Silver is undeniably one of the most favoured investment vehicles for the top minds in the industry. From its ability to rise with a growing economy, to a precious metals hedge against inflation, silver is a metal with many talents.

Right now, we’re seeing history in the making for silver. 2012 will be a big year for silver and with it, my favourite way to play the precious metals boom: silver stocks.

This may all sound familiar to you. That’s because during the last few years, every silver company we featured showed our readers gains of 100% plus.

So it’s no wonder why our first report for 2012 involves a silver company that analysts are calling “one of the most important high grade silver projects on the planet.”

More on this story in a bit.

Silver Set to Explode

In a report published earlier this year (see Before it’s Too Late), Eric Sprott and Andrew Morris pointed out the significant discord between paper and physical supply on the Comex relating to silver:

…Over 800 million ounces traded each day in April on (the Comex). Further, consider that as at the end of April there were only 33 million ounces of registered inventories to back up all of that paper trading. Just imagine if a mere 5% of all of that buying actually stood for delivery; the entire inventories would be more than wiped out.

He concluded that, “With more and more dollars flowing into the silver markets and a finite supply of physical to meet that demand, the theoretical losses for the paper silver short-sellers are near infinite. And with such a skewed and obvious risk/reward payoff vastly favouring the longs, we pose the following question. Who is most at risk in the silver markets: the buyers of a scarce and real asset that serves a growing multitude of purposes, or the sellers, who are short a quantity of silver that may very well not even be obtainable at anywhere near current prices? Let the seller beware!”

Some of the smartest minds in the industry are already calling for $50, $75, $100, and even $150 dollar silver. While these numbers seem far off, critics also said the same when silver hit $20 a few years back, before it skyrocketed to nearly $50.

In the last ten years, the price of silver has had four major crashes, yet it still increased five-fold. Take a look:

Every time silver crashed, it found a way to climb higher – much higher.

The net result? If you invested US$10,000 in silver at the start of 2004, it would now be worth $58,000 plus.

While silver saw a 48% correction last year, it is now poised to explode with clear signs the latest correction is finished. Not only does silver generally bottom at this time of year, it’s starting to break above its 65 week moving average.

But that’s not all.

While institutional and retail demand for physical silver is on the rise (and over 255 million ounces short, according to Eric Sprott), industrial demand is also growing at a staggering pace.

We all know that China has played a pivotal role in the price of gold increase (see Where the Billionaires Invest). As recently as 2002, the private ownership of gold was prohibited in China. But since 2009, the central Chinese government removed all restrictions and began to encourage their citizens to buy precious metals such as gold and silver.

Again, because not everyone can afford gold, many of their citizens will be rushing toward silver. Practically every bank in China now sells gold and silver bullion bars in different sizes. And with a savings rate of 30-40%, you can bet the Chinese are buying these up. Heck, there are even reports of mining employees that have been encouraged to convert some of their wages to gold on payday.

In addition to bullion alone, China also represents an ever-growing economy migrating from a developing nation to first world country. This means that millions upon millions of Chinese citizens will be buying new TV`s, cell phones and devices that require silver.

China’s silver consumption already accounts for 70% of the global total of industrial use, and its middle class is far from reaching its spending potential. This will undoubtedly send the silver supply further downward as global production slows.

Think about it. How many silver producers are there out there? Not many.

The amount of silver coming out of the ground is going down every year. Few discoveries have been announced in the last decade and most silver produced now is coming from the last stages of existing mines.

Not only that, but the quality of silver mined is the lowest it’s ever been and like most metals, silver is rarely mined in veins now. It takes many tons of earth and rock to process even a single ounce.

And that’s what makes the next company I am about to introduce so special.

One of the Highest Grade Silver Projects on the Planet: The Most Important Silver Project in the World

Haywood Securities called this company’s marquee project “one of the most important high grade silver projects globally.”

Canaccord Genuity views this company as “a likely acquisition target with a joint venture that hosts one of the richest and highest-grade silver deposits worldwide …It’s simply one of the most attractive undeveloped silver projects on the planet.”

BMO Capital Markets says the company’s “current resource and exploration upside at their (flagship project) together with the company’s other 100%-owned district-scale holdings in Mexico comprise an attractive asset for any silver producer, not just (the world’s largest primary silver producer in the world.) ”

If you’re looking for the next silver play and a potential takeover target, look no further than:

MAG Silver Corp (TSX: MAG) (NYSE.A: MVG)

We’re not the only ones who think so.

Experts at Raymond James and Canaccord Genuity both have strong buy ratings for MAG Silver Corp (TSX: MAG)(NYSE.A: MVG) (and all believe that MAG Silver may be the next potential takeover target – especially given the significant events that have occurred with MAG over the last few years.)

Canaccord just upgraded MAG Silver Corp (TSX: MAG)(NYSE.A: MVG) with a higher target price, while Raymond James has also done the same. Target prices from large institutions are often very conservative, factoring in every possible risk. With the price of silver looking to explode again, these target prices will undoubtedly be raised to reflect that.

But there’s another significant reason why these target prices may soon be raised much higher.

MAG is about to announce something in the next few weeks that has the potential to make MAG Silver’s NPV (Net Present Value) rise dramatically. Based on the numbers in their previous PEA and more current silver prices, MAG’s NPV could easily double from where it stands today – resulting in an even bigger discount to MAG Silver’s current share price.

Simply One of the Most Attractive Undeveloped Silver Projects on the Planet: Juanicipio Joint Venture

MAG Silver Corp’s (TSX: MAG)(NYSE.A: MVG) flagship project is its Juanicipio Joint Venture with the world’s largest primary silver producer, Fresnillo. It’s located in the Juanicipio property, of which MAG owns 44% and Fresnillo the remainder 56%.

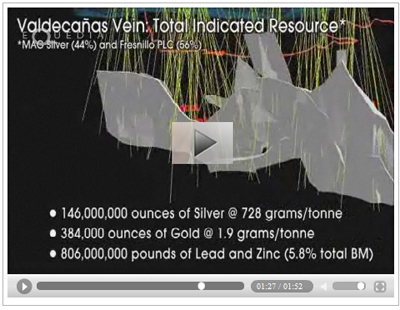

Juanicipio is an exceptionally high grade epithermal vein system that has the potential to produce up to 16 million ounces of silver per year. It is considered to be one of the richest silver discoveries in recent history, hosting an astounding:

Indicated resource of 6.2 million tonnes with an astounding average grade of 728 grams/t silver, 1.9 g/t gold, 1.9% lead, 3.9% zinc (containing 146 million ounces of silver)

and

Inferred resource of 7.1 million tonnes with an average grade of 373 g/t silver, 1.6 g/t gold, 1.5% lead, and 2.6% zinc (containing 85 million ounces of silver)

That’s not a typo. The Juanicipio Joint Venture contains an indicated resource of 146 million ounces with an average grade of 728 grams/t silver and 1.9 g/t gold and an inferred resource of 85 million ounces of silver with and average grade of 373 g/t silver and 1.6 g/t gold.

I know I am repeating myself. But these numbers are so spectacular that when I speak with industry experts, they find it hard to believe. These type of numbers simply don’t exist anymore.

The vast majority of the Juanicipio resource is hosted within the principal vein, the Valdecanas, which spans over 1600 metres in length with average vein width between 4 and 6 metres.

If you look at the map, Fresnillo has already developed its Jarillas shaft and the Saucito mill within 800 metres of the Valdecanas vein on the JV property.

|

| click to enlarge |

It’s no wonder why analysts at Canaccord Genuity call Juanicipio:

simply one of the most attractive undeveloped silver projects on the planet.

Crunching the Numbers

A scoping study was done a few years back and the numbers are truly remarkable – especially considering the low silver price used in the calculations ($12 silver).

Based on a scoping study done in 2009, the NPV (Net Present Value) of the Juanicipio project is estimated at US$ 967M using a 5% discount rate and a silver price of US$12.32 per ounce. That means MAG’s share at 44% is estimated at US$425.5M. The payback period is 2.3 years with an estimated CAPEX of US$ 217.0M.

Operating cost were estimated at US$ 42.28 per tonne milled, which means that the unit cost per ounce of accountable silver sits at only US$ 2.56. Considering silver is over US$33 /ounce today, that spells significant profits for MAG and anyone developing this project.

If we were to use a higher silver price in our calculations, say US$15 /ounce, MAG’s NPV would soar to over $1.1 billion. That means every dollar increase in the price of silver adds another $100 million plus to MAG’s NPV. Just take a look:

|

| click to enlarge |

This scoping study is based on a stand-alone mine development, with a 3.5 year development timeline to advance ramp down to the Valdecanas mineralization. While there are no current studies for alternative development scenarios, much of the CAPEX costs could be reduced significantly and development timeline significantly shortened if MAG were to use Fresnillo’s current infrastructure. By drifting over from the Jarillas shaft less than 1km away, the development timeline could potentially be reduced to 18 months, instead of the 3.5 years estimated in the scoping study.

Furthermore, even if mine development were to commence without the use of Fresnillo’s nearby infrastructure, the payback period given today’s current silver price could be less than a year. Try finding another silver project like this.

|

| click to play |

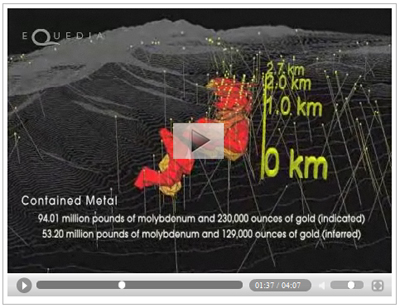

In addition to Juanicipio, MAG Silver Corp (TSX: MAG)(NYSE.A: MVG) also has a strong portfolio of promising high grade silver district projects in Mexico. One of these projects is their 100% owned Cinco de Mayo, which contains a high grade Moly-Gold project that alone would be a major company maker.

Cinco de Mayo, Pozo Seco & Jose Manto Projects

The Cinco de Mayo property comprises 22,000 hectares and is the most advanced of MAG’s five Carbonate Replacement Deposit (“CRD”) style targets.

MAG Silver Corp (TSX: MAG)(NYSE.A: MVG) has already outlined a 147 million pound high grade molybdenum deposit at Pozo Seco within Cinco de Mayo. The deposit is entirely oxidized and possess a very high average molybdenum grade of 0.13%.

|

| click to play |

Over the next few months, MAG is expected to release – for the first time – a new PEA (Preliminary Economic Assessment) that should show the potential for their Pozo Seco high grade Moly project. That means more news and more milestones to come for the company that already has one of the most attractive undeveloped silver projects in the world.

In addition, MAG continually intercepts significant massive sulphides in its on-going exploration drilling at Cinco de Mayo, including a most recent hole of 386 grams per tonne (g/t) (12.4 ounces per tonne (opt)) silver with 14.0% zinc and 8.2% lead over 3.98 metres (298.88 to 302.86 metres downhole) including a high grade core of 1,170 g/t (34.0 opt) silver with 13.7% zinc and 19.1% lead over 0.86 metres.

Of course, like any smart explorer, MAG Silver Corp (TSX: MAG)(NYSE.A: MVG) also has other significant and highly prospective projects in the Mexico Area. You can read more about them below.

Combined with Juanicipio, MAG is on the way to a breakout year. Analysts from all over the nation are calling the Juanicipio project one of the richest and highest grade silver deposits in the world and simply one of the most attractive undeveloped silver projects on the planet.

With such an amazingly high grade silver project, you may be asking yourself: “Why haven’t I heard of MAG before and why isn’t the company trading at much higher prices?”

Why MAG Silver is Under the Radar

In 2008, Fresnillo, which owns 56% of the Juanicipio project, tried a low-balled hostile takeover offer of MAG for US$4.54 per share without any success. During that time, MAG filed a formal request for arbitration on the grounds that Fresnillo attempted to acquire control of MAG on a hostile basis, in breach of standstill provisions contained in the shareholders agreement governing the Juanicipio joint venture.

Two years later, in 2011, the arbitration ruling was issued. And MAG had not only won, but ended up with a much easier path to success.

The arbitration ruling stipulated that any deal would need to be friendly, any offer would need to be cash. Fresnillo must move the project forward with MAG in a reasonable time frame – meaning Fresnillo cannot hold back on moving the project forward to suppress MAG’s progress. As a matter of fact, exploration budgets have already increased this year.

As a result of the ruling, MAG’s share prices rocketed to over $14 last year, only to be pulled back with the rest of the market. But with silver prices expected to climb in 2012, an updated PEA out within the next few weeks, and nearly $11 million of exploration underway for both Juanicipio and Cinco de Mayo, this could be the breakout year for MAG Silver.

It’s Getting Crowded

Silver is an asset whose consumption will exceed new production for many years. With just $50 billion of silver bullion above ground, the silver market is a very small market and gets crowded easily. The amount of silver stocks with strong assets are very limited and very few discoveries are being made worldwide.

Over the next few years, we’re going to see a lot of consolidation in the silver space – especially for companies with high grade projects.

It’s already happening…

Just last week, we saw the takeover of Minefinders by Pan American Silver for $1.6 billion.

So how does Minefinders’ silver project compare to MAG’s?

According to Morningstar:

Most of Minefinders’ silver reserves and all of its current production come from its Dolores open-pit mine in northwest Mexico. Dolores is projected to produce more than 65,000 ounces of gold and 3.4 million ounces of silver in 2011 at cash costs of between $11 and $12 per silver-equivalent ounce (assuming a 41/1 gold to silver price ratio), but seems capable of supporting a much larger annual production rate given its sizable silver reserves.

Dolores’ low cash costs should also help Pan American better control its production cost inflation, as the firm’s existing silver mines are projected to reach cash costs of more than $18 per silver-equivalent ounces in 2011.

Based on the 2009 scoping study, MAG’s unit cost per ounce of accountable silver (net of by product credit and TTM* costs) is expected to be US$1.77 – a big difference to the US$11-12 cost of Minefinders and an even bigger difference to Pan American’s US$18.

Clearly you can now see why analysts are calling Juanicipio one of the most important high grade silver projects on the planet.

Silver prices are near $35/oz and are expected to climb much higher. You can do the math.

Timing is Crucial

There’s no doubt that MAG has one of the most promising silver projects in the world. But that’s not the only reason I am about to buy their shares right now.

Within the next few weeks, MAG is about to hit a critical milestone that could send share prices much higher than where it is today…

MAG is about to announce an updated PEA using much higher silver prices than the PEA done in 2009. The upcoming PEA on one of the world’s highest grade silver deposits is going to be a critical milestone for MAG as it will truly show the real value of what the Juanicipio project has to offer.

To give you an example of how big an impact an updated PEA can be, let’s go back and look at Hathor – the company that hosted one of the world’s richest uranium deposits.

As you can remember, just a few weeks before Hathor announced their new PEA, not only did their share price soar, but takeover bids and rumours started to pour in with Cameco making the first unsuccessful bid.

Once Hathor’s new PEA was released, mining giant Rio Tinto made their move and bought Hathor at significantly higher prices.

While in a different sector, the MAG story has many similarities. While Hathor had one of the richest uranium deposits in the world, MAG has one of the richest silver deposits in the world. Hathor received a failed low-balled takeover attempt by Cameco. MAG received a failed low-balled take-over attempt by Fresnillo.

Once MAG’s new PEA comes out in the next few weeks, you can be sure Fresnillo will be watching as other big shots in the silver space drool over MAG’s asset. With the new PEA, the NPV for MAG would not only rise significantly based on higher silver prices, but it also means that Fresnillo would have to pay more for MAG if it wanted to buy MAG out.

It’s obvious that MAG is a likely acquisition target.

Fresnillo has already boldly claimed that it has a goal of increasing its annual production to 65 million ounces of silver by 2018, up from a current production of around 42 million ounces.

The Juanicipio project is expected to produce an average of 14 million ounces of silver annually. While 100% of Juanicipio would not likely get Fresnillo to its bold goals, it should certainly help the company along the way.

It’s apparent that Fresnillo would be the smartest and most economical suitor of the Juanicipio project. If Fresnillo were to use its existing infrastructure as I had already mentioned, not only would the CAPEX be significantly reduced, but the timeline would also be dramatically shortened (potentially down to 18 months from 3.5 years.)

The reduced cost and shortened timeline makes a compelling and obvious reason why Fresnillo should make a move.

Of course, the only thing that stands in the way is the recent past between MAG and Fresnillo. But at the end of the day, the courts have made their decision and any deal Fresnillo wants will not only have to be friendly, but have to be all cash. The only question is will Fresnillo come to a friendly agreement with MAG?

If Fresnillo doesn’t make a move soon, I wouldn’t be surprised to see other suitors come to the table before MAG continues to increase its value via further exploration work on Juanicipio and its other properties. The big institutions feel the same way:

If Fresnillo does intend to eventually acquire MAG`s interest in Juanicipio, with an increased in exploration budget from last year, an updated PA for the Juanicipio project, and new value to be created at its Cinco De Mayo and Pozo Seco projects, the potential cost of acquiring MAG is likely only to increase over time.

The challenge of structuring a friendly deal between the two companies is obvious, but despite the history, the argument supporting the potential friendly bid for MAG appears compelling. Even without a bid from Fresnillo, we believe the outlook for MAG has improved, which could potentially attract other suitors.” – Canaccord, January 22, 2012

Fresnillo is the biggest player in the primary silver space and you can bet they wouldn’t want any partners on their home turf – especially when MAG is sitting right in their backyard.

MAG is already undervalued based on a 0.75x multiple to Canaccord’s peak silver price estimate of NAVPS (net asset value per share, 7.5% US$35/oz Ag). With an updated PEA on Juanicipio, an upcoming PEA on Pezo Seco, drill results coming from their other high grade silver projects, and the possibility of a takeover, MAG will undoubtedly be the focus of anyone in the silver space.

MAG’s management is top notch and their share structure is rock solid. Management has been able to turn MAG from a penny stock to where it trades today – all without diluting shareholders. They have over US$27 million in the bank and less than 60 million shares outstanding when fully diluted. That is an amazing task considering the progress MAG has made.

The real silver boom is about to begin.

That is why I will be investing in “one of the most important high grade silver projects on the planet.”

That is why I will be investing in MAG Silver…

MAG Silver Corp.

Cdn Symbol: (TSX: MAG)

US Symbol: (NYSE.A: MVG)

Share Price: CDN $8.09

We’re biased towards MAG Silver because they are an advertiser and we will be buying shares (update: we have now purchased shares after the release of this report. You can do the math. Our reputation is built upon the companies we feature. That is why we invest in every company we feature in our Equedia Reports, including MAG Silver. It’s your money to invest and we don’t share in your profits or your losses, so please take responsibility for doing your own due diligence. Remember, past performance is not indicative of future performance. Just because many of the companies in our previous Equedia Reports have done well, doesn’t mean they all will. Furthermore, MAG Silver and its management has no control over our editorial content and any opinions expressed are those of our own.

Until next week,

Ivan Lo

Equedia Weekly

Questions?

Call Us Toll Free: 1-888-EQUEDIA (378-3342)

* Source “Wardrop – Valdecañas Project – Scoping Study, NI 43-101 Technical Report”

MAG Silver Corp is a Canadian issuer.

Daniel MacInnis P.Geo is a non-independent Qualified Person and has compiled this presentation from industry information and 43-101 reports and news releases with specific underlying Qualified Persons as set out in the Releases and reports. Industry Information has been compiled from publicly available sources and may not be complete, up to date or reliable.

This presentation contains forward-looking statements within the meaning of Canadian and U.S. securities laws. Such forward looking statements are subject to risks and uncertainties which could cause actual results to differ materially from estimated results. Such risks and uncertainties include, but are not limited to, the Company’s ability to raise capital to fund development and exploration, changes in general economic conditions or financial markets, changes in metal prices, general cost increases, litigation, legislative, environmental and other judicial, regulatory, political and competitive developments in Mexico or Canada, technological and operational difficulties or inability to obtain permits encountered in connection with The Company’s exploration activities, community and labor relations matters and changes in foreign exchange rates, all of which are described in more detail in the Company’s filings with the Securities and Exchange Commission. There is no certainty that any forward looking statement will come to pass and investors should not place undue reliance upon forward-looking statements

This presentation uses the term “Indicated Resources”. MAG advises investors that although this term is recognized and required by Canadian regulations (under National Instrument 43-101 Standards of Disclosure for Mineral Projects), the U.S. Securities and Exchange Commission does not recognize this term. Investors are cautioned not to assume that any part or all of mineral deposits in this category will ever be converted into reserves.

Cautionary Note to Investors Concerning Estimates of Inferred Resources: This presentation uses the term “Inferred Resources”. MAG advises investors that although this term is recognized and required by Canadian regulations (under National Instrument 43-101 Standards of Disclosure for Mineral Projects), the U.S. Securities and Exchange Commission does not recognize this term. Investors are cautioned not to assume that any part or all of the mineral deposits in this category will ever be converted into reserves. In addition, “Inferred Resources” have a great amount of uncertainty as to their existence, and economic and legal feasibility. It cannot be assumed that all or any part of an Inferred Mineral Resource will ever be upgraded to a higher category. Under Canadian rules, estimates of Inferred Mineral Resources may not form the basis of feasibility or pre-feasibility studies, or economic studies except for Preliminary Assessment as defined under Canadian National Instrument 43-101. Investors are cautioned not to assume that part or all of an Inferred Resource exists, or is economically or legally mineable. The Company may access safe harbor rules. Please see complete information on SEDAR and at the SEC on EDGAR.

This presentation is for information purposes only and is not a solicitation. Please contact the Company for complete information and consult a registered investment representative / advisor prior to making any investment decision.

Note to U.S. Investors: Investors are urged to consider closely the disclosure in MAG Silver’s Form 40F, File no. 001-33574, available at their office: Suite 770-800 West Pender, Vancouver BC, Canada, V6C 2V6 or from the SEC: 1(800) SEC-0330. The Company may access safe harbor rules.

Investors are urged to consider closely the disclosures in MAG Silver’s annual and quarterly reports and other public filings, accessible through the Internet at www.sedar.com and www.sec.gov/edgar/searchedgar/companysearch.html

Neither the TSX Venture Exchange nor the New York Stock Exchange Alternex has reviewed or accepted responsibility for the accuracy or adequacy of this presentation.

Disclaimer and Disclosure

Equedia.com & Equedia Network Corporation bears no liability for losses and/or damages arising from the use of this newsletter or any third party content provided herein. Equedia.com is an online financial newsletter owned by Equedia Network Corporation. We are focused on researching small-cap and large-cap public companies. Our past performance does not guarantee future results. Information in this report has been obtained from sources considered to be reliable, but we do not guarantee that it is accurate or complete. This material is not an offer to sell or a solicitation of an offer to buy any securities or commodities.

Furthermore, to keep our reports and newsletters FREE, from time to time we may publish paid advertisements from third parties and sponsored companies. We are also compensated to perform research on specific companies and often act as consultants to many of the companies mentioned in this letter and on our website at equedia.com. We also make direct investments into many of these companies and own shares and/or options in them. Therefore, information should not be construed as unbiased. Each contract varies in duration, services performed and compensation received.

Equedia.com is not responsible for any claims made by any of the mentioned companies or third party content providers. You should independently investigate and fully understand all risks before investing. We are not a registered broker-dealer or financial advisor. Before investing in any securities, you should consult with your financial advisor and a registered broker-dealer. The information and data in this report were obtained from sources considered reliable. Their accuracy or completeness is not guaranteed and the giving of the same is not to be deemed as an offer or solicitation on our part with respect to the sale or purchase of any securities or commodities. Any decision to purchase or sell as a result of the opinions expressed in this report OR ON Equedia.com will be the full responsibility of the person authorizing such transaction.

Again, this process allows us to continue publishing high-quality investment ideas at no cost to you whatsoever. If you ever have any questions or concerns about our business or publications, we encourage you to contact us at the email or phone number below.

Please view our privacy policy and disclaimer to view our full disclosure at http://equedia.com/cms.php/terms. Our views and opinions regarding the companies within Equedia.com are our own views and are based on information that we have received, which we assumed to be reliable. We do not guarantee that any of the companies will perform as we expect, and any comparisons we have made to other companies may not be valid or come into effect. Equedia.com is paid editorial fees for its writing and the dissemination of material and the companies featured do not have to meet any specific financial criteria. The companies represented by Equedia.com are typically development-stage companies that pose a much higher risk to investors. When investing in speculative stocks of this nature, it is possible to lose your entire investment over time. Statements included in this newsletter may contain forward looking statements, including the Company’s intentions, forecasts, plans or other matters that haven’t yet occurred. Such statements involve a number of risks and uncertainties. Further information on potential factors that may affect, delay or prevent such forward looking statements from coming to fruition can be found in their specific Financial reports. Equedia Network Corporation., owner of Equedia.com has been paid $5833.33 plus HST per month for 6 months which totals $35,000 plus hst of media coverage on MAG Silver Corp. plus any other marketing related expenses. MAG Silver Corp. has paid for this service. Equedia.com may purchase shares of MAG Silver without notice and intend to sell every share we purchase for our own profit. We may sell shares in MAG Silver Corp without notice to our subscribers.

Equedia Network Corporation is also a distributor (and not a publisher) of content supplied by third parties and Subscribers. Accordingly, Equedia Network Corporation has no more editorial control over such content than does a public library, bookstore, or newsstand. Any opinions, advice, statements, services, offers, or other information or content expressed or made available by third parties, including information providers, Subscribers or any other user of the Equedia Network Corporation Network of Sites, are those of the respective author(s) or distributor(s) and not of Equedia Network Corporation. Neither Equedia Network Corporation nor any third-party provider of information guarantees the accuracy, completeness, or usefulness of any content, nor its merchantability or fitness for any particular purpose.

you are really a just right webmaster. The site loading velocity

is amazing. It sort of feels that you are doing any distinctive trick.

Furthermore, The contents are masterwork. you’ve done a great process on this topic!