Every once in a generation, the global economy gets blindsided.

A once-obscure material—long ignored, long misunderstood—suddenly becomes the epicenter of national security, energy transition, and geopolitical tension.

We’ve seen it before with uranium in the 1950s…

Rare earths in the 2000s…

Lithium and graphite in the 2010s…

But over the last year, something much bigger has broken to the surface.

And hardly anyone is paying attention.

The Next Critical Mineral Crisis Has Arrived

Antimony.

Most investors can’t even pronounce it.

Yet world governments are now scrambling for it. And for good reason:

- It’s a top-tier U.S. Critical Mineral essential to national security and modern technology.

- It’s needed for ammunition, advanced optics, night vision, semiconductors, lasers, grid-scale energy storage, and more.

- China controls the overwhelming majority of global supply—mining, refining, and processing.

Last year, the World Economic Forum issued a stark warning:

“Critical minerals, once a niche concern, have become a leverage point in a much broader struggle over industrial resilience and global influence. In particular, the story of antimony — a mineral used for over 5,000 years in pigments, alloys and weaponry — should serve as a warning to US and European markets to work together to ensure access to strategically valuable resources.” – WEF Critical Minerals Report, November 2025

In short, antimony is becoming one of the most strategically important—and scarce—minerals in the world. As geopolitical pressures continue to rise, supply chains are tightening.

Worst of all, the West faces a massive shortfall.

This aligns exactly with what we wrote in our June 2025 report, “How to Play the Critical Minerals Boom.”

In that letter, we highlighted how:

- The U.S. has a near-zero domestic mine supply,

- China has begun imposing export restrictions,

- And the Pentagon has designated antimony as essential to defense readiness.

But the biggest risk?

The US has very little antimony production and refining capabilities.

And there are few high-grade, near-surface antimony discoveries in North America.

Almost none—until now. More on this in just a bit.

The Weapon No One Is Talking About

Somewhere right now, a US missile is being readied for launch.

Inside its ignition system—buried in the primer, the detonator, the infrared sensor guiding it to its target—is a metal most Americans have never heard of.

It’s not lithium. Not copper. Not uranium.

It’s antimony.

And here’s the terrifying part:

The United States produces almost none of it.

Antimony sits at the intersection of three pillars of modern power: defense, energy, and technology. It hardens bullets and artillery shells. It enables night vision and infrared missile guidance. It flame-proofs military vehicles, aircraft electronics, and semiconductor housings. The US Department of Defense uses it in more than 200 types of ammunition alone.

For decades, none of that mattered. Global supply was cheap, abundant, and quietly dominated by one country: China.

That era is over.

The Shots Being Fired — And What They Cost

By now, you’ve seen the headlines from the Middle East:

Tehran downs 2 US warplanes; Israel bombs Lebanon bridges

Israel strikes Beirut as U.S. warns Iran may target universities

US intelligence warns Iran unlikely to ease Hormuz Strait chokehold soon, sources say

Meanwhile, Saudi Arabia, the UAE, and other key US partners are under threat, leaning on American-supplied defense systems to hold the line.

Iran. Missiles. Counter-strikes. US military involvement. Saudi Arabia, the UAE, and other key US partners under threat, leaning on American-supplied defense systems to hold the line.

What the headlines don’t tell you is the price tag.

According to estimates from the Center for Strategic and International Studies, the cost of US military operations against Iran has already surpassed $20 billion, and is likely to exceed $25 billion by the end of this week.

And that’s before any supplemental Congressional appropriations, which could add hundreds of billions more.

Every missile fired, every round of armor-piercing ammunition, and every night-vision system used by US partners in the region…all of them consume antimony.

And virtually every nation involved in this conflict—on any side—relies on the same metal to make their weapons function.

Think about that for a moment.

The US stockpile is being drawn down in real time. Meanwhile, China, which controls nearly half of global mined antimony supply and dominates refining and processing, is watching. Building. And stockpiling.

China’s Leverage

In December 2024, China dropped the hammer.

Beijing formally banned antimony exports to the United States—along with gallium and germanium—as direct retaliation for US semiconductor restrictions.

The US Geological Survey estimated that a full ban on gallium and germanium alone could wipe $3.4 to $9 billion from US GDP. Add antimony, and the damage compounds quickly.

This sent antimony prices soaring to nearly $60,000 per tonne.

This immediately sent shockwaves through the antimony market, putting the US in a very tough spot.

As a result, Trump had to succumb to some of the wishes of China.

In November 2025, Beijing partially backed off, suspending the ban until November 27, 2026, as part of a broader trade truce brokered after Trump and Xi met in South Korea.

The mainstream media called it a de-escalation and a goodwill gesture.

It wasn’t.

Here’s what they missed:

- The ban is suspended—not cancelled. Beijing retains the export control list. Every shipment still requires a license approved by the Chinese government.

- Military end-users remain blacklisted. The prohibition on selling antimony for US military use was never lifted. Not even for a day.

- The clock is ticking. November 27, 2026. That’s when the suspension expires. After that, Beijing can reinstate the full ban with a single announcement.

- China is sending a message. In January 2026, Beijing tightened export controls on dual-use items to Japan over Taiwan’s comments. Critical minerals are leverage, and China will use them.

- Beijing is prosecuting violators. In December 2025, a Chinese court convicted 27 people for smuggling antimony, sentencing the ringleader to 12 years in prison.

China’s control of critical minerals is one of its most powerful bargaining tools – especially in the current geopolitical war.

The current antimony suspension gives the US less than a year before China can flip the switch back off and force the US into more negotiations.

This does not bode well for the US – that is, unless the US can find more supply elsewhere.

The Price Tells the Story

Markets don’t lie.

Antimony prices hit an all-time high of $59,750 per tonne in July 2025—up more than 54% from the year prior. The global supply-demand gap widened to 34,000–39,000 tonnes in 2025, the widest five-year shortfall ever recorded.

China’s own domestic production fell by approximately 16% year-over-year from January to November 2025, driven by mine closures and environmental restrictions. Imports of antimony ore into China dropped more than 33% over the same period.

Even with prices easing from their peak, the structural reality hasn’t changed. Analysts forecast a supply-demand deficit of 9,000 to 14,000 tonnes annually through 2027. New mines take 3–5 years to permit and build. You cannot solve this crisis overnight.

And here is the part that most investors still haven’t grasped: there is no ETF for antimony. No futures contract. The only way to get exposure is through the handful of mining companies positioned to actually produce it.

And right now, most of those companies are NOT in the United States.

Why the US Desperately Needs Its Own Supply

This isn’t just about price; it’s about sovereignty.

Consider the chain of dependencies: the US fields the most advanced military in the world. That military supplies its allies in the Middle East, in Asia, and in Europe. Sales of US military equipment to foreign governments hit an unprecedented $238 billion in 2023.

Last year, it hit $331.18 billion.

Now get this: in FY 2025, there are 16,098 foreign military sales cases with an open case value of over $934 billion!

And those systems—every round of armor-piercing ammunition, every guidance chip in every missile, every night-vision device worn by a soldier—depends on a supply chain that mostly runs through Beijing.

That is not a sustainable position for the world’s biggest arms dealer and the most powerful nation.

The Pentagon knows it, which is why the Department of the Interior has formally listed antimony as a critical mineral, while the Defense Production Act has been activated to fund domestic supply chain development.

The U.S. National Defense Stockpile (NDS), an emergency reserve that exists precisely for moments like this, is running low on everything – including antimony.

In fact, it’s reached “its lowest levels since the Cold War.”

At the exact moment the military is burning through it in the Middle East…

It’s no wonder the Defense Logistics Agency has signed a $245 million sole-source contract to begin replenishing the NDS.

It’s no wonder that the US is committing serious money to this problem.

Perpetua Resources’ Idaho antimony project has attracted US$75 million in DoD awards, approximately US$2.7 billion in EXIM Bank financing now advancing to Congressional notice, and US$255 million in strategic private-sector investment.

But there’s still a problem: Perpetua is not expected to go into production until at least 2029.

There is a clear mandate in Washington: find domestic production, and find it fast!

And the keyword is “fast.”

Because with nearly $1 trillion in open case contracts, continued war with Iran, and a near-empty NDS, the US has to gain access to more antimony.

November 2026 is not far away.

The Only Answer

And that is why today’s letter is so timely.

Because one company has been reporting some of the highest-grade oxide antimony results in the United States in years.

A discovery that sits on U.S. soil, in a brownfield mine site setting, with existing infrastructure, and already advancing toward a near-term production scenario.

In fact, it could be the next and only pure-play US antimony company to go into production by 2027.

In other words, it’s exactly what the United States needs right now.

This company is…

NevGold Corp.

TSXV: NAU | OTCQX: NAUFF | Frankfurt: 5E50

Disseminated on behalf of NevGold Corp.

For many, you already know the story. We have told you about NevGold many times before.

And if you’ve been fortunate enough to be an investor when we first introduced it to you, you may have already seen your money 5x.

If you haven’t read our last report, you can find it here: “How to Play the Critical Minerals Boom.”

But the story keeps getting better.

NevGold has announced that they have a path to be the next and only pureplay antimony producer in the United States by 2027 at its Limousine Butte Project in Nevada.

This is a strategically significant, geopolitically aligned opportunity, arriving at exactly the moment when the U.S. government is urgently seeking domestic antimony supply.

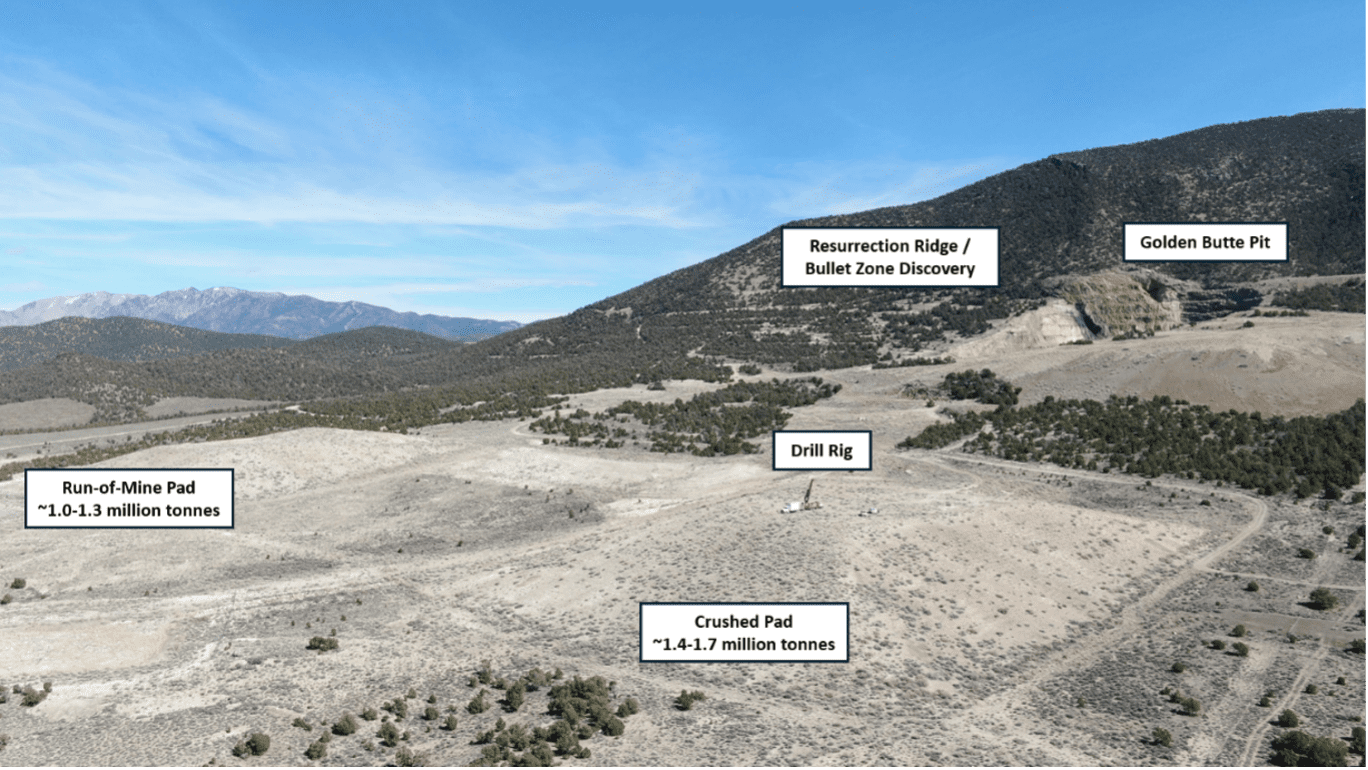

A Historic Near-Term Production Scenario

When most people look at an old heap-leach pad, they see the forgotten remnants of a mine long past its prime.

But every now and then, history leaves behind a gift—material that was mined, crushed, and placed neatly on engineered pads, waiting for someone with the right lens to recognize what others once missed.

In 1989 and 1990, the Golden Butte mine in White Pine County, Nevada produced over 100,000 ounces of gold. The operators were focused entirely on gold. Antimony wasn’t strategic. It wasn’t valuable. They didn’t even test for it.

So they stacked antimony-rich rock directly onto the pads and walked away.

Fast-forward to today, when antimony has become one of the most important critical minerals for defense, energy, and national supply chains. Suddenly, the story at Golden Butte looks very different.

NevGold’s Phase 1 sampling program completed early 2026 shows that the material sitting on the surface of those historic pads—material that’s already been mined, already been crushed, and already been paid for—carries meaningful antimony and gold grades.

CEO Brandon Bonifacio says: “We are in an advantageous position as we have development optionality as we advance Limo Butte towards a potential production and cash-flow scenario by 2027, with further phased gold-antimony project development scenarios in the future.”

In other words, NevGold has a real near-term opportunity to be the next producer of antimony in the United States.

The Back-of-Napkin Math

The company just finished a large drill program on the historical leach pads, and they are advancing to a formal Mineral Resource Estimate (“MRE”) by Q2-2026.

But based on initial sampling, we can guess the numbers.

The Golden Butte leach pads hold roughly 2.5–3 million tonnes of previously mined and crushed material. The initial sampling results, released January 6, 2026, show an average antimony grade of 0.3% Sb.

At that grade, the pads contain approximately 8,500 tonnes of antimony metal sitting in material that has already been mined, hauled, and processed once. Apply a conservative 80% recovery rate based on NevGold’s recent leach testing—the recoverable portion still totals roughly 6,800 tonnes of antimony.

At $50,000 per tonne of antimony, that equals a staggering US$340 million worth of antimony at surface—held by a junior mining company worth less than US$100 million.

In other words, even at a modest grade and conservative recovery, the historic Golden Butte pads could represent a meaningful domestic antimony source, hiding in plain sight.

And that does not include any of the upside from the rest of the 67-square-kilometer project and the recent high-grade antimony Bullet Zone and Armory Fault discoveries…

When you account for the full project scope, NevGold is targeting a potential for more than 10,000 antimony tonnes from the leach pads alone by 2027—and a much larger development scenario with geologic potential for over 100,000 antimony tonnes from the broader project by 2029.

I’ll let you run the math on what that might be worth.

This is not only an opportunity to produce antimony sooner than anyone else in the US, but it creates something the United States has never had:

A vertically integrated, domestic US antimony supply chain.

But there is something else that makes this project even more special.

Oxide vs. Sulphide — The Differentiator That Changes Everything

This is the part of the NevGold story that most people walk right past.

And it may be the most important part of all.

Here is a question that almost no one in the mainstream mining press is asking: even if you find antimony in the United States, how do you actually process it without sending it back to China?

Because here’s the dirty secret about the global antimony industry: most of the world’s antimony projects produce sulphide ore. That ore gets turned into an antimony concentrate—effectively a powder with 25–50% antimony purity. And that concentrate has to go somewhere to be refined into usable metal.

That somewhere is almost always China.

There are virtually no antimony smelters in North America or Europe capable of processing the material. So even if a Western company discovers antimony, it faces the same dependency problem at the back end. You’ve found the mineral. You still can’t process it without Beijing’s help.

NevGold doesn’t have that problem.

Because NevGold doesn’t have sulphide antimony.

NevGold has oxide antimony.

And that changes everything.

Why Oxide is a Metallurgical Dream

Before any company starts talking about trucks, plants, or sales agreements, there’s a critical step that every serious operator must take: metallurgical testing. This is where specialists take representative samples of that crushed material and run it through controlled lab processes to determine how antimony behaves, how easily it can be liberated, and which processing path gives the best recoveries.

Over the past 12 months, NevGold has been advancing that work aggressively. On November 5, 2025, the company announced up to 85% antimony recovery from positive Phase II metallurgical testwork at Limo Butte.

And in their most recent test work results, released April 2, 2026, things have gotten even better.

Sequential leaching recovered up to 99% of the remaining gold after the antimony had already been extracted. That means not only can they get the antimony out of the rocks, but they can also strip the gold out as well.

With gold prices continuing to hover near all-time highs, this project suddenly becomes quite substantial.

But it’s not just the recovery rates that matter. It’s how they’re doing it.

“Most of the global antimony projects are sulphide and narrow vein-type systems that require underground mining to produce an antimony concentrate, which adds significant complexities to the operation, cost structure, and concentrate marketing. At Limo Butte we have defined a large, near-surface footprint of oxide antimony mineralization which is amenable to leaching, and we have the opportunity to produce antimony metal at the project site. Being able to produce antimony metal at the project site removes reliance on downstream refining at a concentrator.”

— Brandon Bonifacio, CEO, NevGold Corp.

Oxide antimony behaves very differently from stibnite, the sulphide mineral that must be floated and then smelted. Oxide antimony can be dissolved using a controlled acid leach. Once in solution, the antimony is selectively recovered through electrowinning, cementation, or hydrolysis—producing high-purity antimony metal or antimony trioxide directly at site.

No smelter. No concentrate. No shipping antimony powder to China for refining.

Just clean, high-purity antimony metal, produced on US soil, at the project site, using proven hydrometallurgical chemistry.

Military-Grade Metal. At the Mine Site.

This is not a minor technical distinction. This is a strategic breakthrough.

NevGold is targeting the production of antimony metal at military-grade specifications, directly at the Limousine Butte project site.

Think about what that means in the context of everything we’ve discussed. The US military needs antimony that meets exacting purity standards for ammunition primers, guidance systems, and defense electronics. Today, that metal almost entirely comes through supply chains that run through China.

NevGold’s oxide metallurgy produces finished metal—not concentrate, not powder, not an intermediate product that needs further processing. High-purity antimony metal, to military-grade specifications, produced and refined in Nevada.

That is exactly what the Pentagon has been asking for. And it is something that virtually no other Western antimony project can offer at this speed.

Almost every other Western project produces sulphide concentrate. That concentrate then has to travel offshore for smelting before it becomes usable metal. NevGold skips that step entirely.

- No reliance on foreign smelters

- No concentrate shipping constraints

- No Chinese refining bottleneck at the back end

- Finished, high-purity antimony metal produced at site

- Military-grade specifications. On US soil.

This is the type of domestic, vertically integrated processing pathway that the U.S. government and defense sector have been pushing for.

And NevGold may be the only company in the United States positioned to actually deliver it in the near term.

Some of the Highest-Grade Antimony Intercepts in the United States

The leach pad story alone is compelling. But it’s only half of what’s happening at Limousine Butte.

Below the surface, NevGold’s drill program has been hitting antimony grades that are turning heads in the industry.

From the newly discovered Bullet Zone:

- “5.51% Antimony Over 4.6 Meters Within 4.00 g/t AuEq Over 41.1 Meters (0.96% Antimony and 0.29 g/t Au) at Limo Butte, Nevada”

- “NevGold Intercepts 5.89% Antimony Over 3.0 Meters Within 2.67 g/t AuEq Over 53.3 Meters (0.59% Antimony And 0.36 g/t Au) At Bullet Zone”

- “12.42 g/t AuEq Over 3.1 Meters (3.06% Antimony And 0.53 g/t Au) Within 3.30 g/t AuEq Over 32.0 Meters”

- “11.42 g/t AuEq Over 7.7 Meters (2.64% Antimony And 1.17 g/t Au) Within 4.91 g/t AuEq Over 27.4 Meters”

These are exceptional oxide antimony grades, especially at near-surface levels.

And NevGold’s step-out drilling has hit 100% of the holes drilled so far:

- Confirmed a major thrust-fault-preserved mineralized zone

- Expanded the footprint at Resurrection Ridge

- Intersected mineralization in both upper and lower zones

- Validated the company’s new geological model, significantly enlarging the potential resource envelope

- Extended the Pilot Shale host rock—which hosts Carlin-type Au-Sb systems—more than one kilometer east of previous drilling, opening a new district-scale trend

30 holes have been completed in the current 2025–2026 drill program, and we’re still waiting on 8 more holes.

In other words, there’s more to come.

The Permitting Non-Issue

There is one more thing that separates NevGold from virtually every other critical minerals project in America: Permitting.

If you’ve followed the mining sector for any length of time, you know that permitting is where dreams go to die. Environmental reviews. Community opposition. Federal agency delays. Some of the best deposits in the world have sat in permitting purgatory for a decade or more.

NevGold doesn’t have that problem.

Limousine Butte is a brownfield mine site in the Nevada desert. It was already mined. The environmental footprint from past operations is established and well-understood. There is strong support from local communities and from the State of Nevada, which has long been one of the most mining-friendly jurisdictions in the world.

There are no environmental unknowns lurking in the review process. No indigenous heritage disputes. No community groups blocking access.

In fact, the March 20, 2025 Executive Order on critical minerals explicitly demands:

- “Priority projects that can be immediately approved.”

- “Acceleration of permits.”

- “A dedicated U.S. mineral investment fund.”

NevGold’s Limousine Butte project sits squarely in that policy crosshair:

- US jurisdiction — Nevada, one of the world’s premier mining states

- Brownfield environment — previously mined, no new ground disturbance required for near-term production

- Existing mined and crushed surface material with antimony production potential by 2027

- Near-surface oxide mineralization

- Strong local community and State of Nevada support

- Advancing toward a gold-antimony Mineral Resource Estimate in Q2-2026

The Pentagon has made it clear they will support viable domestic antimony producers.

We believe NevGold is rapidly entering that category.

Why This. Why Now.

Let’s connect the dots.

The US is fighting a war in the Middle East and burning through antimony-based munitions at an accelerating pace. The National Defense Stockpile is nearly depleted. China controls half the world’s supply and has already demonstrated its willingness to cut the US off. The export suspension expires November 2026. There is a clear government mandate to find domestic production. And the only near-term, at-surface opportunity in the United States is sitting on a brownfield site in Nevada, owned by a junior explorer whose Mineral Resource Estimate is weeks away.

This isn’t a story about a mining company.

This is a story about national security meeting investment opportunity.

Those moments don’t come often. When they do, the investors who are paying attention—who saw the setup before the crowd did—are the ones who benefit most.

When you combine:

- A scarce, strategically essential mineral

- A geopolitical supply crunch with a hard deadline

- A U.S. mandate to approve and fund domestic projects

- A near-term, at-surface production scenario

- Military-grade metal producible at site—without any reliance on Chinese smelters

- Straightforward brownfield permitting in a mining-friendly jurisdiction

- A high-grade underground discovery that is still open in all directions

- And a forthcoming MRE expected in Q2-2026

…you get the conditions we have always looked for at Equedia.

As the World Economic Forum recently put it:

“If governments and industry can get this right, antimony could become the model for building resilience before the next critical minerals supply chain choke point emerges.”

Stay tuned.

More catalysts are coming.

Seek the truth and be prepared,

Carlisle Kane

The Equedia Letter

NevGold Corp.

Canadian Trading Symbol: NAU

US Trading Symbol: NAUFF

German Trading Symbol: 5E50

Disclosure: This letter is disseminated on behalf of NevGold Corp. Equedia owns shares in NevGold Corp. Always conduct your own due diligence before investing. See full terms and disclaimer at equedia.com.

Disclaimer:

Equedia.com and Equedia Network Corporation are not registered as investment advisers, broker-dealers or other securities professionals with any financial or securities regulatory authority. Remember, past performance is not indicative of future performance. This article also contains forward-looking statements that are subject to risks and uncertainties that could cause actual results to differ materially from the forward-looking statements made in this article. Just because many of the companies in our previous Equedia Reports have done well, doesn’t mean they all will. We are biased towards Nevgold (NAU) because the Company is an advertiser on www.equedia.com. We currently own shares of NAU. You can do the math. Our reputation is built upon the companies we feature. That is why we invest in every company we feature in our Equedia Special Report Editions. It’s your money to invest and we don’t share in your profits or your losses, so please take responsibility for doing your own due diligence and consult your own professional advisers before investing in NAU or trading in NAU securities. NAU and its management have no control over our editorial content and any opinions expressed in this article are our own. We’re not obligated to write a report on any of our advertisers and we’re not obligated to talk about them just because they advertise with us. For a complete disclosure of the compensation received by us from NAU, please review our Terms of Service and full disclaimer at www.equedia.com/terms-of-use/.

This newsletter (this “Newsletter”) is provided by Equedia Network Corporation (“Equedia”, “we” or “us”). Your access to and use of this Newsletter is subject to and governed by this disclaimer and Equedia’s Terms of Use, which is available at http://www.equedia.com/terms-of-use (the “Terms”). Please read this disclaimer and the Terms carefully. This Newsletter is not an offer to sell or a solicitation of an offer to buy any securities or commodities. To the extent that anything contained in this Newsletter may be deemed to be investment advice or a recommendation in connection with a particular company or security, such information is impersonal and is not tailored to the needs of any specific person. In addition to historical information, this Newsletter may contain forward-looking statements, including statements with respect to third parties regarding product plans, future growth, market opportunities, strategic initiatives, industry positioning, customer acquisition, the amount of recurring revenue and revenue growth. In addition, when used in this Newsletter, the words “will,” “expects,” “could,” “would,” “may,” “anticipates,” “intends,” “plans,” “believes,” “seeks,” “targets,” “estimates,” “looks for,” “looks to,” “continues” and similar expressions, as well as statements regarding a third party’s focus for the future, are generally intended to identify forward-looking statements. Each of the forward-looking statements we make in this Newsletter involves risks and uncertainties that may cause actual results to differ materially from these forward-looking statements. Factors that might cause or contribute to such differences include, but are not limited to, those disclosed by the parties referred to in this Newsletter in their public securities filings. You should carefully review the risks described therein. You should not place undue reliance on the forward looking statements in this Newsletter, which speak only as of the date such statement was published. Equedia undertakes no obligation to publicly release any revisions to the forward-looking statements or reflect events or circumstances after the date of their publication, except as required by law. As of the date of publication of this Newsletter, Equedia (on behalf of itself and any partner, director, officer or insider of Equedia) may have a financial or other interest in the party or parties featured in this Newsletter, within the meaning of National Instrument 31-103 – Registration Requirements, Exemptions, and Ongoing Registrant Obligations, published by the Canadian Securities Administrators. For full details of our compensation, please visit https://www.equedia.com/terms-of-use/.

As of the date of publication of this Newsletter, Equedia (on behalf of itself and any partner, director, officer or insider of Equedia) may have a financial or other interest in the party or parties featured in this Newsletter, within the meaning of National Instrument 31-103 – Registration Requirements, Exemptions, and Ongoing Registrant Obligations, published by the Canadian Securities Administrators. Equedia and its directors own shares of Nevgold (NAU) at the time of this writing. In March 2026, Equedia was paid $250,000 for three months of advertising services. We have also previously been compensated by NAU for advertising contracts, which have expired.

What about Antimony ( UAMY )? And of course ( PPTA ) Perpetua in Idaho?

Really enjoyed reading this. Your perspective on this topic is very interesting. Thanks for putting this together. (ref:335414cf0465)

I bought west point Gold but has continually dropped in price. What is going on. Typically Equedia recommendations are good.