I know things have been volatile and people are running scared, but even as the market looked like it was about to collapse – it didn’t.

Even as short selling bets against the Standard & Poor’s 500 Index rose to a nine-month high last week, that doesn’t mean we’re going to see a major pullback. If we do, those will be prime opportunities to pick up more cheap stock.

That’s why I have been proactive in telling readers not to listen so much to the media but rather follow the rally until a true signal tells us to stop:

“While I can’t sit here and confidently predict day-to-day events given the political climate, I can’t say I am surprised at what happened. For months I have been saying the markets are overvalued and that the US is in trouble – both long and short term. Does that mean the markets will continue to freefall?

The simple answer is no – the bottom for this summer drought appears to be forming.” –The Dangerous Unknown -August 8, 2011

Since that time, the markets (while still volatile) have erased most of the losses over the past months and have rebounded back. If you missed that issue, I suggest you go back and read it.

While the summer markets have been shaken, a lot of profits have already been made. If you have been following the Equedia Letter and my timing on picking up cheap shares of the major producers, the volatility and the negative outlook of our markets shouldn’t have phased you one bit:

Let’s do a quick review:

June 12, Time to Feel the Pain:

My sentiment towards gold has not changed. When you look at the broader picture of the US and the world economies, the flight to safety and wealth preservation remains a top priority. Gold will climb higher – ’nuff said.

The biggest emphasis I want to make is the disconnect between gold and gold stocks. While gold has performed incredibly well, gold equities have underperformed. But sooner or later, as I have mentioned time and time again, it will change. When it does, we’re going to see some spectacular gains in gold stocks (and other silver stocks, as well) – including the more speculative issues – as they play catch up.

The market swings in gold equities can be big, as we have already witnessed. Don’t be suckered in by selling at the bottom and trying to play catch up when the market turns. I haven’t sold any of my gold and silver stocks recently (the last time I sold was the week right before the correction – see Age of America Over?) because I strongly believe that the equity side of precious metals will turn and my patience will be rewarded with some phenomenal gains.

On June 26, “The Biggest Buyers of Garbage”:

I believe that at current prices, mining share valuations are absurdly low and that fundamentals are bound to restore them to reality. That means that over the next 6-12 months, I expect the shares of both gold miners and strong speculative explorers to finally beat the returns of gold itself. Summer is finally here and that means hunting season is coming around the corner.

When the indices plunged mid-week, gold hit a record high of $1800. That’s hardly a surprise for me and if you have been reading the Equedia Letter for a long time, you would know this. I think gold will continue to go much higher.

But that’s not what caught my attention.

When the indices plunged mid-week and gold hit a record high of $1800, guess what companies soared? That’s right, all of the gold majors.

For the first time in a long time, I saw gold stocks rally with the price of gold. Every gold major surged when gold hit $1800: Barrick, Goldcorp, Kinross, Freeport McMoran, Yamana…you name it.

Just take a look at the Market Vectors Gold Miners ETF (GDX) which surged 4 out of 5 days, ending up nearly 6%. Even the Market Vectors Junior Gold Miners ETF (GDXJ) soared, ending up just over 7%.

This is a big signal – one I am shocked that media outlets and other prominent newsletter writers failed to mention. All they saw was the volatility.

The gold mania is beginning and gold stocks are going to be a lot higher soon as gold looks to crack the $2000 threshold. The gold producers climbed significantly when gold rallied to $1800 last week. Imagine what they will do when gold hits $2000. Imagine where gold will go once QE3 is announced. Imagine where gold will go once Europe spends its way out of trouble.

Once the majors get rolling, the juniors will follow as buyouts and takeover rumours begin. The majors will take advantage of beat up juniors and this will fuel speculation into that market segment. Then the triple digit returns will begin.

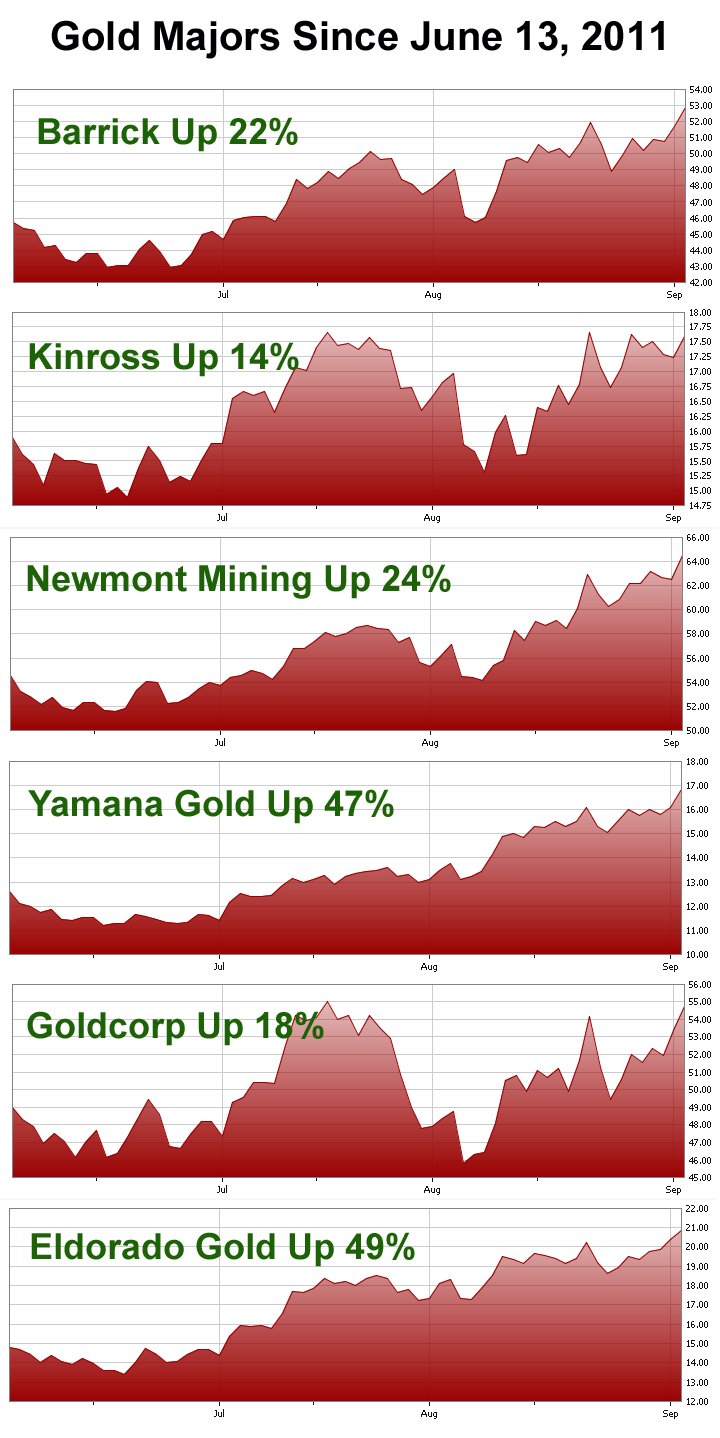

Take a look at what some of the majors have done since June:

|

| Gold Major Charts as of September 2, 2011 |

There’s no doubt in my mind, despite the early gains already made, that this upward trend of the major gold producers will continue. Aside from the many factors I have discussed in previous letters regarding gold’s climb, even more reasons emerge on a daily basis as to why gold prices will continue to climb – as they have for the past 11 years.

There are reasons why senior German government officials are calling for the gold reserves of European countries such as Greece, Portugal, Spain, Italy and Ireland to be used as collateral for future loans.

There are reasons why Kazakhstan has given its central bank a ‘priority right’ to purchase all domestically mined gold “in full”.

There are reasons why major hedge funds and central banks around the world are buying gold. Central banks internationally have been net buyers of gold since 2009, despite being net sellers for nearly two decades. (see The Next Big Boom)

There are reasons why the People’s Bank of China is building their gold reserves without declaring it to the world and is encouraging their citizens to buy gold. (see Everything Has Changed)

There are reasons why Venezuelan President Hugo Chavez said that he plans to nationalize the gold sector and use the production to boost the country’s international reserves and why he’s ordered the repatriation of 90 percent of Venezuela’s gold reserves held abroad, to be returned back to Caracas. (see The Hoarding Has Begun)

There are reasons why stock exchanges around the world are allowing gold to be used as AAA collateral. (see The First Time in History)

There are reasons why even life insurance companies are buying gold for the first time in history (see The Next Big Boom)

There are reasons why many states in the US are pushing for precious metals to be used as legal tender. (see The Greatest War in History)

There are reasons why China, amongst other countries, have created new platforms for the trading of gold. (see Before it’s Too Late)

The list goes on…and on.

While the media and Ben Bernanke would have you believe that gold is not money nor should it be treated like it, the evidence says otherwise.

Just last week, Russia’s central bank announced that it will offer gold-backed loans for up to 90 days at an interest rate of 7 percent, expanding its lending facilities for dealing with any future liquidity crunch in the banking system.

The Russian Secret: Russia Unloads US Bonds

According to Reuters:

The gold-backed lending was approved by the board of directors at a meeting on Friday. The rate on the facility is in line with the central bank’s Lombard rate on borrowing secured against high-quality bonds.

“This measure fits the central bank’s policy of developing refinancing instruments within the banking system. The facility will be unlikely in strong demand, only at times of liquidity crunches,” said Maxim Oreshkin, chief economist at Credit Agricole in Moscow.

Levels of rouble liquidity remain at comfortable levels for now, with the overnight interbank rate having hovered within 3-4 percent range since early 2010 compared to more than 10 percent seen during the crisis of 2008-2009.

Russia has been relentlessly unloading its US bonds. It has been buying gold at record pace. Now they’re offering gold-backed loans to expand its lending facilities for dealing with any future liquidity crunch in the banking system. If there is a liquidity crunch, (which is very possible) Russia will be able to hoard even more gold as citizens and those with gold scramble to pay their bills.

Perhaps this is a secret ploy by the Russian government to discretely confiscate gold. Other central banks, stock exchanges, hedge funds, and even insurance companies are hoarding their gold and looking for ways to increase their holdings. Why aren’t you?

Gold Stocks

Many of the miners are still trading at valuations that haven’t been seen since the 1970’s. While many of the majors are now trading at, or near, 52-week highs, the time to add or enter new positions is still ripe. That’s because many of the companies have valuations far below gold’s current price.

For example, Newmont Mining currently values its resources at a price of $900/oz, which means they try to determine if their projects are feasible at that price. Gold is nearly $2000 ounce. When Newmont decides to move their current resources into the feasibility stage over the coming years, their valuations of resources in the ground would become much more significant – provided gold stays at these high prices.

Another example is Eldorado Gold. Even though it is trading at 20 times next year’s earnings and 15 times next year’s cash flow, they’re expected to double production within 4 years and is currently one of the lowest cost producers with signifcant exploration potential.

The list of big name gold producers are all high a top of my list of stocks to own – if I don’t own them already. Many of them have already been mentioned in the chart above and include: Barrick, Goldcorp, Kinross, and Yamana. If you are going to speculate that gold prices are going to climb or remain at these levels, these are all great bets in my books.

The Juniors

With the low valuations given by the market to the gold juniors and mid-tier explorers, I expect to see a strong wave of takeovers, buyouts, and mergers in the coming months.

Just last week, AuRico Gold Inc. announced a $1.46-billion deal to take over Northgate Minerals Corp. Including net cash, AuRico’s acquisition valued Northgate at 14.7 times earnings before interest, taxes, depreciation and amortization – that’s the lowest valuation since 2004 for a North American deal worth more than $1 billion. If gold prices stay the same, or go higher as I predict, that’s a pretty sweet deal for AuRico.

We also saw Cameco come out with a hostile bid for Hathor. While the Cameco-Hathor deal is not of the precious metals sector, the fact is that the majors are looking to acquire many of the battered juniors and this trend will continue.

When the share prices of the majors rise and the juniors lag behind, it gives the majors substantial pull in using their valuations to target the lower valuations of the juniors. The market knows this. You’ve already seen many of the majors surge since June. This surge will continue and the juniors will eventually follow as I mentioned in “The Big Signal.”

September is here and the market will slowly get back to more aggressive trading as the kids go back to school and the adults get back to work. Even with the strong gains since June, gold stocks still have plenty of room to grow.

It’s time to shine.

Disclosure: I own and plan to purchase both large caps and small cap gold stocks, including Barrick which is mentioned in this article. I also own long positions in gold and silver through ETF’s.

Until next week,

Ivan Lo

Equedia Weekly

For the full interactive newsletter and report, please follow this link: http://archive.constantcontact.com/fs005/1102243211822/archive/1107419012621.html

Forward-Looking Statements

This Newsletter and report contains certain forward-looking statements that may involve a number of risks and uncertainties. Actual events or results could differ materially from current expectations and projections. Except for statements of historical fact relating to the project, certain information contained herein constitutes “forward-looking statements”. Forward-looking statements are frequently characterized by words such as “plan”, “expect”, “project”, “intend”, “believe”, “anticipate” and other similar words, or statements that certain events or conditions “may” or “will” occur.

Except for the statements of historical fact, the information contained herein is of a forward-looking nature. Such forward-looking information involves known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievement of the Company to be materially different from any future results, performance or achievements expressed or implied by statements containing forward-looking information.

Although the Company has attempted to identify important factors that could cause actual results to differ materially, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that statements containing forward looking information will prove to be accurate as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on statements containing forward looking information. Readers should review the risk factors set out in the Company’s prospectus and the documents incorporated by reference.

Cautionary Note to U.S. Investors Concerning Estimates of Inferred Resources

This presentation uses the term “Inferred Resources”. U.S. investors are advised that while this term is recognized and required by Canadian regulations, the Securities and Exchange Commission does not recognize it. “Inferred Resources” have a great amount of uncertainty as to their existence, and great uncertainty as to their economic and legal feasibility. It cannot be assumed that all or any part of an Inferred Resource will ever be upgraded to a higher category. Under Canadian rules, estimates of “Inferred Resources” may not form the basis of feasibility or other economic studies. U.S. investors are also cautioned not to assume that all or any part of an “Inferred Mineral Resource” exists, or is economically or legally mineable.

Disclaimer and Disclosure

Disclaimer and Disclosure Equedia.com & Equedia Network Corporation bears no liability for losses and/or damages arising from the use of this newsletter or any third party content provided herein. Equedia.com is an online financial newsletter owned by Equedia Network Corporation. We are focused on researching small-cap and large-cap public companies. Our past performance does not guarantee future results. Information in this report has been obtained from sources considered to be reliable, but we do not guarantee that it is accurate or complete. This material is not an offer to sell or a solicitation of an offer to buy any securities or commodities.

Furthermore, to keep our reports and newsletters FREE, from time to time we may publish paid advertisements from third parties and sponsored companies. We are also compensated to perform research on specific companies and often act as consultants to many of the companies mentioned in this letter and on our website at equedia.com. We also make direct investments into many of these companies and own shares and/or options in them. Therefore, information should not be construed as unbiased. Each contract varies in duration, services performed and compensation received.

Equedia.com is not responsible for any claims made by any of the mentioned companies or third party content providers. You should independently investigate and fully understand all risks before investing. We are not a registered broker-dealer or financial advisor. Before investing in any securities, you should consult with your financial advisor and a registered broker-dealer. The information and data in this report were obtained from sources considered reliable. Their accuracy or completeness is not guaranteed and the giving of the same is not to be deemed as an offer or solicitation on our part with respect to the sale or purchase of any securities or commodities. Any decision to purchase or sell as a result of the opinions expressed in this report OR ON Equedia.com will be the full responsibility of the person authorizing such transaction.

Again, this process allows us to continue publishing high-quality investment ideas at no cost to you whatsoever. If you ever have any questions or concerns about our business or publications, we encourage you to contact us at the email or phone number below.

Please view our privacy policy and disclaimer to view our full disclosure at http://equedia.com/cms.php/terms. Our views and opinions regarding the companies within Equedia.com are our own views and are based on information that we have received, which we assumed to be reliable. We do not guarantee that any of the companies will perform as we expect, and any comparisons we have made to other companies may not be valid or come into effect. Equedia.com is paid editorial fees for its writing and the dissemination of material and the companies featured do not have to meet any specific financial criteria. The companies represented by Equedia.com are typically development-stage companies that pose a much higher risk to investors. When investing in speculative stocks of this nature, it is possible to lose your entire investment over time. Statements included in this newsletter may contain forward looking statements, including the Company’s intentions, forecasts, plans or other matters that haven’t yet occurred. Such statements involve a number of risks and uncertainties. Further information on potential factors that may affect, delay or prevent such forward looking statements from coming to fruition can be found in their specific Financial reports.

Equedia Network Corporation is also a distributor (and not a publisher) of content supplied by third parties and Subscribers. Accordingly, Equedia Network Corporation has no more editorial control over such content than does a public library, bookstore, or newsstand. Any opinions, advice, statements, services, offers, or other information or content expressed or made available by third parties, including information providers, Subscribers or any other user of the Equedia Network Corporation Network of Sites, are those of the respective author(s) or distributor(s) and not of Equedia Network Corporation. Neither Equedia Network Corporation nor any third-party provider of information guarantees the accuracy, completeness, or usefulness of any content, nor its merchantability or fitness for any particular purpose.