For the full interactive edition, please CLICK HERE

Investors have once again been duped.

Gold fell last week, while stocks rose.

The S&P 500 ended its best week in 2012. The strong gains came after the benchmark index fell more than 6 percent in May and dropped just below its 200-day moving average.

But why in the world is the stock market rising?

Was it the possible thought of QE?

Nope. Bernanke denied us of any immediate spending – yet the market continued to climb.

Was it the encouraging report that U.S. wholesale stockpiles grew twice as fast as they grew in March, signalling that businesses are ordering enough goods to lead to increased factory production and sales?

Nope. Stockpile growth largely depends on the spending habits of U.S. consumers and businesses. With little to no job creation and payrolls rising slower than the rate of inflation, where is the spending coming from?

(I suspect that it’s coming from savings and further loose credit. That means it’s all an unsustainable one-time increase. Yes, oil and gas prices have dropped but still remain high. Spending is not coming from income. That’s what is really scary behind the GDP numbers. More QE? Coming right up…)

Was it China’s central bank announcing a surprise interest rate cut?

Nope. Because that means China’s economy is slowing down. It was China’s first rate cut since the 2008 crisis which means the world’s economic engine may be preparing to announce some very weak data. Analysts are already forecasting China would deliver its weakest quarter of growth in three years in the second quarter at 7.9pc – the sixth straight quarter of slowing growth. They expected 2012 full-year expansion of 8.2pc, the weakest outcome for China since 1999.

So why in the heck is the market rising?

In March, I explained that stocks have been rising on historically low volumes:

“The one biggest concern scaring investors is the volume in trades that has been pushing the market higher. Trading at the New York Stock Exchange declined to the lowest level since 1999 last month, with the average volume over the 50 days ending Jan. 25 slowing to 838.4 million shares. The value of stocks changing hands dropped to $24.9 billion, a 50-day average not seen since at least 2005.”

When stocks rise on low volume, its fall could be disastrous.

While stocks had one of its best weeks, it also had one of its lowest volume weeks of the year. If that signals to you that the markets are moving back up on a new bull leg, you need to think twice.

It may sound shocking to you, but the rise in stocks and the downfall in gold was yet another clear shot of market manipulation by the powers running America. There are no buyers right now. So forget all the talk about a new bull leg.

There isn’t one.

It’s only a matter of time before everyone realises the market can only be propped up for so long. Stimulus can, and will, only ease the minds of investors for a brief period before it becomes mundane. And after one more round of QE, people will finally come to the realisation that their dollars and their currencies are losing value at an astonishing pace. That’s why the Fed will wait until last minute to unleash its paper force.

A Giant Credit Bubble

The world is in one giant credit bubble sustained only by more credit.

Just ask your friends, your neighbours, your families, and your coworkers. I bet they all owe a lot of money – and not just money for their overpriced Canadian homes they were able to buy because of historically low interest rates, despite record high prices.

Most of these debts will never be repaid and yet more debt and credit will flow. But don’t stress yourself thinking you’re the only one. The governments of the world are loaded with even more debt that will NEVER be repaid. It used to be millions. Then it turned into billions. And now sovereign debt is figured in the trillions.

How are these debts being repaid? With more debt…

What Does That Mean?

There’s nothing we can do to fix the world’s financial crisis. It will get a lot worse before it gets better.

There are only two likely simplified scenarios:

- We continue to print more money and inflate the heck out of all fiat currencies.

- We move to some sort of a gold standard.

The likelihood of scenario two is highly unlikely given that the world is still, and will continue to be, controlled by politicians and bankers.

In both scenarios gold prices will move up, as it has done without question in the past century. Citizens will soon realise that wealth is not something you can print. As a result they’ll begin to hoard their gold, land, and other real tangible assets.

Every fiat currency since the Romans first began the practice in the first century has not only ended in devaluation but eventually in collapse. Not only did currencies fail, but the economies that housed them failed as well.

Is our modern civilization on the same path?

If you compare the fall of previous fiat currencies, they all have a similar cycle and consequence. In almost every case, so much money was printed that they became useless and lost nearly all of their value as serious inflation took over.

The fall of civilizations, economies, and currencies don’t happen overnight. Some of these currencies failed within years, some within decades, and some within a century. While the US implemented fiat currency since the late 1800’s, its current currency issued by the Fed (and no longer by the US) is just over 40 years old. How much longer do you think it will last?

While it may seem farfetched today, this point of failing fiat currencies will eventually make sense.

We’re already seeing this in gold’s slow and steady rise over the last ten years, right alongside our monetary base.

Slowly, but surely, gold will continue to rise. There will be a point where gold will show its force and turn speculative. While gold has been shunned by the mainstream media, psychology will reverse and everyone will be rushing to own gold. It’s the only form of money that has been rising steadily for the last few hundred years. Can you say the same about the dollars in your wallet? Will it take another 100 years before people realise that the only thing fiat currencies do is lose value over time? The only thing gold has done over time is gain more value…

No wonder China continued to buy more gold in April, importing another 100 tons of physical gold. In the first four months of 2012 Chinese purchases have already increased by an unprecedented 782% over 2011.

The Chinese are the only ones with real money to spend. With the highest savings rate in the world, they are spending their money on gold and silver. I wouldn’t even call it spending; I would call it saving or preserving wealth.

The Chinese have the strongest purchasing power and a labour shortage while America is a country riddled with debt and unemployment. Which side would you prefer?

Walking on a Tightrope

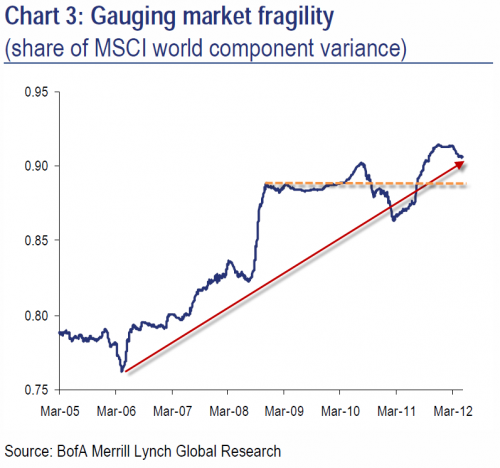

While QE and additional world stimulus packages have alleviated pressures for the time being, the truth is quietly lurking behind the scenes. Take a look at this chart from BofA Meryll Lynch’s Global Research:

In the last year or so market fragility has soared, signaling even higher systemic risks than in the peak pre-Lehman era in 2008. The credit markets are clearly telling us that there is serious risk on the table.

Even after spending trillions of dollars, systematic risks across the board are just as high as they have ever been. Spain still needs a bailout. Greece is finished. Europe remains a mess. And Americans aren’t the economic powerhouse they need to be.

If we adjust for inflation, the real economy is actually in a contractionary state. We’re 3 years into a recovery and we’re growing at an anemic 1.88% rate while the per-capita income continues to shrink.

I had mentioned last week that we may see a bounce from the week prior:

“The stock market could bounce from Friday’s low, but that won’t signal we’re in the clear. The real short term bottom would only be found if indeed another round of QE is announced, or the Greek mess is resolved. And I stress that it would be a near term bottom.”

My thoughts haven’t changed. Politicians are only delaying the inevitable.

I don’t see a pretty week ahead. Let’s see what Spain does first.

Until next week,

Ivan Lo

Equedia Weekly

Disclosure: I am long gold and silver through ETF’s and bullion, as well as long both major and junior gold and silver companies – which means I am biased towards the sector. You can do the math. It’s your money to invest and we don’t share in your profits or your losses, so please take responsibility for doing your own due diligence. Remember, past performance is not indicative of future performance. Just because many of the companies in our previous Equedia Reports have done well, doesn’t mean they all will.

Disclaimer and Disclosure

Equedia.com & Equedia Network Corporation bears no liability for losses and/or damages arising from the use of this newsletter or any third party content provided herein. Equedia.com is an online financial newsletter owned by Equedia Network Corporation. We are focused on researching small-cap and large-cap public companies. Our past performance does not guarantee future results. Information in this report has been obtained from sources considered to be reliable, but we do not guarantee that it is accurate or complete. This material is not an offer to sell or a solicitation of an offer to buy any securities or commodities.

Furthermore, to keep our reports and newsletters FREE, from time to time we may publish paid advertisements from third parties and sponsored companies. We are also compensated to perform research on specific companies and often act as consultants to many of the companies mentioned in this letter and on our website at equedia.com. We also make direct investments into many of these companies and own shares and/or options in them. Companies do pay us to advertise on our website and we often distribute our reports on featured companies. While we are never paid to write a rosy and positive report on any company, we do market our reports using the advertising fees paid for by our featured companies.

This process allows us to continue publishing high-quality investment ideas at no cost to you whatsoever. Our revenue is generated by sponsor companies and we grow our readership by using the advertising fees we charge to distribute our reports. This helps both Equedia and our client companies gain exposure and allows us to provide you with our research at no cost.

Therefore, information should not be construed as unbiased. Each contract varies in duration, services performed and compensation received.

If you ever have any questions or concerns about our business or publications, we encourage you to contact us at the email or phone number below. Equedia.com is not responsible for any claims made by any of the mentioned companies or third party content providers. You should independently investigate and fully understand all risks before investing. We are not a registered broker-dealer or financial advisor. Before investing in any securities, you should consult with your financial advisor and a registered broker-dealer. The information and data in this report were obtained from sources considered reliable. Their accuracy or completeness is not guaranteed and the giving of the same is not to be deemed as an offer or solicitation on our part with respect to the sale or purchase of any securities or commodities. Any decision to purchase or sell as a result of the opinions expressed in this report OR ON Equedia.com will be the full responsibility of the person authorizing such transaction.

Please view our privacy policy and disclaimer to view our full disclosure at http://equedia.com/cms.php/terms. Our views and opinions regarding the companies within Equedia.com are our own views and are based on information that we have received, which we assumed to be reliable. We do not guarantee that any of the companies will perform as we expect, and any comparisons we have made to other companies may not be valid or come into effect. Equedia.com is paid editorial fees for its writing and the dissemination of material and the companies featured do not have to meet any specific financial criteria. The companies represented by Equedia.com are typically development-stage companies that pose a much higher risk to investors. When investing in speculative stocks of this nature, it is possible to lose your entire investment over time. Statements included in this newsletter may contain forward looking statements, including the Company’s intentions, forecasts, plans or other matters that haven’t yet occurred. Such statements involve a number of risks and uncertainties. Further information on potential factors that may affect, delay or prevent such forward looking statements from coming to fruition can be found in their specific Financial reports.

Equedia Network Corporation is also a distributor (and not a publisher) of content supplied by third parties and Subscribers. Accordingly, Equedia Network Corporation has no more editorial control over such content than does a public library, bookstore, or newsstand. Any opinions, advice, statements, services, offers, or other information or content expressed or made available by third parties, including information providers, Subscribers or any other user of the Equedia Network Corporation Network of Sites, are those of the respective author(s) or distributor(s) and not of Equedia Network Corporation. Neither Equedia Network Corporation nor any third-party provider of information guarantees the accuracy, completeness, or usefulness of any content, nor its merchantability or fitness for any particular purpose.