*If you have not already subscribed to our weekly interactive newsletter, please visit:http://equedia.com/newsletter/

For the full interactive edition, please CLICK HERE

Usage: Feel free to post this article anywhere you’d like. Just be sure to follow the rules set forth in our usage agreement by CLICKING HERE

My mom taught me that if I had nothing better to say, don’t say anything. I wonder if Bernanke’s mom had taught him the same thing?

After starting the week off with a bang as I anticipated (The New Breed of Destruction), the market once again tumbled back down towards the end of trading Wednesday when Bernanke decided to open his big mouth. His comments were more of the same…slower growth anticipated, near-zero interest rates, pace of progress in employment remains frustratingly slow, slightly higher unemployment rate in the near future, and that he is clueless as to why the economy is in a soft patch.

It’s no wonder why Bernanke’s standing with the public has slid to its lowest level in almost two years of polling on the issue.

Here is a guy who scored 1590 out of 1600 on his SAT. Undoubtedly, he is smarter than the rest of us – yet he can’t seem to see the obvious problems facing his country. But let’s give him a little credit first.

During the crisis, the Federal Reserve undertook US$3.3-trillion in emergency lending and cut interest rates between zero to 0.25 percent. To support the housing market, it launched a plan to purchase US$1.43-trillion in housing debt. As a result of his actions, Bernanke was named Time Magazine’s “Person of the Year” in December 2009 for being the “mild-mannered man” who “prevented an economic catastrophe.” The S&P 500 began to rise in March 2009 and has since climbed 90% due to QE1 and QE2.

But now that QE2 is officially ending next week, along with the downgraded forecasts and uncertainty by Bernanke, the markets are sinking fast. The QE bandages are coming off and the blood is starting to spill once again.

But this won’t last long. The US will eventually have to bring back another round of Quantitative Easing (as mentioned before).

Why? Because no one else will buy US debt…except for the Fed.

The Biggest Buyers of Garbage

Let’s start with one of US’ biggest purchasers: China

I have already mentioned in the past that China has announced it will begin to diversify its massive $3 trillion dollar foreign reserve stockpiles of US dollar into investment funds designed to invest in precious metals and oil (see Age of America Over?).

Furthermore, Zhou Xiaochuan, the governor of China’s central bank, told us a couple of months back that China’s foreign exchange reserves “exceed(s) (their) reasonable requirement” and that the government should upgrade and diversify its foreign exchange management using the excessive reserves.

Aside from taking their US stockpile and investing it in global natural resources, China is already spending its money elsewhere: Europe.

In a research note published by the Standard Chartered Bank, China likely bought more European sovereign debt in the first four months of the year than it did U.S. dollar assets, stating that it appears to be a concerted effort to diversify away from the greenback.

Here’s more from the research note:

“Of the nearly $200 billion worth of foreign-exchange reserves China accumulated in the January-April period, it likely channelled $150 billion into non-U.S. assets…China is diversifying away from the U.S. assets at the margin, buying proportionally less U.S. paper with its new foreign-exchange reserves… There was no evidence China was diversifying its existing holdings of U.S. debt, though it was a net seller of Treasury bills with maturities of one year or less, shifting toward U.S. debt with longer durations and slightly higher yields.”

The resulting gap of $150 billion, or 76% of China reserves’ growth, represents the biggest shortfall between reserves accumulation and purchases of U.S.-denominated assets by China in the last five years.

This recent move by China is only the beginning of a move away from the Dollar.

Don’t think for one second that China is spending its money recklessly just to move away from the US dollar. It’s well-calculated politics.

At a recent news briefing, Chinese Premier Wen Jiabao said, “China has been a heavy investor in the euro sovereign-debt market. We have bought a lot of euro bonds over the past years and we will continue to support Europe and the euro. China is ready to seize the opportunity together with its European partners, tackling challenges and driving development to support the quickest possible recovery of the global economy and stable growth.

Of course, we all know there is no such thing as a free lunch.

China clearly wants to diversify away from the Greenback. But it also needs to be careful as it owns so much of it. In order for China to truly be recognized as one of the world’s leading nations, it needs more than GDP growth – it needs support of their own currency, the Yuan.

By helping Europe in its time of need, China brings support to its own currency. For example, China will support the development of the Hungarian economy by buying a “certain amount of Hungarian government bonds.” As a result, Hungarian Prime Minister Viktor Orban said China will double its trading volume with the country to US$20 billion by 2015. China will also establish a European logistics and transport hub in Hungary, in line with Hungary’s earlier hopes to become a European hub for China as a logistics and commercial distribution center.

In separate speech in Hungary, Mr. Wen told us that China supports expanding the use of the Yuan to settle cross-border trade with central and eastern Europe, reducing the country’s dependence on the U.S. dollar in international trade.

I already talked about how China and Russia announced a decision to abandon the dollar in bilateral trade dealings, resolving instead to use their own currencies. (see It’s Already Here). Now China is moving its cause into Europe. You can bet that eventually, this will hurt the Dollar.

Let’s move onto the world’s second largest holder of US stockpile, Japan.

Given the recent natural disaster, most of Japan’s money will be spent on its own recovery. But aside from the rebuilding process, it was announced a few months back that Japan’s public pension fund is planning to withdraw about 6.4 trillion yen ($78 billion) from its assets in this financial year to cover a shortfall in pension payouts.

Why is this important?

Here’s what Societe Generale’s Dylan Grice had to say earlier this year in his report, Popular Delusions, A global fiasco is brewing in Japan:

“Japan’s government borrows from Japanese households and has done for decades. But Japanese households are retiring, and traditionally retirees run down their savings. So who will fund Japan’s future deficits, which are already within the range identified by inflation historian Peter Bernholz as hyperinflation ‘red flags’?

… As Japan’s retirees age and run down their wealth, Japan’s policymakers will be forced to sell assets, including US Treasuries currently worth $750bn, or Y70 trillion “eight months” worth of domestic financing. At nearly 10% of the outstanding US Treasury stock, this might well precipitate other government funding crises (bearing in mind that the Japanese model is the argument buttressing confidence in Western government bonds in the face of deteriorating fiscal conditions). At the very least I’d expect it to trigger an international bond market rout scary enough to spook all other asset classes.”

Do you think that Japan – even as the second largest consumer of US treasuries – will step up and buy more US treasuries when it has so many problems of its own?

I don’t.

Now let’s move onto the world’s third largest consumer of US garbage…I mean treasuries: Russia. (Don’t worry, I am almost done.)

Treasury department data showed that Russian holdings of U.S. Treasury securities fell to $125.4 billion in April 2011 from $176.3 billion in October 2010.

In a recent Dow Jones interview covered by WSJ, Arkady Dvorkovich, chief economic aide to Russia’s president, said that Russia will likely continue lowering its U.S. debt holdings as Washington struggles to contain a budget deficit and bolster a tepid economic recovery.

So there you have it. Insight on the world’s three largest holders and consumers of US treasuries. After reading that, do you still believe that QE3 won’t happen in some form or another?

But wait…we’re still missing one more massive buyer from this picture…or are we?

According Goldman Sachs, the biggest seller of US Treasuries in Q1, at an annualized rate of $1.1 trillion, were… drum roll please…

US Households!

According to Goldman, households in Q4 of 2010 were significant buyers of Treasury securities, shifting over $300 billion annualized into Treasuries, while in Q1 households were the dominant seller, accounting for more than $1.1 trillion in annualized outflows. That’s a net outflow of $800 billion! And guess who bought them all?

You guessed it…the Fed.

Only time will tell what will happen if the Fed doesn’t step in by Labour Day. We could see further declines in the market and further declines across all sectors. But eventually, Bernanke will have to step on the gas and print more money to once again put a temporary bandage on our economies.

So while this leaves us with more uncertainty, it will lead to one thing for sure: Higher precious metal prices.

I am not going to go back into all the details that is already driving and will drive gold to higher prices. It will happen. And it will happen soon. Before the year is over, look for gold to be much higher than where it is today.

The People’s Bank of China (PBOC), the central bank, just announced that it will issue more gold and silver to meet soaring demands for precious metals in the country by doubling, and tripling, certain circulation of precious metal coins.

In India, the import of gold and silver has risen by a whopping 222% between April and May 2011, as compared to a year ago. Imports of gold and silver were at $8.96 billion in May, a growth of 500% over the previous month and 222% over last year.

India’s central bank, the Reserve Bank of India, has also made decisions to grant licenses to seven more banks to import bullion. As of the start of 2011, some 30 banks in India have been granted permission to import gold and silver to meet the growing demand of the precious metals.

Even on home court, more than a dozen state legislators in America have now seen bills introduced that would make gold and silver coins legal tender in the respective states (see The Greatest War in History).

Much of this activism is coming from Tea Party supporters. Take a look at this video:

|

| click to play |

I believe that at current prices, mining share valuations are absurdly low and that fundamentals are bound to restore them to reality. That means that over the next 6-12 months, I expect the shares of both gold miners and strong speculative explorers to finally beat the returns of gold itself.

Summer is finally here and that means hunting season is coming around the corner. Happy hunting.

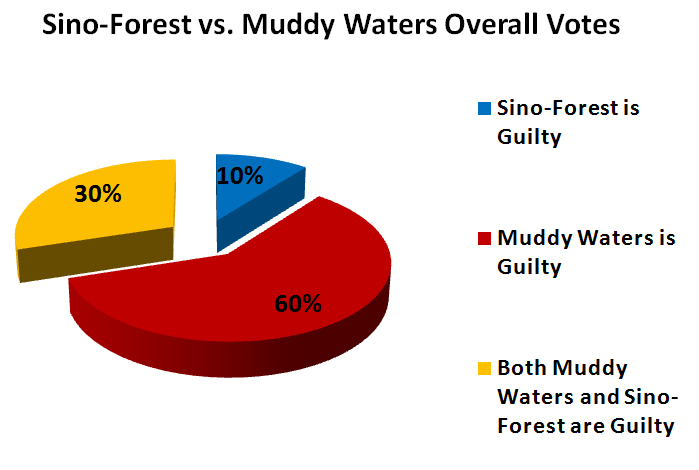

The Results are In

Last week, we conducted the following survey:

The report by Muddy Waters on Sino-Forest has caused a major decline in the shares of many Chinese-listed companies around the world, leading to a great opportunity for many short sellers to profit. Do you believe that Sino-Forest is Guilty? Or do you believe that Muddy Waters should be found guilty of fraud by releasing a report that may be inaccurate for their own profit?

Below are the Results from last week’s poll.

Click here for some random comments posted by our readers.

Housekeeping

Next week is a long awaited holiday for many of us. It is Canada Day here at home, and also Independence Day for our friends down south. That means that we will be skipping a week of the Equedia Weekly Letter. Regular editions will resume July 10, 2011. Have a great long weekend!

Until next week,

Ivan Lo

Equedia Weekly

Questions?

Call Us Toll Free: 1-888-EQUEDIA (378-3342)

For the full interactive newsletter and report, please follow this link: http://archive.constantcontact.com/fs005/1102243211822/archive/1106206837209.html

If you have not already subscribed to Equedia Weekly, you may sign up here:http://equedia.com/newsletter/

Forward-Looking Statements

This Newsletter and report contains certain forward-looking statements that may involve a number of risks and uncertainties. Actual events or results could differ materially from current expectations and projections. Except for statements of historical fact relating to the project, certain information contained herein constitutes “forward-looking statements”. Forward-looking statements are frequently characterized by words such as “plan”, “expect”, “project”, “intend”, “believe”, “anticipate” and other similar words, or statements that certain events or conditions “may” or “will” occur.

Except for the statements of historical fact, the information contained herein is of a forward-looking nature. Such forward-looking information involves known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievement of the Company to be materially different from any future results, performance or achievements expressed or implied by statements containing forward-looking information.

Although the Company has attempted to identify important factors that could cause actual results to differ materially, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that statements containing forward looking information will prove to be accurate as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on statements containing forward looking information. Readers should review the risk factors set out in the Company’s prospectus and the documents incorporated by reference.

Cautionary Note to U.S. Investors Concerning Estimates of Inferred Resources

This presentation uses the term “Inferred Resources”. U.S. investors are advised that while this term is recognized and required by Canadian regulations, the Securities and Exchange Commission does not recognize it. “Inferred Resources” have a great amount of uncertainty as to their existence, and great uncertainty as to their economic and legal feasibility. It cannot be assumed that all or any part of an Inferred Resource will ever be upgraded to a higher category. Under Canadian rules, estimates of “Inferred Resources” may not form the basis of feasibility or other economic studies. U.S. investors are also cautioned not to assume that all or any part of an “Inferred Mineral Resource” exists, or is economically or legally mineable.

Disclaimer and Disclosure

Disclaimer and Disclosure Equedia.com & Equedia Network Corporation bears no liability for losses and/or damages arising from the use of this newsletter or any third party content provided herein. Equedia.com is an online financial newsletter owned by Equedia Network Corporation. We are focused on researching small-cap and large-cap public companies. Our past performance does not guarantee future results. Information in this report has been obtained from sources considered to be reliable, but we do not guarantee that it is accurate or complete. This material is not an offer to sell or a solicitation of an offer to buy any securities or commodities.

Furthermore, to keep our reports and newsletters FREE, from time to time we may publish paid advertisements from third parties and sponsored companies. We are also compensated to perform research on specific companies and often act as consultants to many of the companies mentioned in this letter and on our website at equedia.com. We also make direct investments into many of these companies and own shares and/or options in them. Therefore, information should not be construed as unbiased. Each contract varies in duration, services performed and compensation received.

Equedia.com is not responsible for any claims made by any of the mentioned companies or third party content providers. You should independently investigate and fully understand all risks before investing. We are not a registered broker-dealer or financial advisor. Before investing in any securities, you should consult with your financial advisor and a registered broker-dealer. The information and data in this report were obtained from sources considered reliable. Their accuracy or completeness is not guaranteed and the giving of the same is not to be deemed as an offer or solicitation on our part with respect to the sale or purchase of any securities or commodities. Any decision to purchase or sell as a result of the opinions expressed in this report OR ON Equedia.com will be the full responsibility of the person authorizing such transaction.

Again, this process allows us to continue publishing high-quality investment ideas at no cost to you whatsoever. If you ever have any questions or concerns about our business or publications, we encourage you to contact us at the email or phone number below.

Please view our privacy policy and disclaimer to view our full disclosure at http://equedia.com/cms.php/terms. Our views and opinions regarding the companies within Equedia.com are our own views and are based on information that we have received, which we assumed to be reliable. We do not guarantee that any of the companies will perform as we expect, and any comparisons we have made to other companies may not be valid or come into effect. Equedia.com is paid editorial fees for its writing and the dissemination of material and the companies featured do not have to meet any specific financial criteria. The companies represented by Equedia.com are typically development-stage companies that pose a much higher risk to investors. When investing in speculative stocks of this nature, it is possible to lose your entire investment over time. Statements included in this newsletter may contain forward looking statements, including the Company’s intentions, forecasts, plans or other matters that haven’t yet occurred. Such statements involve a number of risks and uncertainties. Further information on potential factors that may affect, delay or prevent such forward looking statements from coming to fruition can be found in their specific Financial reports.

Equedia Network Corporation is also a distributor (and not a publisher) of content supplied by third parties and Subscribers. Accordingly, Equedia Network Corporation has no more editorial control over such content than does a public library, bookstore, or newsstand. Any opinions, advice, statements, services, offers, or other information or content expressed or made available by third parties, including information providers, Subscribers or any other user of the Equedia Network Corporation Network of Sites, are those of the respective author(s) or distributor(s) and not of Equedia Network Corporation. Neither Equedia Network Corporation nor any third-party provider of information guarantees the accuracy, completeness, or usefulness of any content, nor its merchantability or fitness for any particular purpose.