatingly powerful, but with a catch. Fire it too often, and you teach your enemies to build their own. Beijing knows this, so it has chosen to calibrate — to tighten and loosen the valve as a flexible instrument of statecraft, keeping the entire system in place while modulating exactly who feels the pressure and when.

As we mentioned in a previous newsletter, there is now a countdown clock ticking toward late November 2026, when the current suspension is scheduled to lapse.

The entire industrial world is watching it, while the smart money is using this fragile, temporary reprieve to do one thing as fast as humanly possible: build supply that China cannot touch.

National Security Windfall

For a long time, the United States treated its mineral dependence the way a frog treats slowly warming water: comfortable and unbothered…until it boils to death.

But that era is over, and the speed of Washington’s reversal has been staggering.

On January 20, 2025, the administration signed the Unleashing American Energy executive order, which included a mandate to ensure the National Defense Stockpile could provide a robust supply of critical minerals in the event of a future shortfall.

In March 2025, a further executive order demanded swift action to ramp up domestic mineral production — a direct response to the dependence that China had just exposed.

Then came the money.

In April 2025, Congress passed sweeping legislation allocating roughly $7.5 billion for critical minerals, including $2 billion to expand the national stockpile. Through its Export-Import Bank, the U.S. has issued, by recent count, nearly $15 billion in Letters of Interest for critical minerals projects — including a headline $10 billion “Project Vault” initiative to establish a U.S. Strategic Critical Minerals Reserve.

But the single most revealing move came from the Pentagon itself.

In July 2025, the Department of Defense announced a transformational partnership with MP Materials, the operator of the only operating rare earth mine in the United States, at Mountain Pass, California. The DoD agreed to buy $400 million of convertible preferred stock plus warrants — a stake that, fully exercised, would represent roughly 15% of the company, making the U.S. government MP’s largest shareholder.

Stop and absorb how extraordinary that is.

The federal government did not simply issue a grant or offer a loan guarantee; it bought equity, becoming the single biggest owner of a publicly traded mining company.

This was the first time the U.S. government had become a major shareholder in a critical minerals company.

And Pentagon officials made clear it would not be the last.

But the deal didn’t just stop at equity.

The DoD committed to purchasing the entire output of a new magnet facility for ten years!

It set a price floor of $110 per kilogram for neodymium-praseodymium oxide — nearly double the prevailing Chinese market price at the time — guaranteeing a profitable market regardless of what Beijing does with pricing. Meanwhile, two of the largest banks in the world, JPMorgan and Goldman Sachs, committed a billion dollars in construction financing alongside it.

As a result, MP Materials’ stock surged roughly 50% in a single day, adding about $2.5 billion in market capitalization in one trading day. MP’s CEO, James Litinsky, framed the deal as a blueprint for the future.

Via CNBC, quoting Litinsky:

“I’d like to think that this is sort of the first, it’s a model.”

In other words, expect more of these deals to come.

By early February 2026, the State Department convened a Critical Minerals Ministerial with representatives from 54 countries and the European Commission — described by one Council on Foreign Relations fellow as among the most ambitious multilateral gatherings the administration had attempted. There, Vice President JD Vance unveiled a plan to bind allies into a preferential trade bloc with coordinated price floors.

Via Yahoo Finance, quoting Vance:

“These reference prices will operate as a floor maintained through adjustable tariffs to uphold pricing integrity.”

Interior Secretary Doug Burgum put the stakes in even simpler terms.

Via Quest Metals’ summary of his remarks at the ministerial, quoting Burgum:

“These minerals go into everything from missiles to AI accelerators.”

But it was Secretary of State Marco Rubio who captured the entire thesis of this letter in a single breath — explaining exactly why the West got into this mess.

Via The Hilltop, quoting Rubio:

“We fell in love with the design of these things. But forgot that to design something, you have to be able to build it, and to build it, you have to have the fundamental materials to make it.”

That is the whole game, stated by America’s top diplomat.

This is exactly what Elon’s first principle theory on manufacturing is saying: the design is downstream, while the materials are upstream. And whoever controls the upstream controls everything below it.

Read between the lines.

When the most powerful government on earth starts buying equity stakes in miners, guaranteeing price floors, building strategic reserves, and signing supply treaties with dozens of nations at once, it is telling you, in the loudest possible terms, where it sees the next great vulnerability.

And where there is vulnerability at the national level, there is opportunity at the investment level.

Nationalization of Critical Minerals

Here’s what makes this moment genuinely different from past commodity cycles: it isn’t just China and the United States.

The entire world has suddenly realized that whoever controls the rock controls the future.

And nations everywhere are moving to lock down their own.

This is the part of the story that transforms a supply concern into a structural, multi-year repricing of an entire asset class.

Consider what’s happened in just the last couple of years…

Indonesia banned the export of unprocessed nickel, forcing manufacturers to build processing inside its borders. And in doing so, reshaped the entire global nickel market.

Zimbabwe imposed export bans on unprocessed lithium for the same reason: to force value-added processing to happen at home rather than shipping raw ore abroad.

The Democratic Republic of the Congo — which produces the majority of the world’s cobalt — imposed an outright export ban on cobalt in February 2025. When it lifted that ban in October, it kept a quota in place. And by early 2026, the DRC was moving to stockpile its own critical minerals, transforming itself from a passive supplier into an active manager of global supply and price.

Mali’s government revoked more than 90 mining exploration permits in a single decree, covering gold, iron ore, bauxite, uranium, and rare earths — releasing the ground for reallocation and asserting state control over strategic assets. Neighboring Guinea annulled licenses in a parallel push.

Each of these moves, on its own, might look like a local political event. Together, they form an unmistakable pattern: resource nationalism is back, and it is accelerating.

Every export ban tightens global supply, and every license revocation makes existing, secure assets more valuable. Every quota and every processing mandate pulls more of the value chain behind a national border. The pool of mineral assets that a Western manufacturer or a Western government can actually rely on is shrinking — even as demand explodes.

In other words, the best place to be for miners right now is in the country that has the most money, resources, and power: the United States.

And nowhere does that vulnerability come into sharper focus than with a single, unglamorous, grayish-white metal that almost no one outside the defense and semiconductor industries has ever thought about.

The Hardest Metal in the Room

If you wanted to design the perfect critical mineral — the one with the most dangerous combination of irreplaceability, military necessity, and supply concentration — you would end up describing tungsten.

Why? Well, let’s start with the physics.

Tungsten has the highest melting point of any metal on the periodic table at a staggering 3,422°C, along with extraordinary density and a hardness, in its carbide form, that approaches diamond.

In other words, they are the reason tungsten cannot be swapped out for something cheaper or more abundant. When you need a material that won’t deform under extreme heat, won’t wear down under extreme stress, and won’t yield under extreme force, there is frequently no substitute.

As Elon puts it, physics doesn’t negotiate.

That unsubstitutability is exactly why tungsten sits at the heart of the things that matter most in the 21st century: defense, semiconductors, AI hardware, and space.

Tungsten in the Military

This is where tungsten is most irreplaceable and most strategically sensitive. Its density and hardness make it the metal of choice for armor-piercing munitions, artillery shells, tank armor, and kinetic-energy penetrators. Meanwhile, its heat resistance makes it essential for rocket and missile components. As Western defense planners are now painfully aware, you cannot build a modern arsenal without it, and roughly 90% of the raw materials needed for munitions and armor production effectively run through China, Russia, or North Korea. Just ask NATO when it published a list of twelve defense-critical raw materials in December 2024, forming the backbone of military hardware. Yes, tungsten was on it.

Tungsten in Semiconductors and AI

For roughly the last 25 years, tungsten has been the primary metal used for the microscopic interconnections inside chips— the ultra-thin films, deposited via tungsten hexafluoride in a chemical vapor deposition process, that wire transistors together and fill the contacts inside a processor. Tungsten’s high melting point and stability mean those interconnects survive the extreme current and heat of a working chip, allowing manufacturers to build denser, more powerful processors. As AI pushes silicon to run hotter and harder than ever before, that thermal and electrical stability becomes more valuable, not less. Tungsten wire is also used to slice the silicon ingots into wafers in the first place.

Via Western tungsten producer Almonty Industries, framing the stakes:

“AI sees silicon chips run hotter and work harder than anything before them — and tungsten is the hidden metal making it possible.”

In other words, the metal is embedded at multiple points in the very chips that power the entire artificial-intelligence revolution.

Tungsten in Space

The same property that makes tungsten essential for missiles — its ability to hold its structure at temperatures that would liquefy almost anything else — makes it critical for spaceflight. Rocket nozzles, throat inserts, reaction-control components, and other parts that must survive the searing heat of propulsion rely on tungsten and its alloys. As the new space race accelerates — commercial launch, satellite constellations, and even early experiments in orbital semiconductor manufacturing — the demand for heat-tolerant materials like tungsten climbs alongside it.

A Near-Monopoly

Now here is where it gets uncomfortable.

According to the U.S. Geological Survey’s most recent Mineral Commodity Summaries, global tungsten mine production was roughly 82,000 metric tons in 2024, estimated at around 85,000 tons for 2025. Of that, China alone produced about 67,000 tons, representing over 80% of the entire world’s supply.

The USGS puts China’s share of global mine production above 80%, and China also holds the largest reserves on earth, roughly 2.4 to 2.5 million tons out of a global total around 4.7 million.

Production outside China from countries like Vietnam, Bolivia, Russia, North Korea, Austria, Spain, Portugal, and Rwanda collectively accounts for only around 20% of the world’s supply, and much of that has historically been processed in China.

And the United States?

A big ZERO.

In fact, the U.S. has not commercially mined tungsten since 2015!

According to the USGS, U.S. net import reliance for tungsten runs above 50%, and a meaningful share of historical imports traced back, directly or indirectly, to China. A nation that depends on tungsten for its entire defense industrial base produces none of it from its own mines.

The Squeeze Arrives…Again

You can probably guess what happened next because it follows the exact same script as antimony and rare earths.

On February 4, 2025 — reportedly within minutes of new U.S. tariffs taking effect — China announced export controls on tungsten, along with tellurium, bismuth, indium, and molybdenum, requiring licenses to export some 20 related products in the name of “national security.” China classifies tungsten as a dual-use material, reflecting its role in both civilian and military supply chains.

The effect on supply was immediate and deliberate.

Chinese tungsten exports fell sharply in 2025, down roughly 14% in the first nine months of the year versus 2024, by some measures down more than 20% in the first half, despite stable global demand. Customs data showed the United States imported essentially no ammonium paratungstate (the key intermediate chemical) from China during parts of this period.

And guess what? Prices responded accordingly: benchmark APT prices jumped sharply through 2025, with European APT reportedly up over 40% in the first half of the year alone, and the broader tungsten market climbing from roughly $6 billion in 2024 toward double-digit-billion projections later this decade.

Like the other minerals, tungsten was swept into the November 2025 U.S.–China de-escalation, which paused some of the dual-use controls. But the underlying licensing architecture stayed fully intact, and the military-end-user restrictions did not go away.

But that’s not all.

The Trillion-Dollar Time Bomb

Buried in the National Defense Authorization Act, and implemented through the Defense Federal Acquisition Regulation Supplement (DFARS), is a hard legal deadline. Beginning January 1, 2027, U.S. defense contractors are barred from delivering covered materials sourced from a “covered country.”

That means China, Russia, Iran, or North Korea.

Via the DFARS clause language, as reported by Fastmarkets,

“…(contractors) shall not deliver under this contract any covered material mined, refined, separated, melted, or produced in any covered country, or any end item, manufactured in any covered country, that contains a covered material.”

Those covered materials explicitly include tungsten metal powder and tungsten heavy alloy, along with samarium-cobalt and neodymium-iron-boron magnets and tantalum.

Think about what that means.

The vast majority of the world’s tungsten comes from precisely those covered countries. Yet starting in 2027, none of it can legally flow into U.S. defense contracts. The underlying rule, analyzed by law firm Crowell & Moring, stems from successive National Defense Authorization Acts (Section 871 of the FY19 NDAA and Section 854 of the FY24 NDAA).

Industry commentary has pegged the value of outstanding and ongoing U.S. defense contracts that touch tungsten and these covered materials at on the order of nearly one trillion dollars — an enormous web of weapons programs, from aircraft to munitions to armor, that will need to certify a clean, non-Chinese tungsten supply chain or risk contract termination.

With commitments of roughly a trillion dollars of defense work, how will these contracts be fulfilled if the production of them requires tungsten that the United States does not currently mine, from a Western supply base that barely exists, in a market where one rival nation controls more than 80% of global output and can throttle exports at will?

This isn’t just a market inefficiency; it’s a national-security cliff with a date attached.

And the U.S. government knows it.

The Defense Logistics Agency has been actively stockpiling tungsten, while the Pentagon has signaled tungsten among its critical mineral spending priorities.

In October 2025, a U.S.–Kazakhstan joint venture to develop tungsten resources was announced as Washington moved to “cut in line” ahead of China for major untapped deposits abroad. New Western-aligned production is being raced toward commissioning with projects like the Sangdong mine in South Korea (expected to supply a large share of non-China tungsten at full capacity) and early-stage efforts to re-establish tungsten mining and processing on U.S. soil.

But these take years to ramp, and the 2027 deadline is closing fast.

That gap, between an ironclad legal mandate on one side and a near-total absence of compliant supply on the other, is the kind of structural imbalance that defines a generational opportunity.

When a trillion dollars of defense spending is legally forced toward a supply base that doesn’t yet exist, the few credible non-Chinese tungsten assets in the world become extraordinarily valuable.

And tungsten is just one mineral.

The same dynamic — irreplaceable function, concentrated supply, government mandate, structural deficit — is playing out across the entire critical-minerals complex at once.

Which brings us to the demand side of the equation, and the force that is about to make all of it dramatically worse.

The AI Fuel

Every data center being built to train and run AI models is a voracious consumer of physical materials.

The copper alone is staggering — the wiring, the busbars, the transformers, the grid connections required to feed these power-hungry facilities represent one of the largest sustained pulls on copper demand in history. The chips inside need gallium and germanium. The backup power, the cooling, the grid buildout — all of it rests on the same scarce materials that are now being weaponized and hoarded by governments around the world.

So you have a once-in-a-generation demand shock from AI and electrification crashing headlong into a once-in-a-generation supply shock from resource nationalism and export controls.

In any other market, that is the textbook recipe for a violent, sustained repricing.

And we are already seeing it in the numbers.

Antimony is the clearest example. This obscure metal — one that the U.S. produced exactly zero tonnes of from domestic mines in recent years — saw its price rocket from around $12,000 per tonne to over $60,000 per tonne by early 2026. That’s a fivefold increase.

A Govini supply-chain analysis found that antimony, gallium, germanium, tungsten, and tellurium appear in more than 80,000 individual weapons parts across roughly 1,900 weapon systems — meaning nearly 78% of all U.S. Department of Defense weapon systems are potentially exposed to Chinese export controls on just those five minerals.

The Value of “Made in America”

If you follow the logic all the way down, you arrive at an inescapable conclusion — the same one the Pentagon, BlackRock, JPMorgan, and the sovereign wealth funds have already arrived at: The most valuable mineral assets in the world are the ones located in the right place.

A world-class deposit sitting in a jurisdiction that can ban exports tomorrow, revoke your license next year, or nationalize your project on a whim is a liability dressed up as an asset. A more modest deposit sitting on secure, friendly, domestic ground — particularly inside the United States — is suddenly worth a fortune, because it is something money increasingly cannot buy: reliability.

This is the great repricing that’s underway right now, and it’s why the institutions are scrambling.

Take Perpetua Resources, which spent nearly a decade grinding through permitting for its Stibnite gold-antimony project in Idaho — home to the largest known antimony deposit in the United States and viewed currently as the only viable domestic source of the metal – with the exception of THIS company, who is on track to possibly be the first antimony producer in the US.

As the antimony crisis exploded and the project secured its final federal approvals, the stock went from under C$4 to over $20 — a five-bagger — and its market capitalization swelled past the billion-dollar mark. The Department of Defense recognized the project’s strategic value and provided funding to help fast-track it, while the Export-Import Bank of the United States (EXIM) recently unanimously approved a $2.9 billion loan to it under the Make More in America Initiative (MMIA).

In the nearly 20 years of this Letter’s existence and successful mining company profiles, we have never seen a situation in which the target for success has been so apparent.

Strong U.S. critical mineral projects represent one of the clearest paths to value creation in the mining sector, combining resource quality, geopolitical relevance, and significant government-backed de-risking.

The investment case is simple: own scarce critical mineral resources in jurisdictions where governments are actively incentivizing domestic production and securing supply chains.

That is the template. And there will be more.

The problem? There are very few of these assets…

Diamond in the Rough

America spent two decades letting its mining and processing base wither. You cannot conjure a new antimony or tungsten mine, a new gallium refinery, or a new rare earth separation facility out of thin air. The handful of credible domestic projects that exist are, by definition, scarce — and scarcity, in a market this hungry, is where fortunes are made.

The big money already knows this.

Jamie Dimon, the head of the largest bank in America, made the point bluntly at the Reagan National Economic Forum in late May 2025.

Via Fox News, quoting Dimon:

“We shouldn’t be stockpiling bitcoins, we should stockpiling guns, bullets, tanks, planes, drones, you know, rare earths.”

He added, via the same Fox News report:

“We know we need to do it. It’s not a mystery.”

BHP, BlackRock, and Gulf sovereign wealth funds have all been maneuvering for critical-mineral exposure. The institutions are not waiting for the news to make it obvious, and are already positioning ahead of it.

And this torrent of capital has very few places to go.

And that is precisely the imbalance that creates opportunity for those who move early.

The Next Play

We’ve been doing this a long time, and we’ve learned to recognize the difference between a fad and a fault line, and between good mining companies and bad.

A fad is loud, crowded, and obvious – overly promoted mining stocks without great assets. By the time it reaches the front page, the easy money is gone.

A fault line is quiet. It builds pressure for years beneath the surface while the crowd looks elsewhere — and then it releases all at once, redrawing the entire landscape and rewarding the handful of people who were paying attention.

This is why we will be intensely focused on this space.

Not because it’s the trendy story. In fact, it isn’t; the trendy story is still AI and chatbots. But because it sits underneath the trendy story, holding it up.

Because the most powerful institutions on earth, and the U.S. government itself, are pouring capital into it with a sense of urgency that only comes when national survival is on the line. And because, unlike the fireworks at the top of the pyramid, this opportunity is still largely hidden in plain sight.

We’ll be hunting for the assets that matter most in this new era: secure, domestic or allied-jurisdiction critical-mineral projects — antimony, rare earths, gallium, germanium, copper, tungsten, and the rest — that stand to benefit from government price floors, offtake guarantees, strategic stockpiling, and a structural supply deficit that won’t be resolved for years.

We’ll be looking for the early-stage explorers and developers that could become the next Perpetua, the next Mountain Pass — companies sitting on the right rock, in the right place, at exactly the right moment.

But we urge caution: just because you have some decent drill results in the United States, it doesn’t mean you will be successful. To get ANY interest from the US government or the big institutions, you still have to have a rare project with great geology, or be one of the biggest (size matters when the big boys want to invest and loan out billions).

Conclusion

You can’t have an AI future without the materials to build it, nor defend a nation without the metals to arm it. You can’t run a data center, a power grid, or a fighter jet on enthusiasm.

Remember Musk’s first principle: the lowest cost anything can ever reach is the spot value of its material constituents.

Strip away the hype from every sector the market is chasing right now, and what you’re left with — the irreducible floor beneath all of it — is the rock. Whoever controls the rock controls the ceiling on everything built from it.

Everyone is talking about who will build the most powerful AI, but almost no one is talking about who controls the inputs that make ANY of it possible.

That silence is the opportunity.

The fuse is lit, and the institutions can already see it. The question is whether you’ll be positioned before the rest of the crowd finally looks down from the fireworks, and realizes what’s been holding everything up all along. We intend to be.

And we’ll be looking aggressively to bring you the best ideas in the months ahead, in a space where we have had numerous successes.

Seek the truth.

Carlisle Kane

Thank you- this is extremely good intel